Novo Resources Corp (TSX:NVO, OTCQX:NSRPF, ASX:NVO, FRA:1NOR) has delivered a maiden mineral resource estimate for the Leven Star Reef at its Belltopper Gold Project in Victoria, outlining an inferred resource of 760,000 tonnes grading 3.6 g/t gold for 87,000 ounces of contained gold.

The resource marks the first JORC-compliant mineral resource at Belltopper and provides an initial foundation for a project that Novo believes still offers substantial growth potential through additional drilling and resource definition.

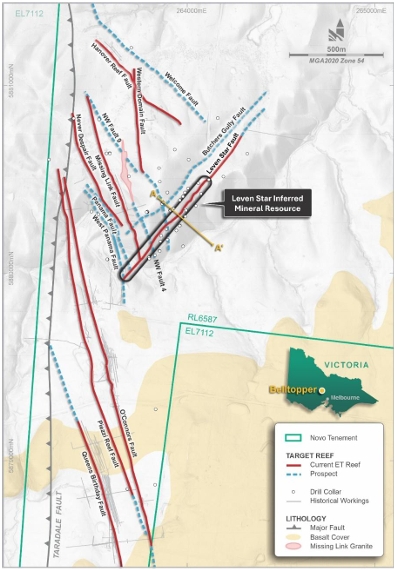

Leven Star is one of eight high-grade gold-bearing reefs included within Belltopper’s broader exploration target, which was upgraded earlier this year and currently ranges from 2.1 million to 3.1 million tonnes at 6.7–8.9 g/t gold for between 460,000 and 880,000 ounces of contained gold.

“The delivery of this maiden Inferred Mineral Resource at Novo’s Belltopper Gold Project marks an important milestone for the Belltopper Gold Project and for Novo generally,” said Novo Resources executive co-chairman and acting chief executive officer Mike Spreadborough.

“An initial 87,000-ounce Inferred Mineral Resource Estimate provides a solid foundation for what we see as a highly prospective asset, with encouraging potential for further resource definition given the previously released Exploration Target — all underpinned by the current gold price environment, which is as favourable as we have seen it in a generation.”

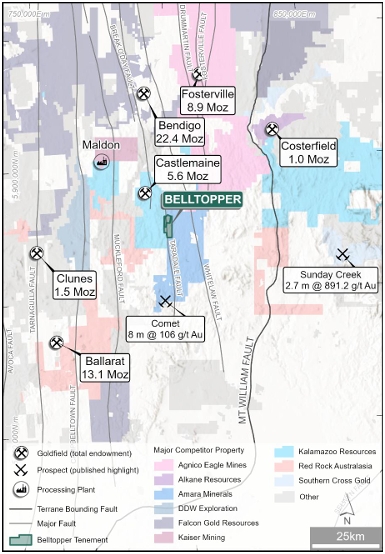

Belltopper Gold Project location map with regional gold occurrences and major structure.

Open in multiple directions

The Belltopper project lies about 120 kilometres northwest of Melbourne in Victoria’s historic Bendigo Zone, a region that has produced more than 60 million ounces of gold and hosts major operations including Fosterville and Costerfield.

Novo noted that the Leven Star Reef has been relatively lightly drilled, with just 44 drill holes completed to date. Mineralisation remains open in multiple directions, offering opportunities to expand the resource with further exploration.

Drilling has defined mineralisation over roughly 800 metres of strike, with the reef distinguished by a quartz-veined stockwork-breccia system rather than the more typical quartz vein-hosted gold mineralisation seen elsewhere in Victoria.

The current resource is based solely on the Leven Star Reef and has been assessed on the basis of underground mining. Novo said the broader Belltopper system includes seven additional reefs that could contribute future resource growth.

Map of Belltopper area showing the Leven Star Reef Inferred Mineral Resource extent and Exploration Target. Diagram also depicts other current Exploration Target Reefs: Missing Link; Never Despair; O’Connors; Queens/Egyptian; Hanover Fault; Piezzi/Stackyards and Western Domain Fault; in addition to other prospective key target faults.

Underground mining scenario

The resource estimate was generated using underground mineable stope optimisation shapes and a 1.9 g/t gold cut-off grade. Key assumptions included a gold price of A$5,250 per ounce, metallurgical recovery of 88%, mining costs of A$162 per tonne and processing costs of A$119 per tonne.

Novo said a mine life of between five and 10 years was considered appropriate for the assessment of reasonable prospects for eventual economic extraction.

Metallurgical test work completed on sulphide mineralisation indicated flotation is likely to be the preferred processing route, with testing delivering overall gold recoveries of around 93% when flotation and gravity recovery were combined.

Drilling campaign planned

Novo is preparing a new drilling campaign for the second half of 2026 aimed at both expanding the Leven Star resource and advancing the wider Belltopper exploration target.

The company plans initial scoping-level drilling across the remaining seven exploration target reefs as well as tests of additional historic gold reefs that currently sit outside the exploration target.

High-priority targets within the Belltopper Anticline Corridor are also scheduled to be drilled as part of the upcoming program.

Novo said its strategy is to grow Belltopper through incremental resource expansion at Leven Star while systematically evaluating the project’s broader network of high-grade gold reefs.