Stock Surges 46% in 2026: AI Infrastructure Growth, Earnings, and Outlook")

TradingKey – Cisco Systems, Inc. (NASDAQ: CSCO) is one of the most unexpected stocks in the 2026 market. According to Yahoo Finance and Zacks Investment Research, the networking stock is up nearly 46% in value. The rally easily beats both the Nasdaq index performance, as well as the overall 14.6% gains achieved in the Computer and Technology Sector. But for a firm that was once thought of as a legacy hardware play, the surge raises the question: What’s changed?

What Drives Cisco’s 46% Growth?

The quick response: enterprise and hyperscale customers are upgrading their network gear sooner than planned, and many of those investments are directly associated with the build-out of AI data centers. The technology company’s stock has climbed by approximately 45% since March 31 through the early part of July 2026; the bulk of the gains have been driven by a single earnings report in May.

How Did Cisco Beat Analysts’ Consensus in Q3 2026?

Cisco’s fiscal 3Q 2026 results, which wrap up on April 25, 2026, have come in well ahead of the consensus. The total revenue was $15.84 billion, up 12% year-over-year, and wider than the average analyst estimate of $15.56 billion, while adjusted EPS of $1.06 topped the forecast of $1.04, per CNBC.

The networking product segment, which is particularly affected by the AI-powered data center upgrades, registered a 25% revenue increase to $8.82 billion. Orders increased 35% YOY, and the forecasted revenue for the next quarter of $16.7-$16.9 billion was higher than analysts’ estimates.

The company’s stock jumped 15% after the report, and CNBC noted that the results would be Cisco’s best since 2002.

How Much Has Cisco’s Orders For AI Infrastructure Grown?

What sets Cisco apart from a networking refresh cycle is the order for AI infrastructure. The hyperscaler orders of AI infrastructure were at $1.9 billion in fiscal Q3, with a cumulative value for the year to date of $5.3 billion. This is already more than the initial forecast by management of $5 billion for FY26. Since then, Cisco has increased its forecasts for orders for AI infrastructure in FY26 to roughly $9 billion, almost four and a half times the order intake during fiscal 2025.

Such an order backlog was the reason why Cisco was being classified as among the beneficiaries of AI infrastructure despite not having developed any AI chip, a factor which some investors attributed to Cisco’s outperformance this year relative to pure-play semiconductor stocks without any manufacturing risk exposure.

Why Would Cisco Cut Jobs in a Growing Business?

In discussing its earnings, Cisco announced a reduction of fewer than 4,000 positions, or less than 5% of its workforce, beginning in mid-May. Cisco’s CEO Chuck Robbins said that the job reductions were part of the company’s efforts to redirect investments toward demand-driven portions of its business, a move that appears to be consistent with the actions of a company that’s growing.

Cisco has acquired small businesses in the security and observability businesses in the fields in the past few months, including Galileo Technologies in April, Astrix Security in May, and WideField Security in June, all aimed at acquiring AI agents and infrastructure.

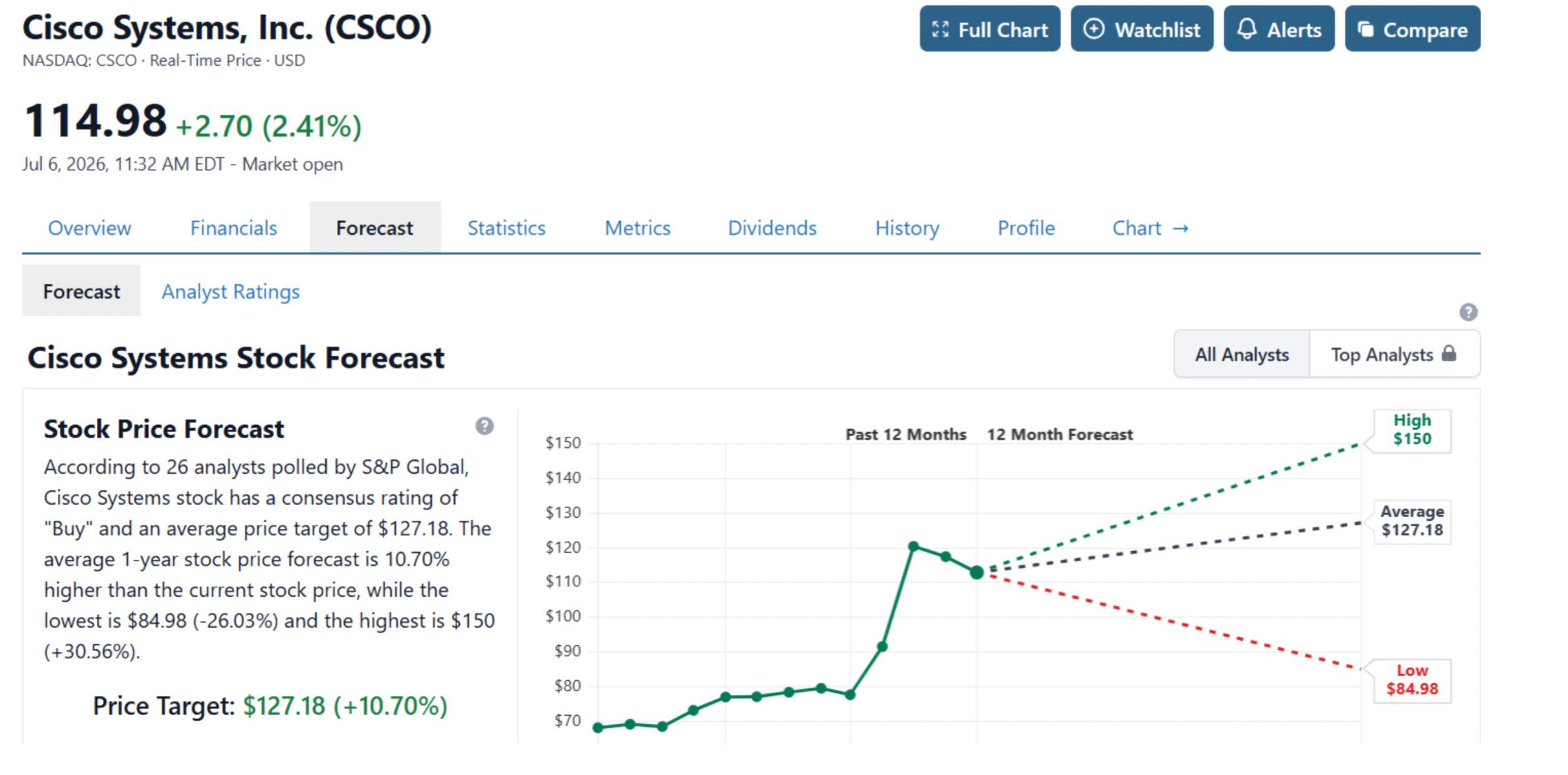

What Are Analysts Anticipating for Cisco Stock?

Wall Street sentiment is improving along with the stock. StockAnalysis.com reports that 26 analysts are averaging a “Buy” rating with a 12-month price target of about $127. Morgan Stanley and KeyBanc have both increased their targets to $130; HSBC upgraded Cisco to Buy in May thanks to momentum in AI infrastructure; and Bank of America (BofA) increased its target to $150 and maintains a Buy rating. Zacks upgraded to a “Strong Buy” rating in July based on better-than-expected earnings estimates.

Source: StockAnalysis.com

After This Run, Is Cisco Stock Still Worth Buying?

Not every stock valuation model believes there is upside left in this rally. Cisco’s stock has advanced from around $89 in April to a price in the $110-$120 range early in July, nearing its all-time high close of $130 reached on June 4. The long‑term model values Cisco at around $116 by 2030, suggesting limited upside as anticipated AI order growth is already reflected in the stock price.

Margins are another watch factor; Cisco took a 330 basis point hit to its non-GAAP product gross margin during the third quarter due to rising costs for memory components, despite more than 20 internal cost reduction programs and price increases offsetting this. EBIT for the third quarter was $5.41 billion, or 11% higher than the same period a year ago, and margins were at 34%.

In the aggregate, Cisco’s thesis heading into 2026 involves becoming the plumbing used in AI infrastructure, enterprise networks, security, and data center switching, a thesis the market seems to believe based on the current share price, and one that suggests further upside potential for Cisco’s shares only if margins can hold up given rising memory costs and increasing competition in hardware.

Cisco CSCO 2H Chart: Symmetrical Triangle Consolidation Near Oversold RSI

Cisco is trading within the symmetrical triangle pattern (A-B-C-D) on the 2H. Price has bounced near the lower trendline (black ascended trendline support) and has recently been testing red candlesticks with long lower wicks on this support, which is a typical price action during this stage. This price action is also indicative of tactical buying following an impulsive phase.

Cisco (CSCO) Price Chart – Source: Tradingview

The measured move from the symmetrical triangle (base) ranges from approximately $12-$15. Upside breakout targets range between $126-$133 whereas downside break below support will open targets between $106-$100. RSI 14 remains at 42.31 with no sign of divergence and still has room to move up or down to either side.

Price action volume is diminishing within the pattern which can be expected prior to a breakout event. Price action technical setup depicts high-probability directional resolution as symmetrical triangle is nearing its apex with support on the ascended trendline providing tactical defense.

Trade Idea: Long $113.84 with a stop below $106.00 targeting $126.10 on a breakout of the triangle.

Disclaimer: The content of this article solely represents the author’s personal opinions and does not reflect the official stance of Tradingkey. It should not be considered as investment advice. The article is intended for reference purposes only, and readers should not base any investment decisions solely on its content. Tradingkey bears no responsibility for any trading outcomes resulting from reliance on this article. Furthermore, Tradingkey cannot guarantee the accuracy of the article’s content. Before making any investment decisions, it is advisable to consult an independent financial advisor to fully understand the associated risks.