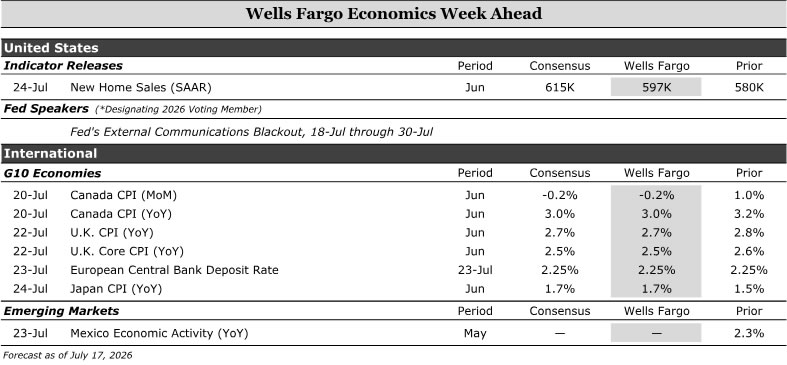

We expect new home sales to rebound modestly in June following recent weakness, although elevated mortgage rates and soft buyer demand suggest housing activity remains subdued.

Internationally, we expect Canadian inflation to ease modestly, while U.K. inflation and labor market data should provide insight into whether underlying price pressures remain persistent. We anticipate the ECB will leave rates unchanged while maintaining a cautious stance on inflation. In Australia, labor market data are unlikely to materially alter the outlook for further policy tightening. In Japan, inflation data will be closely watched for signs that price growth is holding up. Among emerging markets, Mexico’s economic activity data should provide insight into whether growth is stabilizing after a soft start to the year.

- United States: New Home Sales (Friday)

- G10 Economies: Canada CPI (Monday), U.K. CPI + Labor Force Survey (Wednesday), European Central Bank Deposit Rate (Thursday), Australia Labor Force Survey (Thursday), Japan CPI (Friday)

- Emerging Markets: Mexico Economic Activity (Thursday)

U.S. Week Ahead

New Home Sales • Friday

We anticipate that new home sales rose 2.9% in June. Transactions appear poised for an improvement following back-to-back slips in April and May. That said, our expectation for a 597K annual pace of sales is still quite sluggish.

Inflation stemming from the U.S.-Iran war lifted the 30-year mortgage rate to 6.5% on average in June. Mortgage applications for purchase ticked up slightly over the month, but remained much lower than the trend at the close of 2025. Builders also continued to report poor sales conditions and weak buyer traffic, according to the NAHB. We see scope for new home sales to modestly strengthen this year as global price shocks fade and longer-term interest rates come down somewhat, especially as builders continue to utilize price cuts and other sales incentives. However, a meaningful acceleration in activity is unlikely.

G10 Week Ahead

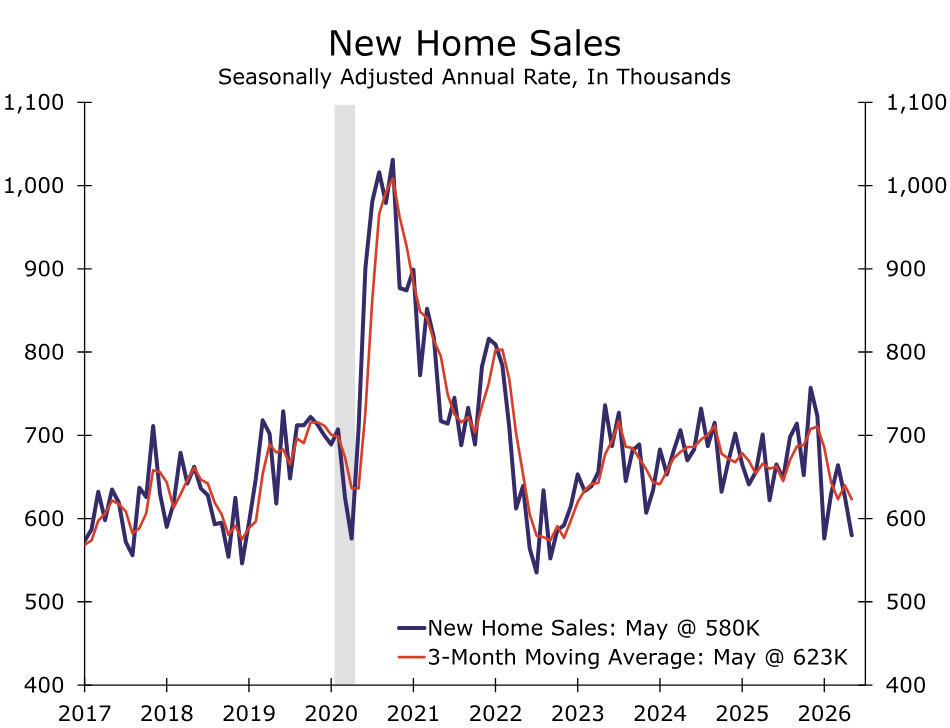

Canada CPI • Monday

Underlying consumer inflation pressures remain relatively contained in Canada despite the recent upward move in headline prices stemming from higher oil costs. Importantly, measures of core inflation have shown little sign of broadening price pressures, with both the trimmed mean and weighted median measures moving sideways at or near 2% in May. The breadth of inflation has also narrowed with the share of CPI components growing above 3% falling back close to its historical average in recent months.

Inflation expectations also remain generally anchored, according to the Bank of Canada’s (BoC) latest Q2 Survey of Consumer Expectations. While near-term inflation expectations remain somewhat elevated compared to prior to the pandemic, they’re not showing signs of moving meaningfully higher. Five-year ahead expectations have inched up, but remain well within normal ranges.

We look for headline CPI to drop modestly in June amid the move lower in oil prices leading the year-ago rate to 3.0%. Core measures should, however, remain near recent months pace of about 2.0%. The BoC elected to keep rates steady at this past week’s monetary policy meeting, and we expect it to continue to look through commodity-driven price increases unless they begin to feed more meaningfully into underlying inflation trends.

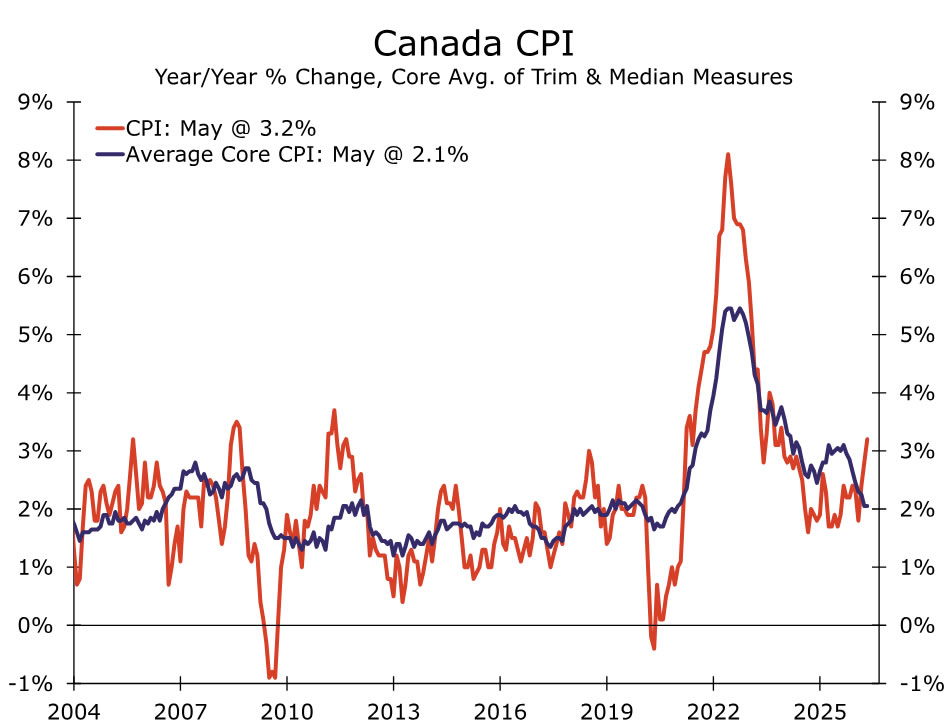

U.K. CPI + Labor Force Survey • Wednesday

The UK’s June CPI and May labor market data are due next week and should provide further insight into the Bank of England’s (BoE) policy outlook. We expect headline inflation to ease to 2.7% year over year from 2.8% in May, while core inflation edges down to 2.5% from 2.6%. Services inflation should also moderate to 3.6%, helped in part by lower airfares. Lower energy prices in June and the Ofgem price cap mechanism should provide additional support to disinflation.

The labor market also appears to be stabilizing. Consensus expectations are for the unemployment rate to remain unchanged at 4.9%, while regular pay growth, excluding bonuses, is likely to hold near April’s pace of 3.4% year over year on a three-month average basis. Wage growth has continued to ease and remains below the BoE’s projections, though services inflation and household inflation expectations remain elevated.

A softer labor market should reinforce the Monetary Policy Committee’s cautious approach, particularly given the weak growth backdrop. However, policymakers are unlikely to place too much weight on a few favorable inflation prints, especially as recent energy price increases and renewed Middle East tensions have yet to fully filter through to the data. While we recently lowered our forecast from two rate hikes to one, we continue to see tightening risks. Our base case is now for a single hike in Q4, though a move in late Q3 remains possible if inflation pressures prove more persistent than expected.

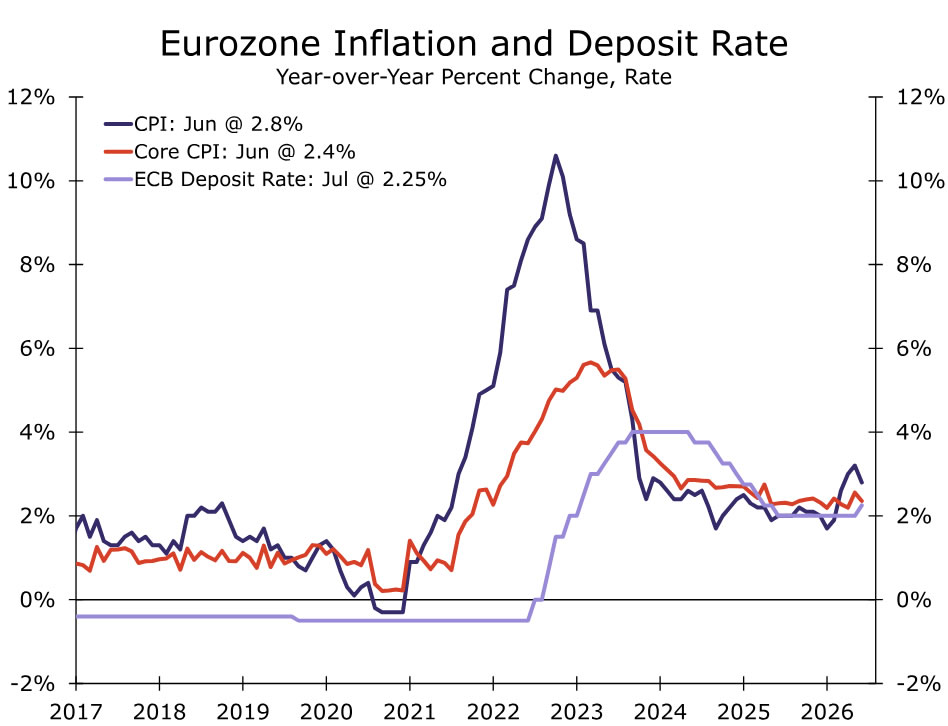

European Central Bank Deposit Rate • Thursday

We expect the European Central Bank (ECB) to leave rates unchanged next week, keeping the Deposit Rate at 2.25%. While inflation remains above the ECB’s 2% target, recent data have been encouraging, with June headline and core inflation moderating from earlier highs. However, renewed tensions in the Middle East continue to pose upside risks to energy prices, which could complicate the disinflation process and delay further progress in underlying inflation.

The ECB’s relatively hawkish tone comes despite the slowing growth backdrop. Wavering consumer confidence, moderating wage growth, and soft forward-looking PMI surveys suggest activity may remain subdued across the euro area. Economic weakness has been concentrated in Germany, where industrial activity and external demand remain under pressure, while service and tourism economies such as Spain have shown more resilience. An uneven growth picture complicates the outlook but is unlikely to outweigh the ECB’s priority of ensuring inflation returns to target.

Easing inflation pressures support a hold next week, but we do not expect the ECB to signal that the inflation fight is over. We continue to expect one additional 25 bps hike later in Q3, likely September, although incoming inflation, wage, and energy data will remain critical to that outlook.

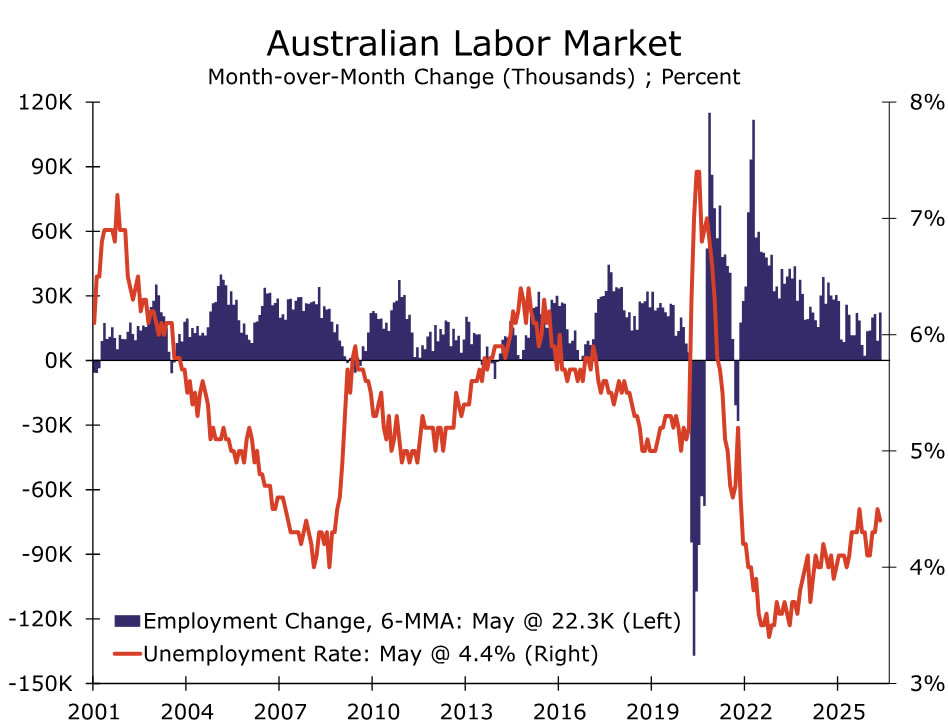

Australia Labor Force Survey • Thursday

Australia’s June employment report is due next week and will provide the final labor market reading before the Reserve Bank of Australia’s (RBA) August meeting. May employment rose 40.3K, although the details were less encouraging. Job gains were concentrated in part-time work, hours worked declined, and revised data showed underemployment was higher than initially reported. Recent labor market data have also been affected by revisions to population estimates and temporary seasonal distortions, leaving a less robust picture than the headline figures suggest. Business surveys and job ads also point to some moderation in labor market momentum.

Even so, we do not expect next week’s employment data to materially alter the RBA’s broader policy outlook. Policymakers have remained clear in recent speeches and post-meeting communications that inflation remains the primary concern and that further tightening may still be required. The June CPI release remains the more important input ahead of the August meeting. A softer inflation outcome could support another hold, but the recent outbreak of hostilities in the Middle East has increased the risk of renewed energy price pressures and delayed progress on disinflation.

As such, we continue to expect the RBA to deliver a 25 bp rate hike in Q3. August remains our base case, although a softer inflation print could push the move to September. Either way, policymakers appear committed to a front-loaded approach to ensure inflation returns to target.

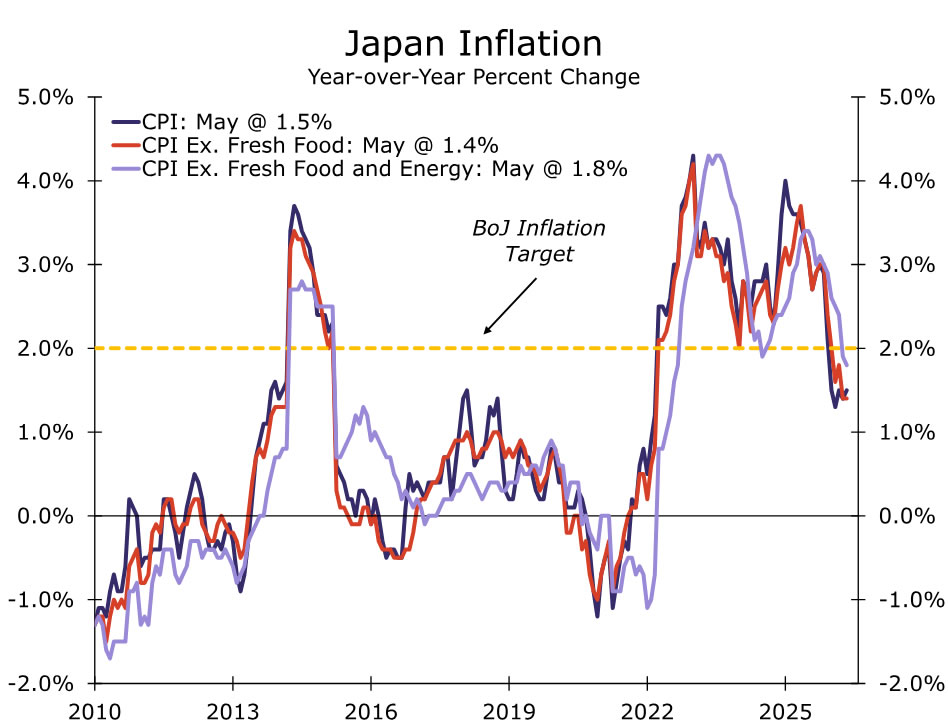

Japan CPI • Friday

Japan’s June CPI release is due next week and should provide another test of whether underlying inflation remains strong enough to support further policy normalization. In recent months, inflation has moderated substantially where headline CPI is currently around 1.5% year over year in May, while core-core, the Bank of Japan’s (BoJ) preferred gauge, has also trended lower to 1.8% year over year.

The BoJ’s wage-price narrative remains somewhat mixed since labor cash earnings came in softer than expected, raising questions whether strong wage negotiations are fully translating into realized income growth. However, Tokyo CPI firmed in June at 1.7% year over year, providing a constructive signal given its strong historical relationship with nationwide CPI. Domestic demand indicators have also shown some improvement, with household spending strengthening on a sequential basis and services activity remaining supported by resilient PMI and non-manufacturing Tankan readings.

Even with inflation softer this year, the case for normalization remains intact. Policymakers are likely to focus on underlying inflation measures and wage developments, rather than headline CPI alone, particularly as energy-driven price swings can distort the near-term picture. Combined with strong Q1 GDP growth and a solid Q2 Tankan survey, a firmer inflation print would strengthen the case for further tightening. We continue to expect the BoJ to raise rates by 25 bps in Q4, most likely in October, bringing the policy rate to 1.25% by year-end.

EM Week Ahead

Mexico Economic Activity • Thursday

Next week’s Economic Activity release for Mexico should provide further insight into whether growth stabilized in Q2 following a weak Q1. As a timely proxy for GDP, the data will help determine whether activity remains concentrated in services or is beginning to broaden into manufacturing.

Recent data suggests that services continue to support activity, aided by resilient retail sales and remittance inflows despite consumer confidence, wage growth and labor market conditions softening. The manufacturing outlook remains more nuanced. While industrial production has stayed subdued, manufacturing PMI has improved and U.S. manufacturing activity has generally remained resilient, raising the possibility that industrial activity is beginning to bottom out. That said, Mexico’s manufacturing sector is still highly dependent on the U.S. cycle and faces ongoing uncertainty surrounding USMCA negotiations. We continue to expect that nearshoring momentum will gradually fade, which could weigh on investment and limit the scope for a broader manufacturing recovery.

We do not expect the release to materially alter Banxico’s outlook and continue to expect rates to remain on hold at 6.50% through 2027. However, evidence of stronger and broadly based growth would reinforce the case for policymakers to remain comfortably on hold, while signs of renewed weakness could strengthen expectations for an eventual rate cut.