The stock market has witnessed considerable volatility over the past fortnight. From 81,867 on August 1, the Sensex fell to 78,593 on August 6, before recovering to 80,436 by August 16. While investors have weathered the recent bout, they should be prepared for similar episodes in the future.

Hit by global cues

A rapid appreciation of the yen in early August triggered a global sell-off. “Investors borrowed yen at Japan’s low interest rates and invested in higher-yielding assets abroad. However, as concerns that the Bank of Japan may tighten stance emerged, the yen began to strengthen. This led to an unwinding of some carry trades, causing sharp corrections,” says Manuj Jain, associate director, co-head product strategy, WhiteOak Capital Mutual Fund.

"Chart")

The Indian market is susceptible. “Having not experienced a significant correction since March 2023, it is more sensitive to negative news due to high valuations,” says Neelesh Surana, chief investment officer (CIO), Mirae Asset Investment Managers (India).

Held up by retail flows

Negative news from abroad (global growth concerns, wars, etc.) could affect the market in the near future. Year-to-date, foreign portfolio investors are net buyers of Indian equities to the tune of Rs 16,123 crore. But they are prone to sell Indian equities in

large quantities.

Expensive valuations in certain market segments are a cause for concern. The Nifty 50 is trading at a forward price-to-earnings (P/E) ratio of 20.6, in line with its 10-year average. However, the Nifty Mid-Cap 150 is trading at a premium (31.3 currently against the long-term average of 18.5), as is the Nifty Smallcap 250 (22 versus 18.1).

Clouding the outlook is slowing earnings growth. According to a recent Business Standard report, the combined net profit of 2,909 companies which have so far declared their first-quarter results for fiscal year 2024-25, is up a meagre 4.4 per cent year-on-year, the slowest in six quarters.

“In some narrow segments of the market, stock prices are factoring in high earnings in the coming years. Any disappointment may dampen investor sentiment,” says Jain.

On the positive side, India’s macroeconomic fundamentals are sound and retail flows remain stable. “During the June quarter, retail direct flows, including systematic investment plans (SIPs), was at an all-time high of about $19 billion (about Rs 1.59 trillion). While volatility may persist, strong retail investment could provide stability,” says Surana.

The latest data from the US on jobless claims and retail sales has reignited hopes that the US may not fall into

a recession.

MF investors: Displaying recency bias

During bull markets, investors fall prey to recency bias and invest heavily in sector, thematic, and momentum-based schemes. This one is no exception. “Investors tend to select funds based on latest performance with little attention to risk and volatility. Feeding into these funds are large inflows coming via SIP flows, mostly channelled via platforms and ‘do it yourself’ investors,” says Kavitha Menon, Sebi registered investment advisor and ARIA board member.

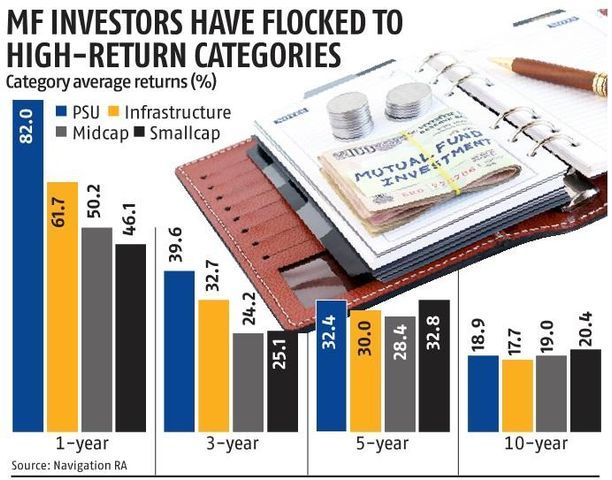

Fund houses have launched a large number of new fund offers (NFOs) belonging to sector and thematic categories, such as infrastructure, auto and manufacturing, which have captured most of the inflows. Jain informs that over the past 12 months (as of July 31, 2024) 38 per cent of total active equity mutual fund net flows were directed into sectoral/thematic funds

while another 12 per cent went into small cap funds.

Review and rebalance

Investors must review their portfolios. “If their allocation to certain segments have become high due to strong returns over the past three-four years, they should rebalance their portfolios and bring them in line with their long-term asset allocation,” says George Thomas, equity fund manager, Quantum Asset Management Company (AMC). He suggests having a healthy mix of large, mid, and small-cap allocation.

Do not expect the high returns from certain sector and thematic strategies to continue. Emphasising that winners rotate, Jain suggests directing fresh investments into parts of the market that are still available at relatively reasonable valuations, but have underperformed recently despite yielding reasonable earnings growth in the past few years.

Direct equity investors: Chasing momentum

Many new investors are chasing stocks displaying high momentum. Others are underestimating the risks that high valuations, especially in small and midcap stocks, pose.

“Overexposure to these volatile segments, driven by short-term gains, can lead to significant losses during corrections. Many also try to time the market, buying speculative stocks without understanding their intrinsic value or long-term potential,” warns

Tarun Birani, founder, TBNG Capital Advisors.

Adds Vikram Kasat, head advisory, PL-Capital, Prabhudas Lilladher: “Driven by FOMO (fear of missing out), investors buy at unreasonable valuations, causing low-quality stocks to become overpriced.”

Investors need to return to first principles. “Thoroughly research any company before investing. Evaluate management quality, business strength, and valuation,” says Master.

He adds that investors must adopt a long-term approach and invest in high-quality companies available at reasonable valuations.

First Published: Aug 18 2024 | 10:14 PM IST