Key Takeaways

- Deal activity: U.S. PE entered 2026 with real momentum, driven by improving financing conditions, a backlog of delayed processes, and sustained demand for scaled, high-conviction assets. Activity became more selective as the quarter progressed, however, as SaaS volatility, the war in Iran, and stress in private credit made buyers more disciplined on timing, price, and financing.

- Industry trends: Software underwriting has become more cautious as sponsors reassess the impact of AI on the landscape. In contrast, capital is rotating toward sectors with more visible cash flows and lower disruption risk, including professional services, finance, and construction, as well as “HALO” assets tied to AI deployment.

- Exits: The exit market is improving, but it is not fully reopened. Sponsors have more pathways than they did in 2023, including selective IPO windows, but exits remain concentrated in premium assets and tailored processes.

U.S. PE Deal Activity

Strong start, more selective finish: U.S. PE entered 2026 with real momentum, driven by improving financing conditions, a backlog of delayed processes, and sustained demand for scaled, high-conviction assets. But activity became more selective as the quarter wore on due to various headwinds. Public-market volatility among SaaS companies affected valuation in the tech sector, geopolitical uncertainty tied to the war in Iran made buyers increasingly disciplined on timing and price, and the stress in the private credit markets reshaped deal economics due to tighter financing.

Mega deals are masking a narrower market underneath: While headline activity remained solid, much of the market’s resilience continues to be driven by the top end. Large, differentiated assets can still attract capital, but the broader market remains bifurcated, with traditional software, cyclical businesses and harder-to-underwrite stories facing a higher bar to clear.

Mega-deal activity remains concentrated in scarce, financeable assets: The continued rise in $5Bn+ transactions underscores that capital is still available for scaled businesses with durable cash flows, strategic relevance or infrastructure-like characteristics, even if the broader market remains more selective.

Large deal mix skews to exits and energy: The largest announced deals were primarily exits and take-privates, with energy-related assets accounting for four of the top 10 transactions and totaling over $55 billion.

| Date | Acquiror | Target | Value ($Bn) | Industry | Deal Type |

|---|---|---|---|---|---|

| Mar, 2026 | GIP, EQT, CalPERS, QIA | AES | $38.4 | Utility & Energy | Take private |

| Mar, 2026 | Sysco Corp | Restaurant Depot (Leonard Green) | $29.1 | Retail | Exit |

| Mar, 2026 | Eli Lilly & Co | Centessa Pharmaceuticals (General Atlantic) | $9.0 | Healthcare | Exit |

| Feb, 2026 | Mubadala Capital, TWG Global | Clear Channel Outdoor Holdings | $7.8 | Professional Services | Take private |

| Jan, 2026 | Mitsubishi Corp | Aethon (OOTP, RedBird Capital) | $7.5 | Oil & Gas | Exit |

| Jan, 2026 | HgCapital, General Atlantic, Tidemark | OneStream (KKR) | $6.4 | Tech | Take private |

| Mar, 2026 | Thoma Bravo | WWEX Group (Providence Equity Partners, PSG, Ridgemont) | $5.0 | Transportation | Exit / Secondary buyout |

| Mar, 2026 | LS Power Equity Advisors | PJM Interconnection | $5.0 | Utility & Energy | Divestiture |

| Jan, 2026 | Vistra Corp | Cogentrix Energy (Quantum Energy Partners) | $4.7 | Utility & Energy | Exit |

| Feb, 2026 | Covetrus Inc | MWI Veterinary Supply | $3.5 | Healthcare | Portfolio |

Source: Dealogic, U.S. deals only, based on filing / announcement date. Data pulled on 4/14/2026.

![]()

Industry Trends

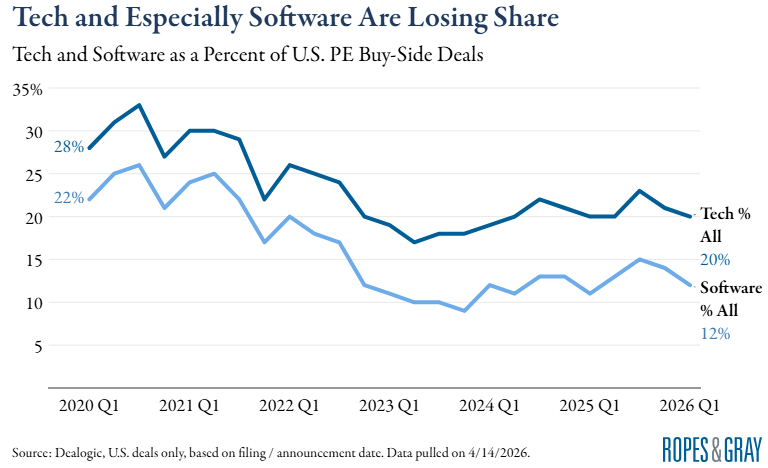

Software’s share of buy-side activity continues to reset: Relative to the 2020–2021 peak, sponsors are underwriting software more cautiously as investors reassess how AI will reshape product differentiation, pricing power and customer stickiness across application-layer businesses.

Capital is rotating toward sectors with more visible cash flows and lower disruption risk: Professional services, financials and construction have gained share over the last six years as sponsors favor businesses tied to outsourcing, compliance, infrastructure spending and mission-critical execution, which are areas that can offer more predictable demand than sectors still working through the broader software reset.

Exit Activity

Exit market is improving, but it is not fully reopened: Sponsors have more pathways than they did in 2023, but a meaningful valuation gap persists in many sectors and buyers remain highly selective. The market is reopening first for premium assets and tailored processes, rather than through a broad-based normalization of exits.

IPO window reopened selectively, then narrowed again: Early-quarter issuance suggested improving receptivity, but late-quarter volatility and renewed geopolitical tension quickly reinforced that public exits remain selective.

Continuation vehicles remain a useful tool, not a substitute for a broader exit recovery: Sponsors continue to use single-asset vehicles to hold onto their strongest companies for longer, but lower Q1 volumes suggest that continuation capital is not fully offsetting the slower pace of traditional sponsor exits.

Q1 2026 U.S. PE-Backed IPOs

|

Date |

Company | Sponsor | Deal Value ($Bn) | Industry |

|---|---|---|---|---|

| February 10, 2026 | SOLV Energy Inc | American Securities LLC | $513 | Construction/Building |

| February 4, 2026 | Bob’s Discount Furniture Inc | Bain Capital LP | $331 | Retail |

| February 4, 2026 | Forgent Power Solutions Inc | Neos Partners LP | $1,512 | Machinery |

| January 28, 2026 | York Space Systems Inc | AE Industrial Partners LP | $629 | Aerospace |

Source: Dealogic, U.S. Exchanges only, based on pricing date. Data pulled on 4/14/2026

Deal Dynamics

Financing markets have reopened faster than valuation expectations: Credit has returned for high-quality sponsor-backed transactions, particularly at the upper end of the market, enabling processes to move forward even as equity underwriting remains cautious. Multiples have improved modestly, but not enough to fully close the gap between seller expectations and buyer return hurdles, especially in sectors exposed to earnings volatility or technology-led disruption.

The result is a bifurcated deal environment: High-quality assets with resilient cash flows, lender support and a clear value-creation story can still command competitive processes, while weaker credits or harder-to-underwrite businesses continue to face tighter structures and a smaller buyer universe.

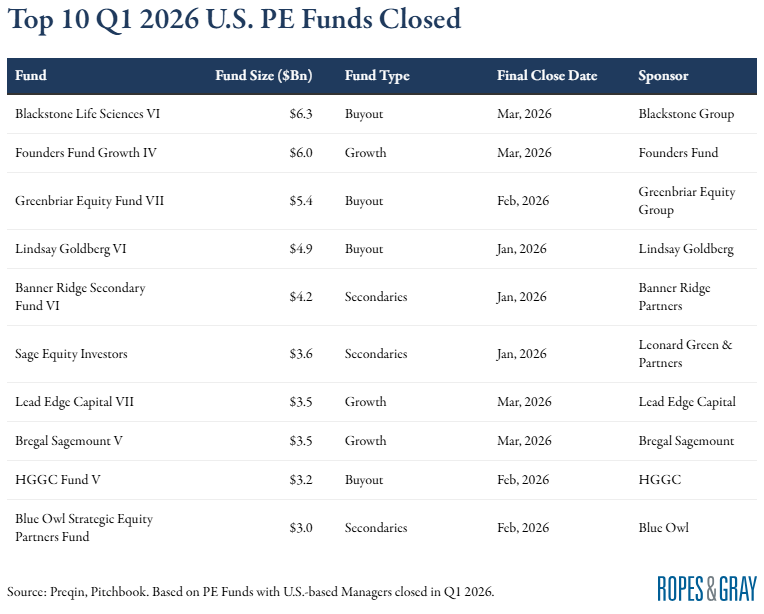

Fundraising Trends

Fundraising appears to be stabilizing, but it is not getting materially easier: Q1 suggests the market may be finding a floor, yet LPs remain selective and continue to prioritize managers with strong track records, differentiated sourcing, and a credible path to realizations.

Capital continues to consolidate around scale and specialization: The concentration of capital among the largest funds reflects an LP market that is still rewarding established platforms, while also favoring strategies such as growth and secondaries that can deploy capital more selectively in an uneven exit environment.

A Look Ahead

- Growing Attraction of “HALO” Assets: As AI continues to drive deal activity, investors are rotating toward tangible enablers such as data centers, power, semiconductors, and connectivity. Heavy-Asset, Low-Obsolescence (HALO) assets are becoming increasingly attractive in this environment, as they support AI deployment and offer more controllable value creation, visible demand and contracted, mission-critical revenues relative to asset-light models facing technological disruption.

- Software underwriting is being recalibrated for an AI-native world: Buyers are placing greater emphasis on workflow ownership, data advantages, and pricing durability as agentic AI begins to challenge traditional software interfaces and seat-based revenue models.

- Defense, cybersecurity, and critical infrastructure are emerging as core private capital themes: Heightened geopolitical tension is expanding focus on defense technology, aerospace, cyber resilience, and supply-chain security, with investors increasingly aligning around sectors linked to national security.

- The Iran war is now influencing both the macro backdrop and deal execution: The conflict has heightened volatility across energy and shipping markets, complicating the inflation and rates outlook and, in turn, affecting financing costs, valuation confidence, and transaction timing. In M&A, that has translated into slower processes, more diligence, and tighter buyer discipline, particularly in sectors exposed to commodity costs, supply chains, or cross-border risk.

- Credit markets remain open, but underwriting is increasingly selective: Lenders are constructive on stronger credits, but weaker businesses are facing wider spreads, tighter documentation, and a higher threshold for leverage.

- Exit markets should continue to improve gradually rather than all at once: Sponsors are still most likely to monetize high-quality assets with resilient earnings and scarcity value, while broader portfolio exits will depend on a more durable recovery in valuations and public market stability.