Record Free Cash Flow Reveal a New Capital Allocation Playbook?")

- In April 2026, Kinross Gold Corporation reported first-quarter 2026 net income of US$843 million, more than double the prior year, with basic and diluted earnings per share from continuing operations rising to US$0.70, alongside a maintained quarterly dividend of US$0.04 per common share payable on June 4, 2026.

- Record free cash flow, higher realized gold prices, and ongoing progress at projects such as Great Bear and Lobo-Marte highlight Kinross Gold’s financial strength and project pipeline, while strong shareholder support for its board and executive pay underpins confidence in the company’s governance and long-term plan.

- Next, we’ll examine how Kinross Gold’s record free cash flow and reaffirmed guidance could influence its existing investment narrative and outlook.

Find 6 companies with promising cash flow potential yet trading below their fair value.

Kinross Gold Investment Narrative Recap

To stay invested in Kinross Gold, you need to believe its strong free cash flow and disciplined balance sheet can offset rising cost pressures and permitting risks across its global portfolio. The first quarter of 2026 supports that view financially, with record free cash flow and higher margins, but it does not materially change the near term catalyst of executing on projects like Great Bear and Lobo Marte or the key risk that cost inflation and regulatory delays could still erode those cash flows.

Among the recent announcements, Kinross reaffirming its 2026 production and cost guidance after a quarter of record free cash flow stands out. Holding to its 2.0 million ounce target and embedded 5% inflation assumption, while returning about US$300 million through dividends and buybacks, matters directly to the catalyst of consistent cash returns and project funding, and it gives investors more concrete parameters to watch as those development and cost risks play out.

Yet behind the strong quarter, investors should also be aware of the risk that rising all in sustaining costs could still compress margins if…

Read the full narrative on Kinross Gold (it’s free!)

Kinross Gold’s narrative projects $9.0 billion revenue and $3.0 billion earnings by 2029. This requires 8.3% yearly revenue growth and an earnings increase of about $0.6 billion from $2.4 billion today.

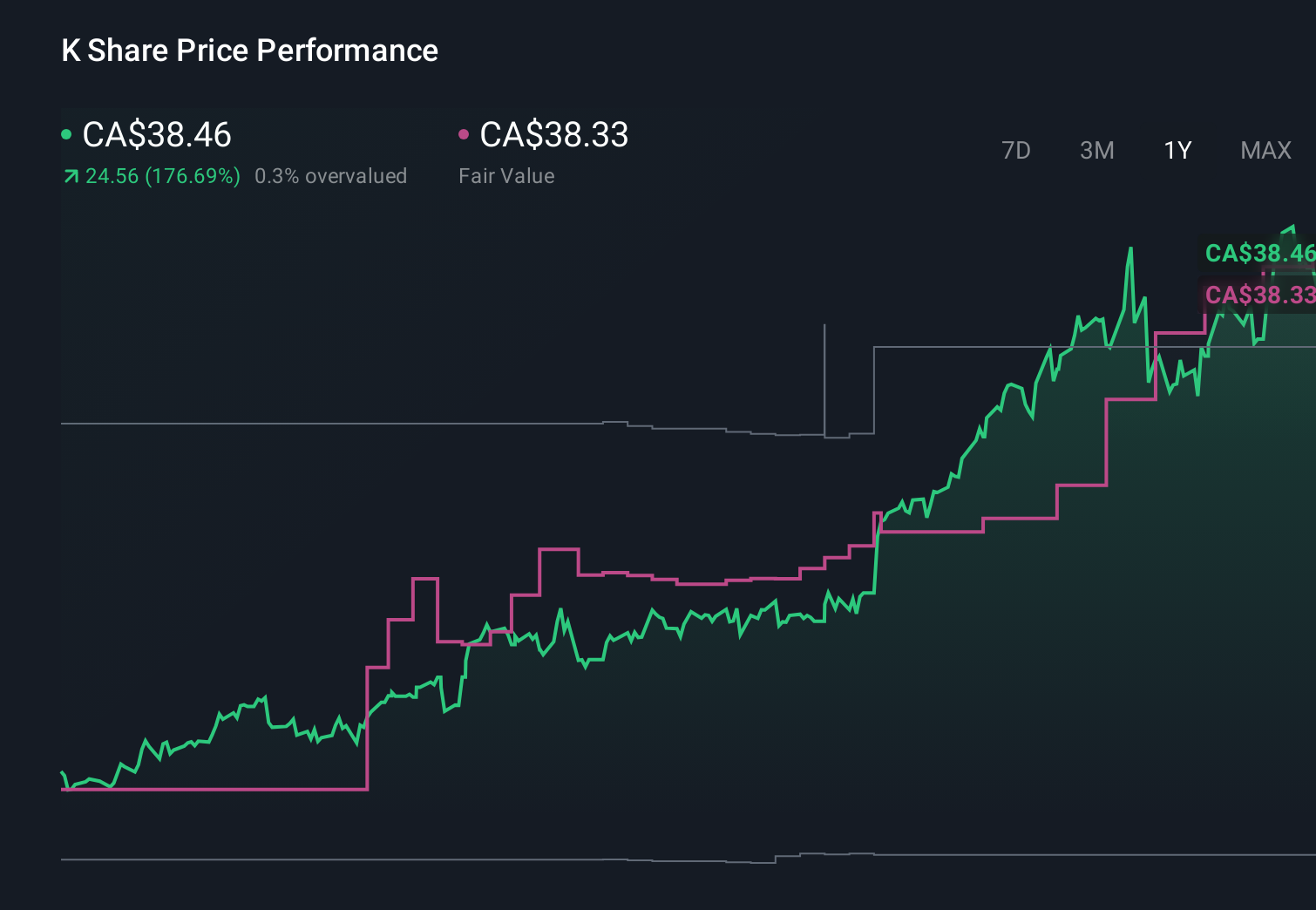

Uncover how Kinross Gold’s forecasts yield a CA$54.92 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue near US$7.4 billion and earnings around US$2.1 billion by 2028, so this quarter’s results could either support that upbeat view or expose its risks, depending on how you weigh cost pressures and geopolitical exposure in places like Mauritania and Brazil.

Explore 4 other fair value estimates on Kinross Gold – why the stock might be worth 44% less than the current price!

Form Your Own Verdict

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Looking For Alternative Opportunities?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Kinross Gold might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com