Fully Valued After Its Russell Index Removal?")

Royal Gold (RGLD) was removed from both the Russell 1000 Defensive Index and the Russell 1000 Value-Defensive Index on 27 June 2026. This change may influence how index-tracking funds hold the stock.

See our latest analysis for Royal Gold.

Royal Gold’s recent removal from the defensive indices comes as the stock trades at US$202.12, with the share price down 20.58% over 90 days and 9.96% over 30 days, even as the 1 year total shareholder return stands at 14.65% and the 5 year total shareholder return is 82.80%. This suggests that recent momentum has faded against a stronger longer term record.

If this shift in sentiment has you looking beyond a single precious metals stock, it could be a good moment to scan the wider gold space using our 33 elite gold producer stocks

With Royal Gold now trading well below some valuation estimates and after a sharp pullback despite solid multi year total returns, investors are left with a key question: is there genuine value on offer here, or has the market already priced in future growth?

Most Popular Narrative: 38.3% Undervalued

The most followed narrative puts Royal Gold’s fair value at $327.50, well above the last close at $202.12, which raises a clear question about what supports that gap.

The strategic acquisitions of Sandstorm Gold and Horizon Copper will significantly diversify Royal Gold’s asset base, reducing single-asset risk and increasing exposure to long-term growth projects, which should drive more stable and growing revenue streams and improve net margins. Recent investments in projects like the Kansanshi gold stream (with a multi-decade production profile) and the Warintza copper-gold-moly project (large-scale development potential in the early 2030s) position Royal Gold to benefit from increasing demand for gold (as a hedge against inflation and geopolitical risk) and copper (driven by electrification and renewable energy adoption), supporting higher long-term revenue and earnings growth.

This narrative leans heavily on compounding revenue, thicker margins, and a richer earnings multiple. Curious which specific long range assumptions have to come good to support that valuation?

Result: Fair Value of $327.50 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the Royal Gold narrative also leans on gold remaining supportive and key projects like Hod Maden delivering as planned, so weaker pricing or operational setbacks could quickly challenge it.

Find out about the key risks to this Royal Gold narrative.

Another View on Royal Gold’s Valuation

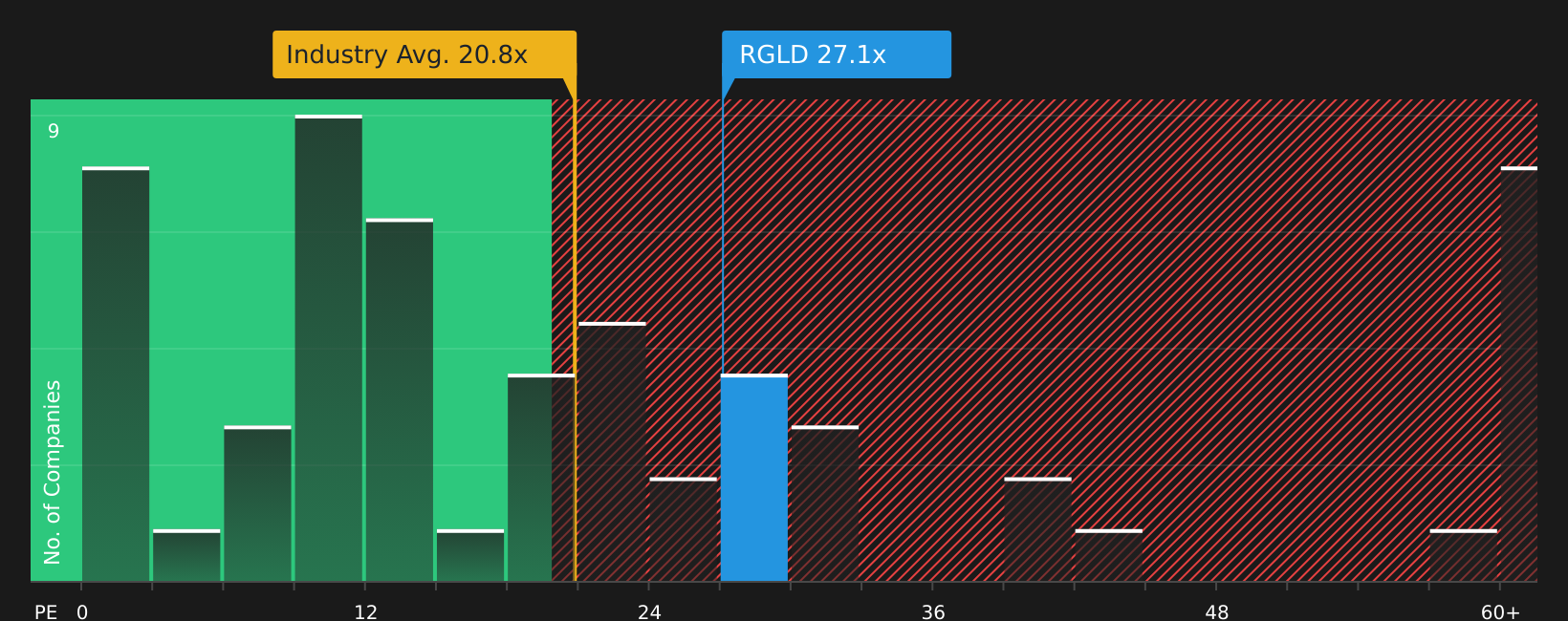

The earlier fair value for Royal Gold leans heavily on future earnings forecasts and a higher P/E in a few years’ time. On today’s numbers, the stock trades on a P/E of 27.1x, compared with 20.8x for the US Metals and Mining industry, 26.8x for peers, and a fair ratio of 24.5x.

That gap suggests the market already prices Royal Gold above both its sector and the fair ratio that the market could move toward. This may leave less room for error if growth or project delivery fall short.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed tone around Royal Gold has you wondering what to think, do not wait on the sidelines. Review the full picture of both concerns and potential upsides through the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Royal Gold?

If Royal Gold has sharpened your thinking about quality and timing, do not stop here, broaden your watchlist now and keep your options wide open.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com