Introduction & Market Context

Sanmina Corporation (NASDAQ:SANM) unveiled exceptional second quarter fiscal 2026 results on April 27, 2026, showcasing the transformative impact of its ZT Systems acquisition and surging demand for AI and cloud infrastructure solutions. The company’s stock rose 2.41% in aftermarket trading to $196.80, approaching its 52-week high of $197.63, as investors responded positively to results that significantly exceeded analyst expectations.

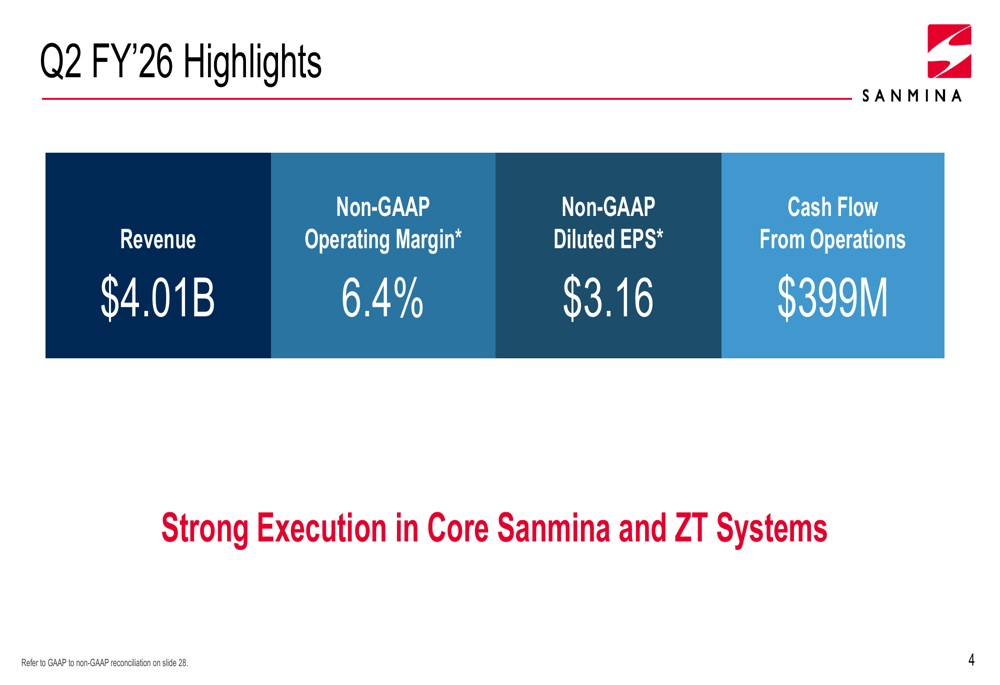

The electronics manufacturing services provider reported revenue of $4.01 billion and non-GAAP diluted earnings per share of $3.16, beating forecasts of $3.29 billion and $2.40, respectively. The performance marks a dramatic acceleration in Sanmina’s growth trajectory, driven primarily by the successful integration of ZT Systems and accelerated compute shipments for hyperscale data center customers.

Quarterly Performance Highlights

As shown in the following financial summary, Sanmina delivered robust results across all key metrics for the second quarter of fiscal 2026.

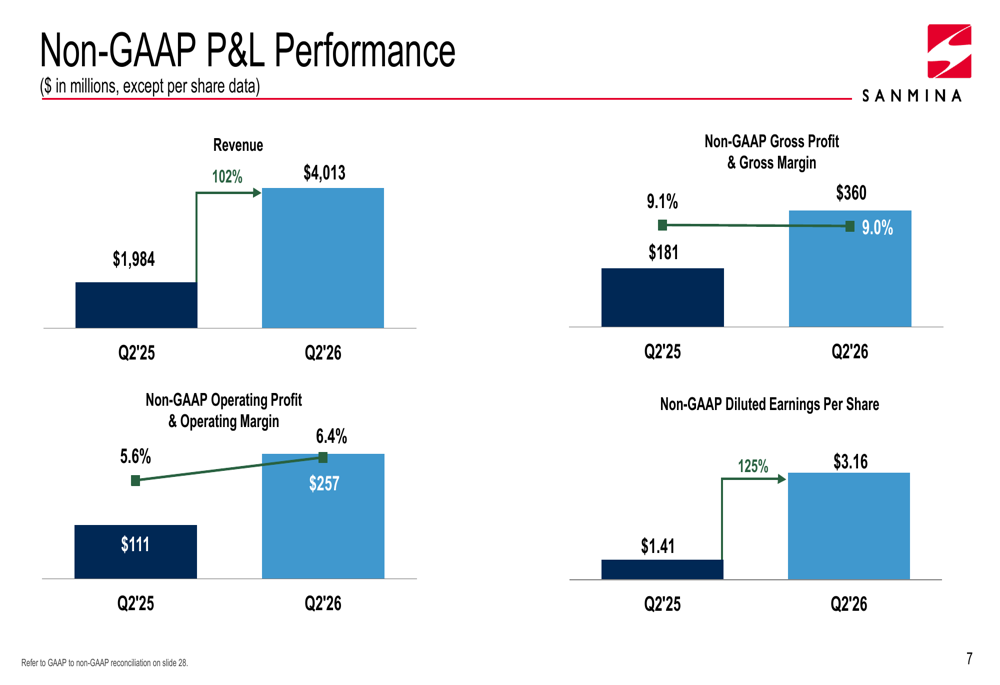

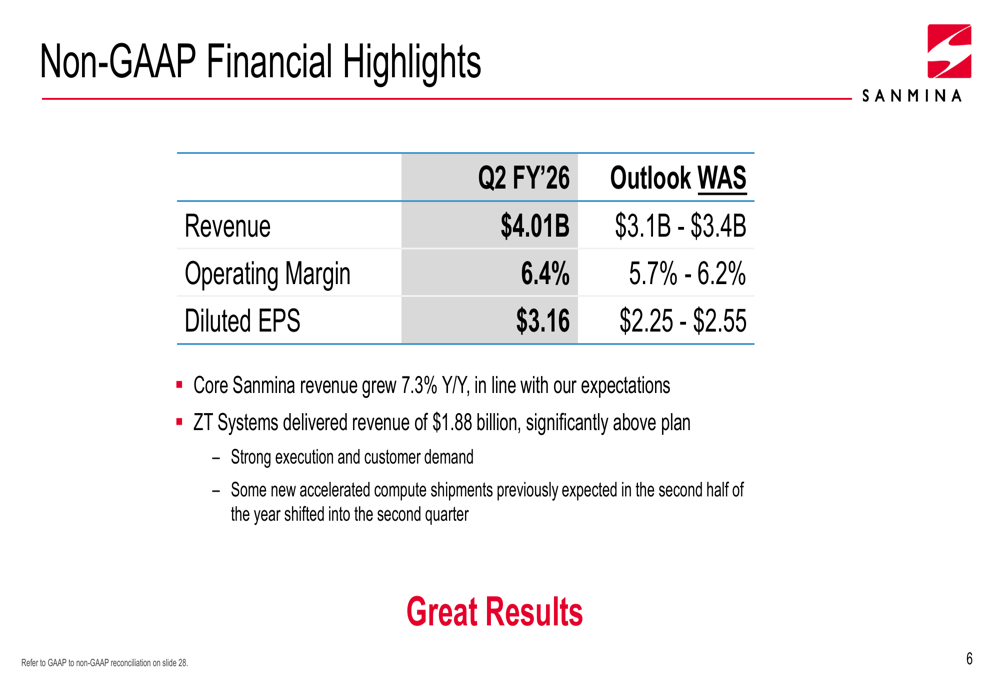

The company achieved revenue of $4.01 billion, representing a remarkable 102% year-over-year increase from $1.98 billion in Q2 FY’25. This growth significantly outpaced the company’s initial outlook range of $3.1 billion to $3.4 billion, driven by what management characterized as “strong execution in core Sanmina and ZT Systems.”

The following year-over-year comparison illustrates the magnitude of Sanmina’s growth across key financial metrics.

Non-GAAP operating margin expanded to 6.4% from 5.6% in the prior-year period, while operating profit surged 131% to $257 million. Most notably, non-GAAP diluted earnings per share jumped 125% to $3.16 from $1.41, substantially exceeding the company’s outlook range of $2.25 to $2.55.

ZT Systems Integration Drives Outperformance

The standout performance in Q2 was largely attributable to ZT Systems, which Sanmina acquired to expand its capabilities in accelerated compute and AI infrastructure. As detailed in the company’s results comparison, ZT Systems delivered $1.88 billion in revenue during the quarter, “significantly above plan.”

Management attributed the ZT Systems outperformance to strong execution, robust customer demand, and accelerated compute shipments that shifted from the second half of the fiscal year into Q2. Meanwhile, core Sanmina revenue grew 7.3% year-over-year, in line with expectations, demonstrating healthy underlying business momentum independent of the acquisition.

The company provided an update on its phased integration strategy, noting that it has largely completed the initial integration phase and is now focused on winning and shipping new accelerated compute business with key hyperscale and OEM customers. Management emphasized it is “executing to the plan” with the integration progressing smoothly.

Segment Performance & Market Diversification

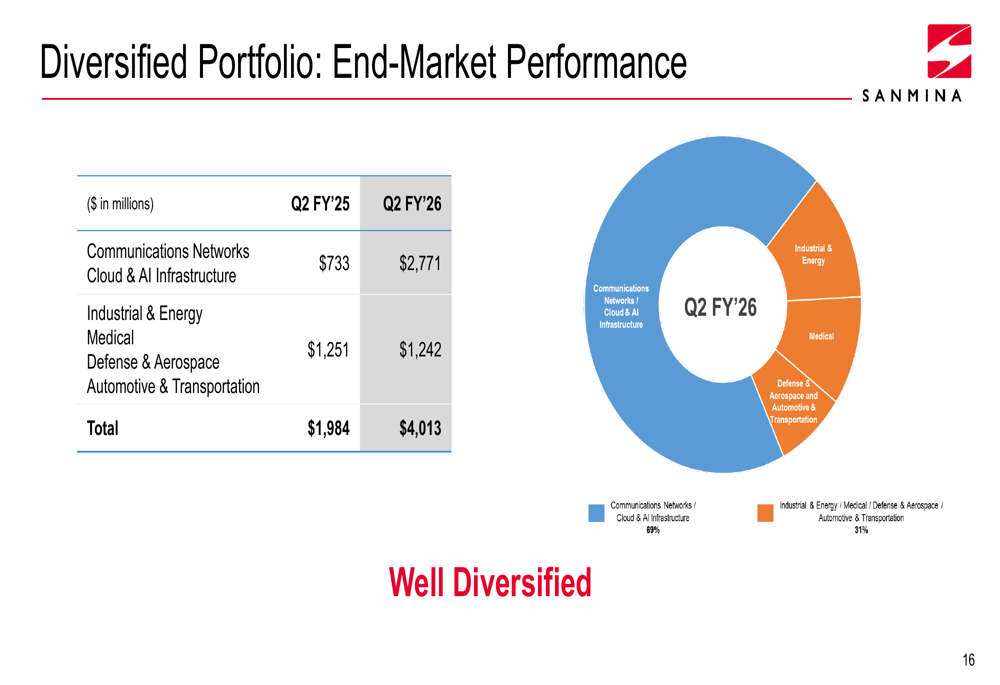

Sanmina’s diversified end-market portfolio remained a key strength, though the revenue mix shifted notably toward cloud and AI infrastructure following the ZT Systems acquisition. The following breakdown illustrates the company’s revenue distribution across end markets.

Communications Networks and Cloud & AI Infrastructure represented 69% of total revenue at $2.77 billion, up dramatically from $733 million in the prior-year quarter. The remaining 31% came from a diversified mix of Industrial & Energy, Medical, Defense & Aerospace, and Automotive & Transportation markets, which collectively generated $1.24 billion.

Breaking down performance by operating segment, the Integrated Manufacturing Solutions (IMS) division saw revenue surge to $3.58 billion from $1.60 billion, with gross margin improving to 8.5% from 7.7%. The Components, Products and Services (CPS) segment grew 12.2% year-over-year to $461 million, though gross margin compressed to 11.6% from 13.9% due to component shortages impacting timing of revenue and profitability for one product business.

Financial Strength & Capital Allocation

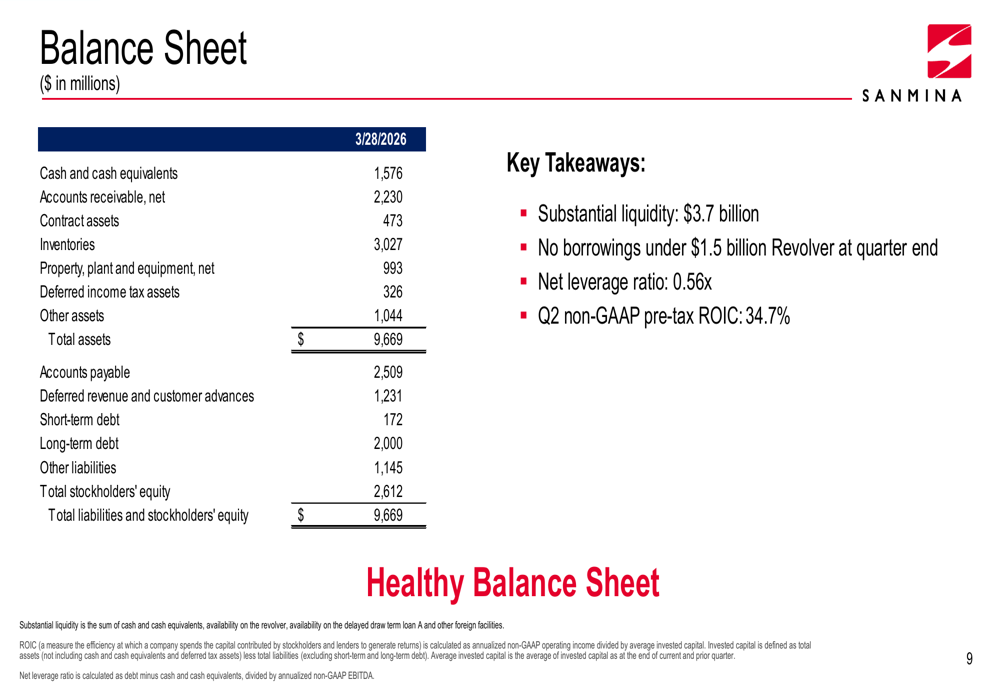

Sanmina’s balance sheet remained robust despite the significant capital deployed for the ZT Systems acquisition. As presented in the company’s financial position summary, total liquidity stood at $3.7 billion with no borrowings under its $1.5 billion revolving credit facility.

The company reported a net leverage ratio of just 0.56x and achieved a non-GAAP pre-tax return on invested capital of 34.7%, demonstrating efficient deployment of capital. Total debt stood at $2.17 billion against stockholders’ equity of $2.61 billion.

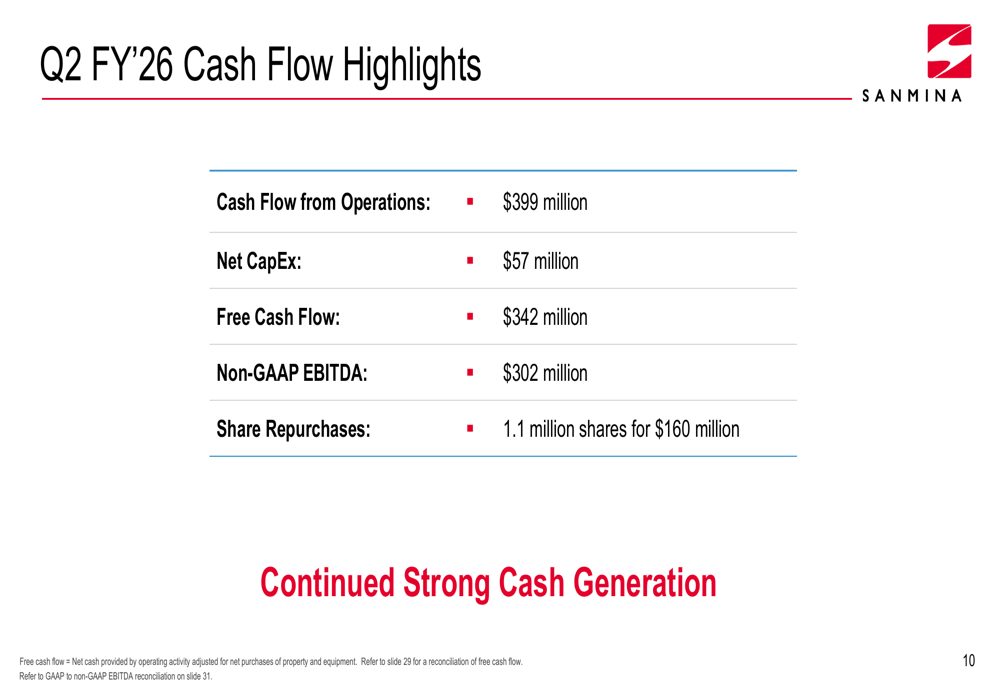

Cash generation remained strong, as illustrated in the following quarterly cash flow summary.

Operating cash flow reached $399 million, while free cash flow totaled $342 million after $57 million in net capital expenditures. The company repurchased 1.1 million shares for $160 million during the quarter, continuing its balanced capital allocation approach. Sanmina’s board authorized an additional $600 million for share repurchases, reflecting confidence in the company’s growth trajectory and cash generation capabilities.

Forward-Looking Guidance

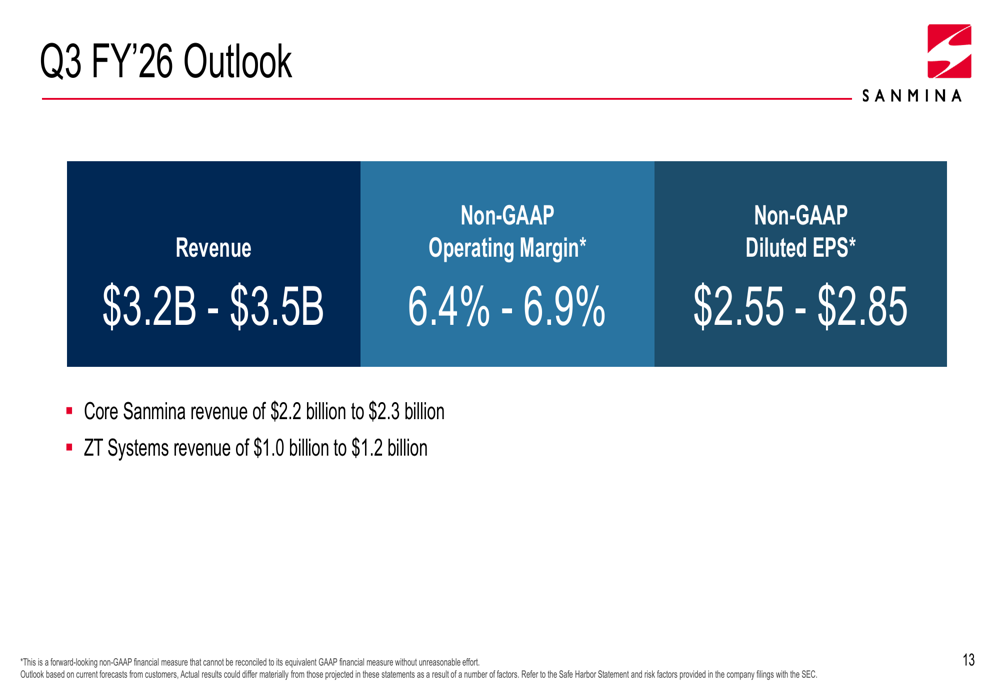

Management provided optimistic guidance for both the third quarter and full fiscal year 2026, projecting continued strong performance driven by AI infrastructure demand. The following outlook details the company’s expectations for Q3.

For the third quarter of fiscal 2026, Sanmina expects revenue between $3.2 billion and $3.5 billion, with non-GAAP operating margin of 6.4% to 6.9% and non-GAAP diluted EPS of $2.55 to $2.85. The midpoint of this guidance suggests sequential moderation from Q2’s exceptional performance, which management attributed to some revenue pulling forward from later quarters.

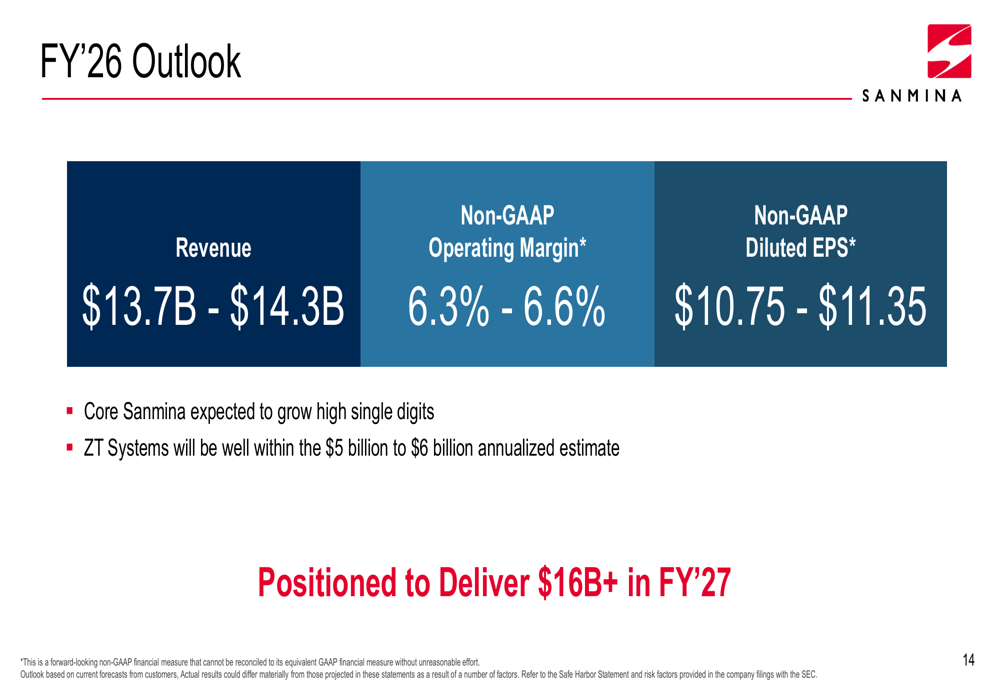

Looking at the full fiscal year, the company raised its outlook substantially based on the strong first-half performance.

Full-year fiscal 2026 revenue is now projected at $13.7 billion to $14.3 billion, with non-GAAP operating margin of 6.3% to 6.6% and non-GAAP diluted EPS of $10.75 to $11.35. Management highlighted that core Sanmina is expected to grow at a high single-digit rate, while ZT Systems revenue will be “well within” the previously estimated $5 billion to $6 billion annualized range.

Significantly, the company stated it is “positioned to deliver $16B+ in FY’27,” suggesting continued momentum beyond the current fiscal year as AI infrastructure investments accelerate across the technology sector.

Strategic Positioning & Capabilities

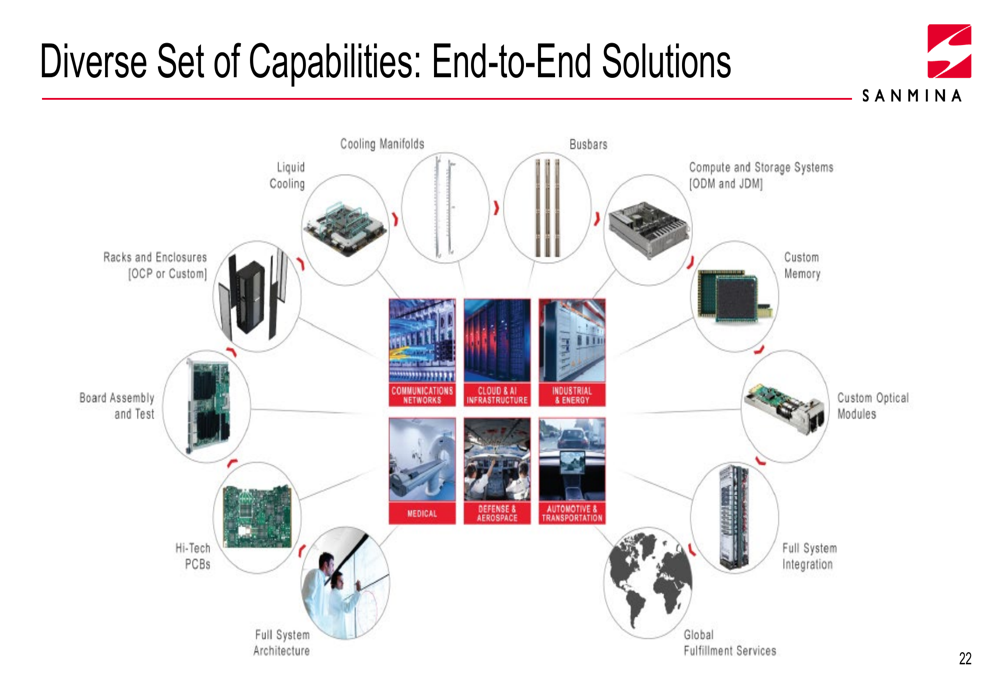

Sanmina emphasized its comprehensive end-to-end solutions capabilities as a key competitive differentiator in serving complex technology markets. The following infographic illustrates the company’s integrated approach across the value chain.

The company’s capabilities span from component-level manufacturing including liquid cooling systems, busbars, and custom optical modules through board assembly, system integration, and global fulfillment services. This vertical integration enables Sanmina to serve diverse end markets including communications networks, cloud and AI infrastructure, industrial and energy, medical, defense and aerospace, and automotive and transportation sectors.

Supporting these capabilities is Sanmina’s extensive global manufacturing footprint, strategically positioned to serve customers across major regions.

With manufacturing facilities spanning the Americas, Europe, and Asia, Sanmina maintains flexibility to support both global and regional supply chain strategies. The company’s substantial U.S. manufacturing presence positions it favorably amid ongoing discussions about supply chain resilience and potential trade policy changes.

Management highlighted several growth drivers across its diversified end markets, including AI-driven demand for communications networks and cloud infrastructure, expanding energy business for AI data centers, stable medical device markets, continued defense and aerospace growth, and programs transitioning from new product introduction to full-scale production in automotive and transportation.

Risks & Challenges

Despite the strong performance, Sanmina’s presentation acknowledged several risk factors that could impact future results. The company cited potential adverse changes in key cloud and AI infrastructure markets, tariff and trade policy impacts, reliance on a limited number of large customers, international operations risks, and geopolitical uncertainty including the Middle East conflict.

The concentration of revenue in cloud and AI infrastructure—now representing 69% of total revenue—creates potential vulnerability to any slowdown in hyperscale data center capital spending. Additionally, the company noted that component shortages impacted timing of revenue and profitability in one product business within its CPS segment, highlighting ongoing supply chain challenges.

With shares trading at a price-to-earnings ratio of approximately 45 based on the current fiscal year guidance, investors are pricing in continued strong execution and sustained demand for AI infrastructure solutions. The stock’s proximity to its 52-week high suggests limited margin for disappointment in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.