DavidLeshem

Introduction

On April 17, I wrote an article titled “Low Risk, High Return? The Power Of The 15-Stock Dividend Growth Portfolio.”

In that article, I discussed what makes dividend growth so special. In fact, we discussed what makes this strategy the best (proven!) strategy to build long-term wealth.

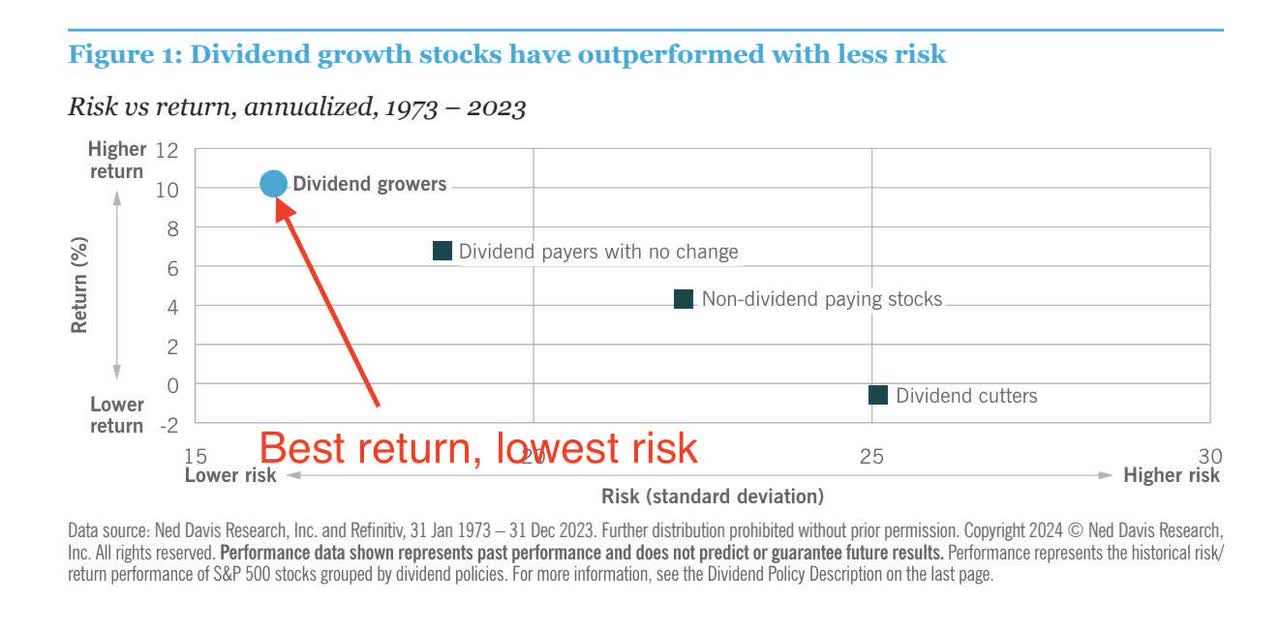

As we can see below, using data collected in the 1973-2023 period, dividend growers have seen the highest average annual return with the lowest standard deviation (the definition of “risk”).

The beauty of this is that it allows us to find higher returns in lower-risk areas, defying the notion that the higher the desired return, the more risk we need to take.

Nuveen

While the “average” dividend growth stock won’t let you compound your money 10-fold within a few years, the biggest factor is consistency. As I often like to say, investors who hunt for stocks that have the potential to quickly double will likely often run into stocks that don’t make it, which has the potential to significantly average the total result and add a lot of volatility.

According to Luisa Zhou:

- 9 out of 10 startups fail.

- 38% of startups fail because they run out of cash.

- 35% of startups fail because there is no market need for them.

- By year 5, 50% of all startups will have failed.

Although every single business comes with risks, proven dividend growth stocks do not have these issues, which brings me to the two main reasons why (I believe) dividend growth stocks have such a great history of superior returns with subdued risks.

This is what I wrote in the article I highlighted at the start of this article:

Strong financials and business models: Companies that can consistently raise their dividends typically have healthy finances, stable earnings, and a strong competitive advantage. This allows them to generate excess cash they can return to shareholders through dividends. Or, to put it differently, they have proven they can withstand the test of time.

Management discipline: A company’s decision to raise its dividend reflects a commitment to shareholder returns. This suggests that management is focused on long-term growth and profitability. After all, if you manage a company with a consistent track record, the focus shifts automatically to sustainable long-term growth.

In light of all of this, after many requests (thanks for those!), I decided to write this article, discussing how I would start a portfolio from scratch in this market environment.

By doing so, I kept a few things in mind:

- Usually, I would advise most people to stick to ETFs. However, as this is Seeking Alpha (the emphasis is on “alpha”), I know that many people buy individual stocks and have the skills to understand what they are buying.

- I have a focus on “never sell” stocks. While we’ll obviously sell our stocks at some point (unless the next generations inherit them), I like to apply the never-sell mindset to pick stocks that, I expect, will survive anything the market and economy throw at us. That would make this portfolio an ultra-low maintenance portfolio.

- I include both higher-yielding dividend stocks and lower-yielding dividend stocks with more growth to provide a portfolio that appeals to most investors.

- While backtesting always comes with a survivorship basis (I would be silly to include failed businesses in this portfolio), I expect all of these companies to keep outperforming the market.

So, let’s get to it!

A Bigger Focus On Safety And Value

Just like my prior dividend portfolio article, I want to briefly discuss two things I increasingly incorporate in my research:

- Value (buying attractive stocks in a market with an overall lofty valuation).

- Buying bullet-proof companies.

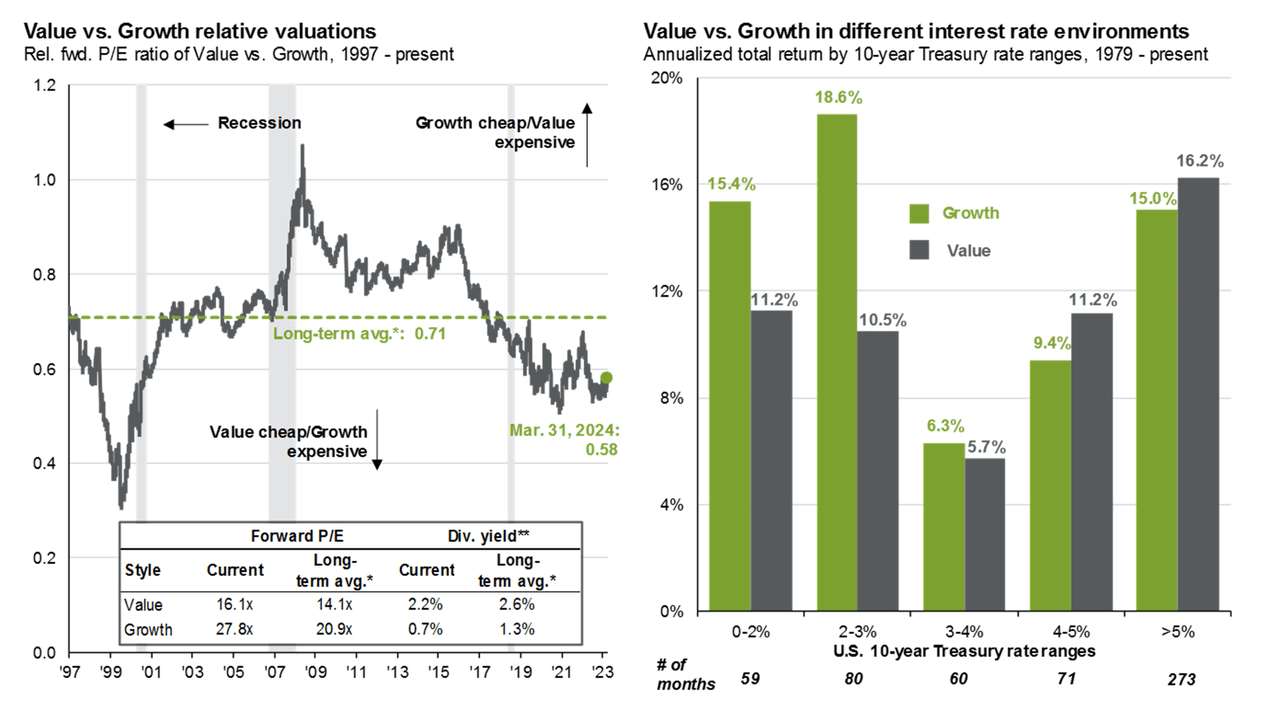

If you’re a regular reader, you will be familiar with the chart below, as I have used it in a number of articles in the past.

Essentially, what we are seeing is that value stocks are extremely attractive compared to growth stocks. While both trade above their long-term averages, growth stocks have run hot again since the market started to price in much lower inflation last year.

JPMorgan

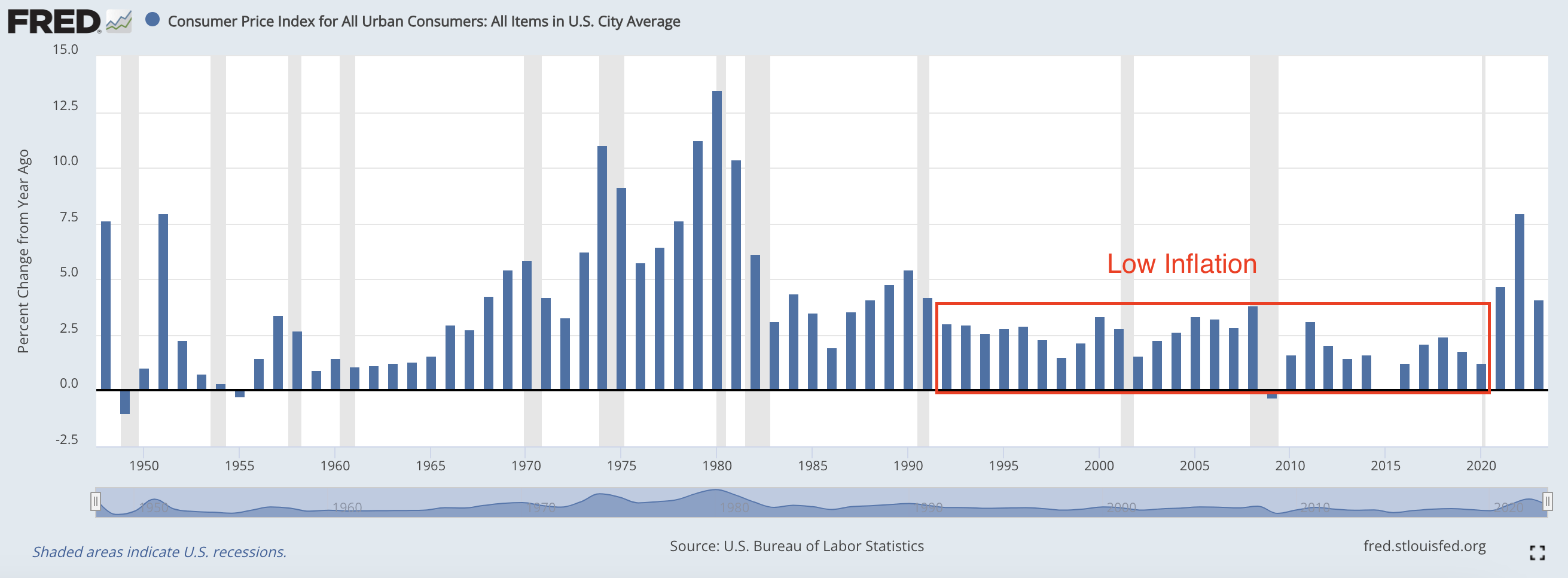

While it is somewhat obvious that inflation has come down from its peak (imagine if it hadn’t), I have been in the camp that expects inflation and interest rates to remain higher for longer, eventually leading to a situation where the Fed may be forced to pick protecting economic stability over fighting inflation.

Due to factors like de-globalization, structural labor shortages, a less favorable supply situation in oil, gas, and coal, and global geopolitical challenges, I expect that the period of subdued inflation between the early 1990s and 2021 will not be repeated anytime soon.

Federal Reserve Bank of St. Louis

As a result, I want to own corporations with pricing power, stellar balance sheets, and business models that come with elevated moats (with just a few exceptions) to protect investors against anything the market may throw at them.

In fact, the stocks in this article were picked based on their ability to give investors exposure to critical supply chains and economic areas while benefitting from both income and growth.

The Wide Moat Portfolio

If I had to start from scratch, I would likely buy every holding of my current 20-stock portfolio.

However, as I already mentioned, I decided to do things a bit differently in this article.

Not only am I focusing more on yield and safety, but I also decided to implement my view on the economy using just a few select stocks.

Furthermore, I decided to build a portfolio that I would be comfortable with if I had a full-time job that was not in the business I’m in now.

After all, I spend almost all day thinking about and working on (dividend) investments. Most people with a job in a different industry do not have the “luxury” to check on their portfolios almost on a 24/7 basis.

Hence, I decided to implement a strategy that I apply to a number of family accounts of people who are usually busy doing other stuff than checking their investments – but who still want single-stock exposure.

Here is the first overview of the portfolio:

Leo Nelissen

Here is an interactive table, including the tickers of the ETF and each stock:

| Weighting | Company | Industry | Dividend Yield | 5Y CAGR | Payout Ratio |

| 45% | Schwab U.S. Dividend Equity ETF (SCHD) | Dividend ETF | 3.50% | 11.80% | N/A |

| 5% | Waste Management Inc (WM) | Professional & Commercial Services | 1.50% | 3.30% | 45.2% |

| 5% | Union Pacific Corporation (UNP) | Freight & Logistics Services | 2.30% | 10.10% | 50.4% |

| 5% | Equity LifeStyle Properties Inc (ELS) | Residential & Commercial REIT | 2.90% | 10.00% | 63.5% |

| 5% | Home Depot Inc (HD) | Specialty Retailers | 2.70% | 13.90% | 56.4% |

| 5% | Johnson & Johnson (JNJ) | Pharmaceuticals | 3.40% | 5.80% | 45.5% |

| 5% | AbbVie Inc (ABBV) | Pharmaceuticals | 3.80% | 8.30% | 53.9% |

| 5% | Abbott Laboratories (ABT) | Healthcare Equipment & Supplies | 2.10% | 12.10% | 48.3% |

| 5% | CME Group Inc (CME)* | Investment Banking & Investment Services | 2.20% | 9.30% | 47.1% |

| 5% | Moody’s Corporation (MCO) | Professional & Commercial Services | 0.90% | 11.70% | 31.8% |

| 5% | Canadian Natural Resources Ltd (CNQ)* | Oil & Gas | 3.70% | 22.30% | 48.9% |

| 5% | Texas Instruments Inc (TXN) | Semiconductors & Semiconductor Equipment | 3.10% | 12.80% | 71.4% |

*= These companies pay special dividends that are not included in these numbers. Both usually distribute up to 100% of their free cash flow each year.

As we can see above, I decided to go with 45% exposure to the Schwab U.S. Dividend Equity ETF. This ETF is what I consider to be one of the best dividend ETFs on the market. It is well-diversified, has a juicy yield, and consistent dividend growth.

I also opted for this ETF instead of a dividend growth-focused ETF because I believe value-focused dividend stocks are likely in a better spot, benefitting from an attractive relative valuation, as I briefly discussed in this article.

I gave this ETF 45% exposure, which significantly contributed to its dividend profile, as the portfolio has an average yield of 2.7% and a weighted average 5-year dividend CAGR of more than 11%.

That said, I expect dividend growth to come down, as the economy is not as strong as it was during the past five years.

The 11 single stocks in the portfolio have a 5% weighting each.

I didn’t pick these stocks at “random” but based on the criteria I explained in the first part of this article.

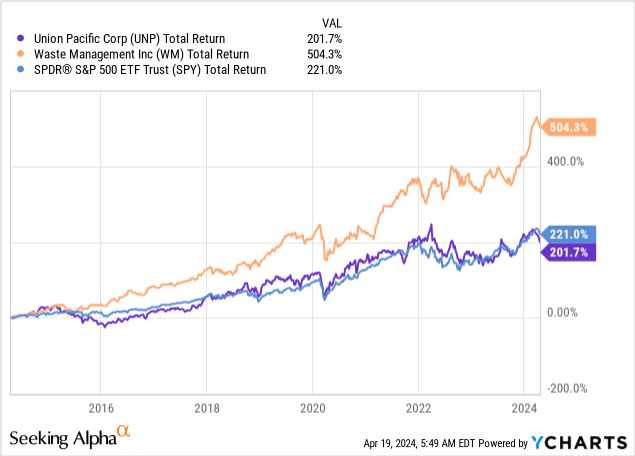

- I included two industrial stocks. Union Pacific and Waste Management. These two stocks give investors fantastic exposure to critical supply chains. Union Pacific is the largest public railroad, servicing all major economic centers in the western two-thirds of the United States, with connections to Mexico and Canada. It has a duopoly with Warren Buffett’s BNSF railroad. Meanwhile, Waste Management is highly anti-cyclical, as it is the nation’s largest waste management company. It benefits from our ever-increasing need to get rid of waste, recycle valuable waste, and turn certain items into renewable natural gas. It’s a stock on my watchlist I desperately want to own. I own Union Pacific. It was one of the first dividend stocks I added to my portfolio.

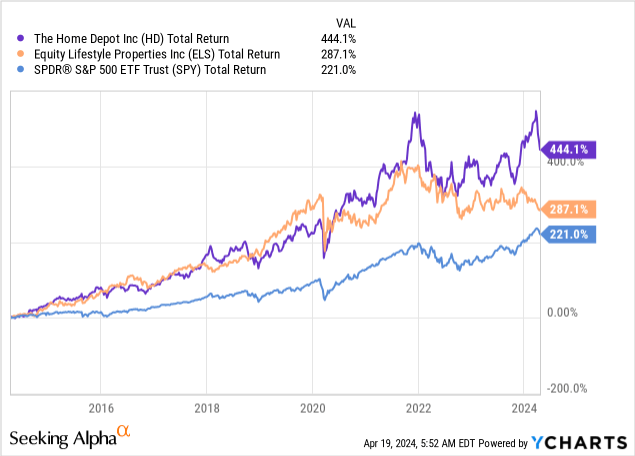

- I went with two housing-related stocks: Equity LifeStyle Properties and Home Depot. Equity LifeStyle is a REIT focused on manufactured housing communities benefitting from housing shortages, secular demand growth from retirees, inflation protection (rents are often tied to CPI), and anti-cyclical demand. While Home Depot is more cyclical, it benefits from its move into the Pro segment, a major footprint in the DIY sector, and its focus on dividend growth and buybacks. To me, HD is one of the best consumer stocks in the world. I believe these two stocks give investors fantastic long-term housing/consumer exposure with a terrific risk/reward profile.

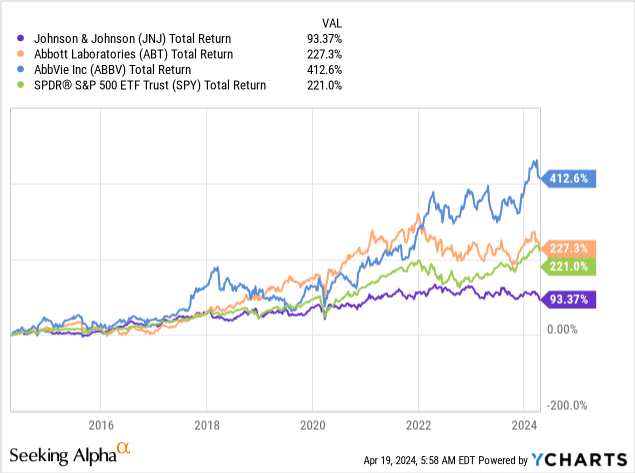

- I love healthcare, which is why I went with three plays in this area. I added Abbott Laboratories because of its fantastic mix of products, including therapeutics, cardiovascular health, diabetes, and more. The stock is a very consistent dividend growth company with a Dividend King tag after more than 50 consecutive annual dividend hikes. AbbVie is also a Dividend King, as it is a spin-off from Abbott that has hiked its dividend every single year since the separation. This company is a biotech giant with large franchises in arthritis, leukemia, and other illnesses and disorders. I also added Johnson & Johnson. Although this stock has struggled in recent years, it is now streamlined after spinning off Kenvue (KVUE) and focused on high-growth markets in surgery, orthopedics, and others. It also has an unbeatable credit rating of AAA.

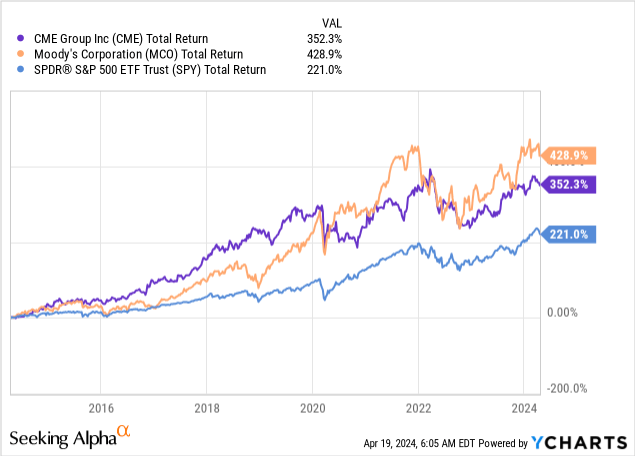

- Speaking of credit ratings, I also added two financial stocks. Neither of these companies is a bank. Both benefit from tremendous secular growth. CME Group owns major stock exchanges, like NYMEX and CBOT, which includes the famous e-mini S&P 500 Future. It makes money on every transaction and benefits from the ever-increasing need of corporations to hedge financial risks. On top of that, it usually benefits when volatility spikes during recessions, making it a great play for safety – although its stock tends to sell off with the market. Also, it usually pays a special dividend in January, bringing the total payout to roughly 100% of free cash flow. This is NOT visible in the portfolio tables above. The other stock is Moody’s, which is the second-largest rating agency in the world. It benefits from the advantages that come with a credit rating agency and its ability to diversify into other service areas, implementing new technology like artificial intelligence.

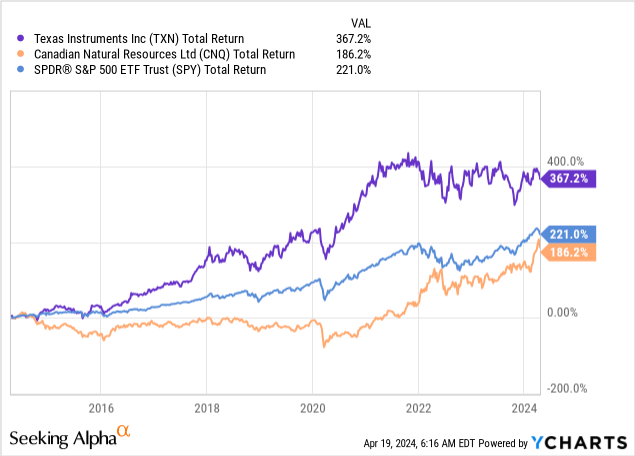

- Last but not least, I added technology and energy. For technology, I added Texas Instruments, a tech company with a highly cyclical customer base, which explains why it has been performing poorly lately, missing the upside of semiconductors with AI exposure.

- For energy, I added Canadian Natural Resources, which has low-cost production in Canada’s oil sands, very deep reserves, and the plan to distribute 100% of its free cash flow to shareholders through regular quarterly dividends, special dividends, and buybacks. As I am very bullish on oil, I made this one of my largest investments.

So, what about the performance?

A Highly Favorable Total Return Picture

There’s good and bad news.

The good news is that the data we’re about to see confirms the theoretical background we discussed in the first part of this article.

The bad news is that we can backtest only 11 years.

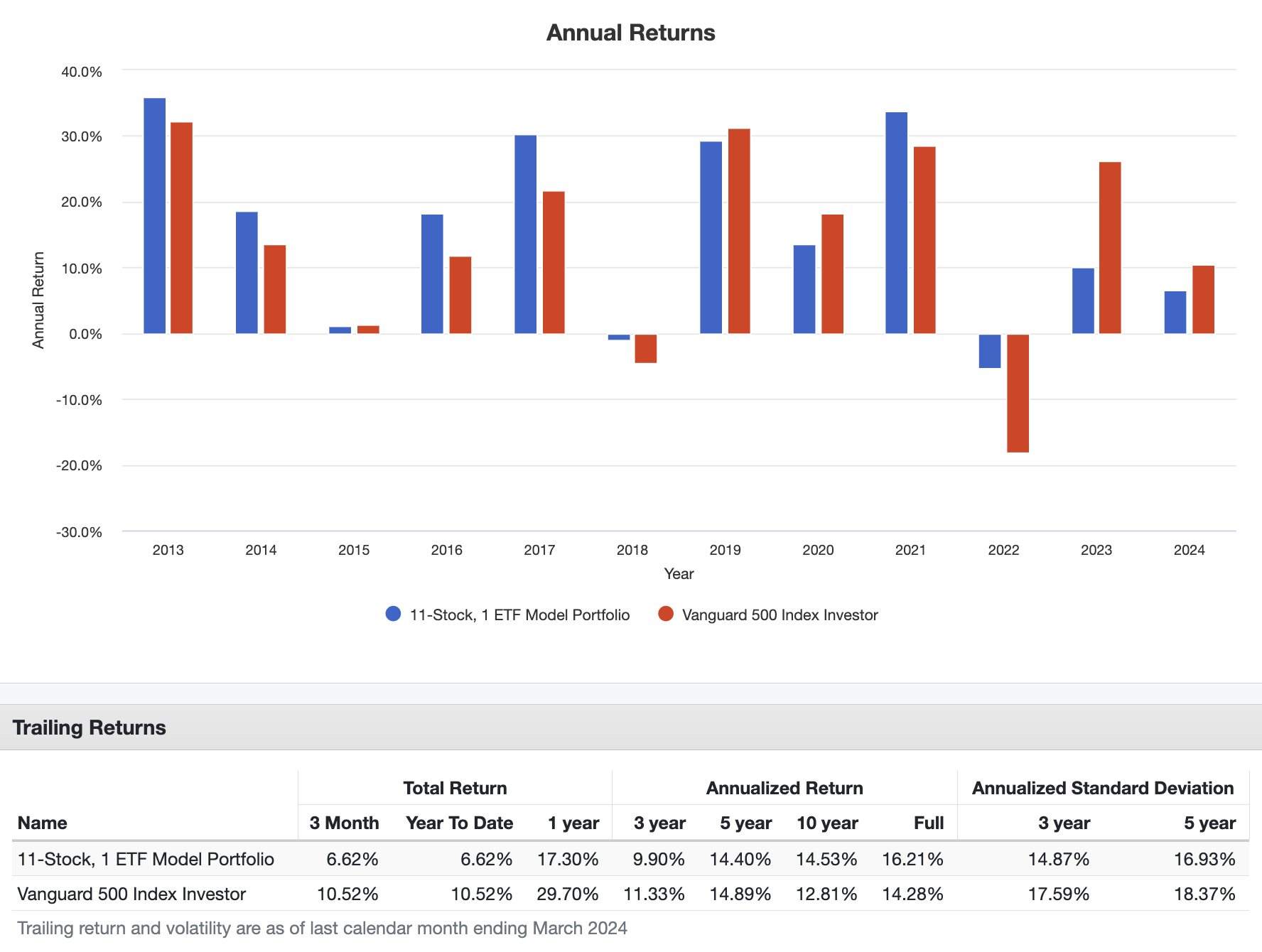

Going back to December 31, 2012, this model portfolio has returned 16.2% per year, turning a $10,000 investment into more than $54,000. During this period, the S&P 500 returned 14.3% per year.

Portfolio Visualizer

Even better, the standard deviation of the model portfolio was roughly 90 basis points lower that the S&P 500’s standard deviation.

The worst year of this portfolio saw a 5% drawdown, compared to -18% for the S&P 500.

As a result, it has a much higher Sharpe Ratio, indicating a very favorable risk-adjusted return.

Over the past five years, it has returned 14.4% per year, with a 140 basis points difference in the standard deviation.

Note that this model portfolio did not outperform the market in 2023 and the first three months of 2024, as this period was marked by a significant flow into high-growth technology companies. This also explains why value stocks have become so attractive compared to growth investments.

Portfolio Visualizer

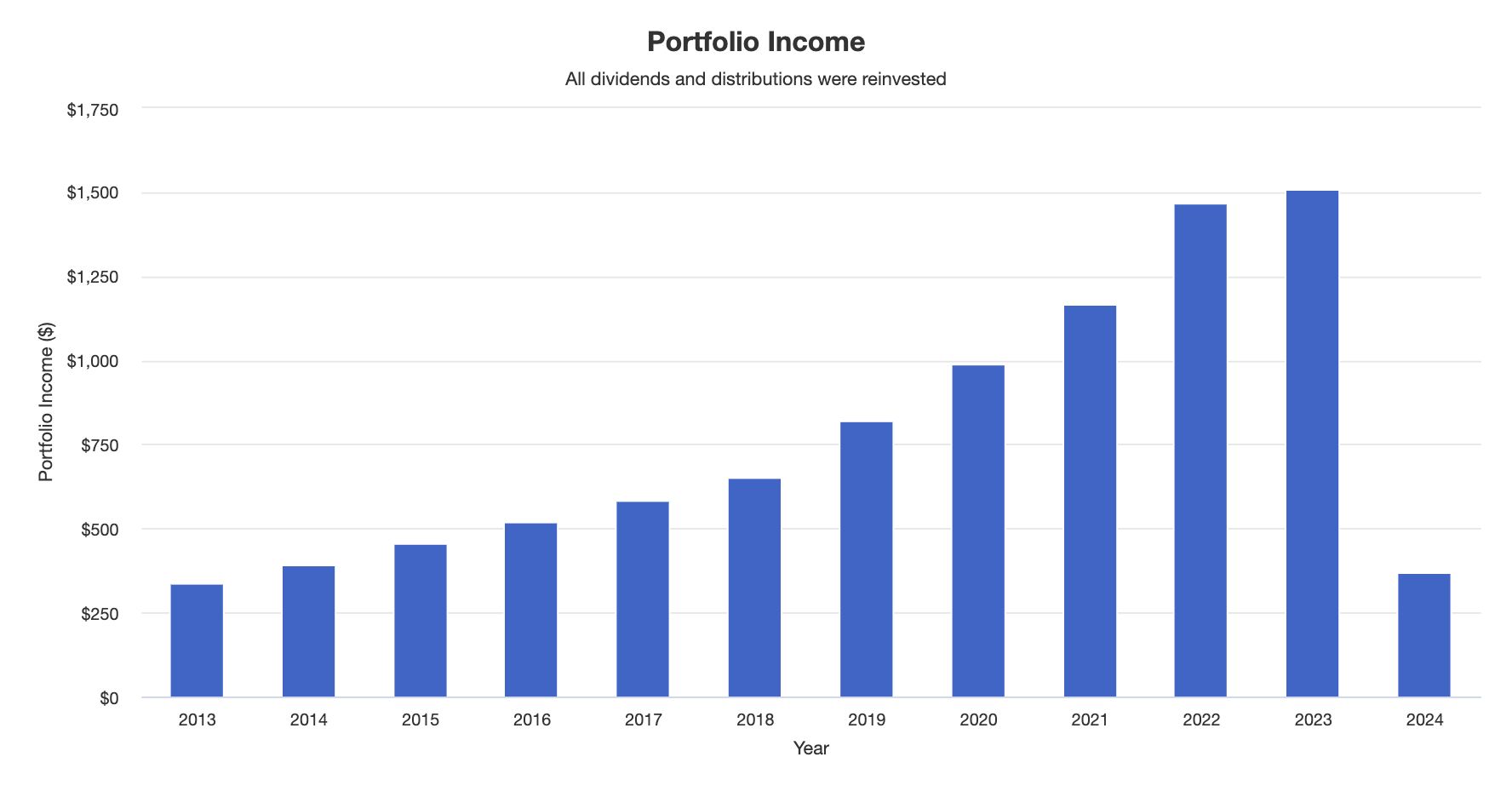

The portfolio has also seen higher dividend income for every single year since 2013.

For what it’s worth, a $10,000 investment in 2013 now pays more than $1,500 in annual income. That’s a >15% yield on cost (pre-tax).

Portfolio Visualizer

A $100.000 investment in this portfolio would pay $15,000 in annual dividends. That’s $1,250 in pre-tax monthly dividends.

While that won’t make anyone financially independent, it is a great start.

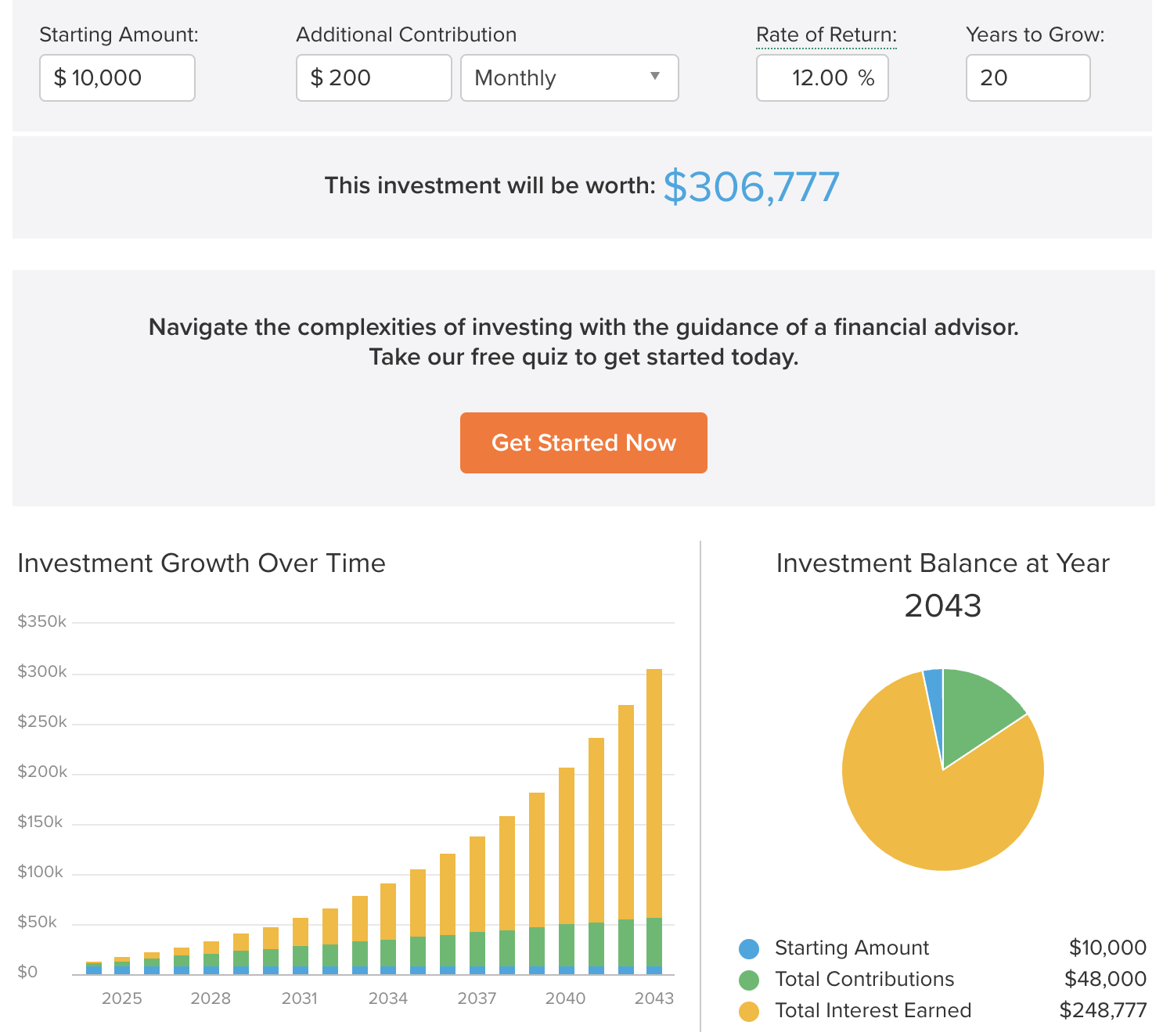

After all, even if we assume the portfolio return drops from 14-16% to 12%, a $10,000 initial investment could turn into $307,000 after 20 years, including monthly additions of $200. A $100,000 investment would turn into $3.1 million (assuming the monthly contribution of $200 is 10x higher as well).

Obviously, all of this is theoretical, but my point is that a well-diversified portfolio of wide-moat businesses with steady dividend growth can give investors a fantastic foundation to build long-term wealth with minimal monthly additions and a somewhat “low” starting budget.

SmartAsset

Hence, assuming that this portfolio can turn $10,000 into $300,000 is not at all far-fetched.

Moreover, if needed, investors can sell this portfolio close to retirement and switch to higher-yielding investments.

However, because this portfolio yields close to 3%, it does come with income, which will allow some investors to retire with minimal changes.

My personal view is to change just a few investments if I get to a situation where I could live off my dividend stocks, as I always want to benefit from the power of dividend growth – even when I’m old.

Takeaway

By focusing on consistent dividend growth, investors can find higher returns in lower-risk areas.

This approach defies the conventional belief that greater returns require greater risk.

The portfolio in this article emphasizes companies with wide-moat business models, strong financials, stable earnings, and a commitment to shareholder returns.

Moreover, by blending higher-yielding dividend stocks with those offering more growth potential, this strategy offers a balanced approach suitable for most investors.

As a result, despite market volatility in the past 11 years, the portfolio has shown resilience, delivering favorable total returns and a steady stream of dividend income.

I believe this approach lays a solid foundation for building wealth, even with minimal monthly additions and a modest initial investment.

{kind=link}