Alexandr Screaghin /iStock via Getty Images

Universal Corporation (NYSE:UVV) reported its latest quarterly result, highlighted by steady growth and profitability. The company, recognized as the world’s largest supplier of raw tobacco leaf, has benefited from strong pricing, helping to balance ongoing industry headwinds on the volume side.

The attraction here is that even as cigarette sales are down globally, the rise of smokeless tobacco products including vaporizers and oral nicotine pouches has worked to support demand and points to the company’s sustainable future.

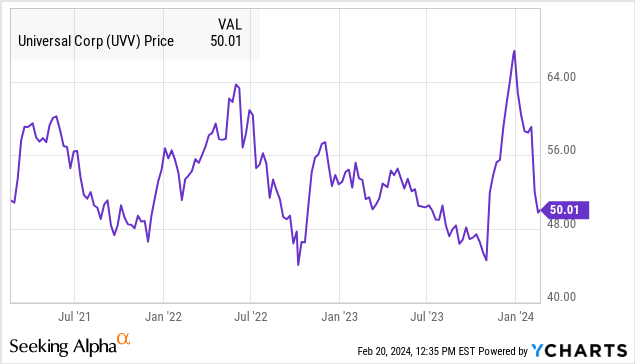

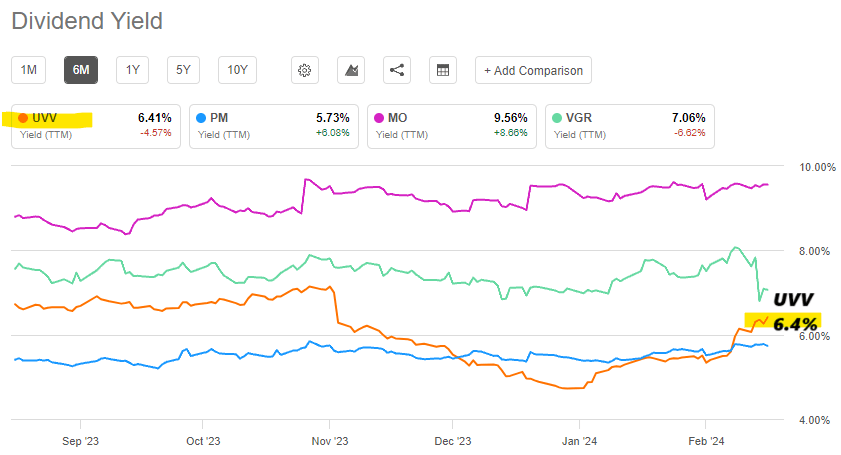

We last covered UVV back in 2022, citing the opportunity in the company’s smaller ingredients segment, diversifying beyond tobacco. While the stock has been volatile over the period, we reiterate a bullish view, with the recent selloff representing a new buying opportunity. UVV is a high-quality segment leader with a compelling 6.4% dividend yield, which we believe has good value at the current level.

UVV Earnings Metrics

UVV reported fiscal 2024 Q3 EPS of $2.12, up 27% year-over-year. Revenue of $821.5 million climbed by 3.3% y/y. We mentioned the higher average pricing for different types of tobacco leaf, considering historically low levels of supply and tight inventories globally. Management also explains that a favorable product mix has added to the top line momentum.

Within ingredients operations, revenue of $77.6 million increased by 10% y/y, rebounding from a weaker first half of the year. For context, ingredients contributed a modest 3% of total operating income this past quarter.

On the earnings side, the gross margin of 20.3% climbed from 18.3% in the period last year, which is in the context of a more difficult comparison period in 2022 that has improved from easing cost pressures. Over the first nine months of the fiscal year, EPS is up about 12%

source: company IR

While Universal is not providing official financial targets, comments during the earnings conference call projected optimism for the rest of the year and into fiscal 2025. The theme remains the tight tobacco supply globally, with a focus on generating operational efficiencies.

The company continues to move forward with growth efforts, including the expansion of an ingredients processing facility in Lancaster, Pennsylvania, expected to be online by the end of this calendar year.

In terms of the balance sheet, Universal ended the quarter with $74.1 million in cash against $617 million in long-term financial debt. Considering approximately $268 million in EBITDA over the trailing twelve months, a net leverage ratio of around 2x is stable in our opinion.

What’s Next For UVV?

While Universal doesn’t capture the same spotlight as cigarette makers like Philip Morris International Inc. (PM) or Altria Group, Inc. (MO), our understanding is that the company is equally important and possibly even a better investment within the industry.

The big advantage we see when looking at UVV is that the company is removed from the regulatory uncertainties PM and MO face as dealing directly with consumers while UVV is a business-to-business supplier.

A major trend from the cigarette players is attempting to deal with falling rates of combustible tobacco use worldwide. According to the World Health Organization, the prevalence of tobacco use among people over the age of 15 between men and women is around 22% in 2020 and has declined from as high as 26% 10 years ago. At the same time, the decline is seen leveling off through the rest of the decade towards 18%.

Within that amount, a major trend is the shifting consumption patterns between “combustible” products like cigarettes into next-generation form factors including not only “heated tobacco products” like electronic cigarettes and vaporizers, but also nicotine pouches that have benefited from accelerating growth in recent years.

source: WHO

As it relates to Universal, the company’s core product of tobacco leaves will continue to play a critical role in the supply chain as the base for the evolving demand drivers. This was a point management specifically touched on going back to the Q2 earnings conference call last November:

We continue seeing a strong demand for our portfolio of products, different varieties of tobacco. We stated that we see undersupply basically in every one of these categories, and we believe that it will continue into the next year.

So with regards as new generation products, as I stated also before, we basically participate in all these categories as well as supplying service and raw products for the heat-not-burn, for the vaping, shisha, smokeless, oral products, and that is why — how we see it that we continue seeing opportunities in all the segments where we operate.

In other words, regardless of how the industry shakes out between winners and losers, Universal stands to benefit regardless of the direction tobacco consumption goes.

By this measure, we see good value in its 6.4% dividend yield relative to PM at 5.7% and also lower risk compared to MO, which has faced some financial weakness in recent periods.

Seeking Alpha

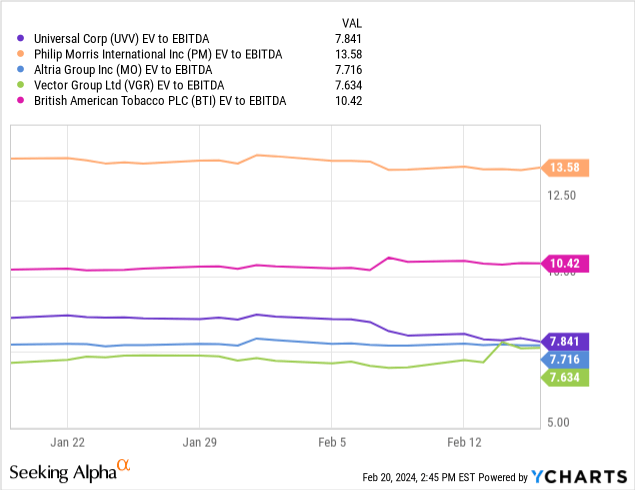

Our assessment of value is also consistent with UVV trading at an 8x EV to EBITDA multiple, notably at a discount to PM trading closer to 14x. To be clear, each of these tobacco stocks has varying strengths and weaknesses, but our take is that UVV offers a good balance of exposure to high-level trends with lower headline risk on the regulatory side.

Final Thoughts

We rate UVV as a buy with a price target for the year ahead at $60.00 implying an expansion of the current valuation premium towards a 9x EV to EBITDA multiple.

As we see it playing out, solid results over the next few quarters should help support more positive sentiment toward the stock, with an upside catalyst being the ability of the company to elevate margins. The possibility of falling interest rates through the rest of the year should also work as a tailwind for the stock. The upside here would be stronger than expected trends on the ingredients side of the business as an incremental growth driver.

In terms of risks, even with the defensive or counter-cyclical profile of the tobacco industry, Universal would not be immune to a global macro slowdown. A sharper decline in tobacco demand trends or cigarette sales would also force a reassessment of the long-term earnings outlook.

{kind=link}