hirun

Investment Thesis:

My Buy thesis on Workiva (NYSE:WK) is predicated on two key value drivers for the investment thesis. First, management is focused on improving its go-to-market strategy and creating value by incentivising upselling and cross-selling products. Second, regulatory regime changes in Europe, the US, and APAC are creating a significant tailwind for growth in the next five years. Workiva’s International market position will strengthen due to these regulatory shifts. I believe management has put the right incentives and organisational strategy in place to execute this growth opportunity.

Overview of the Business Model:

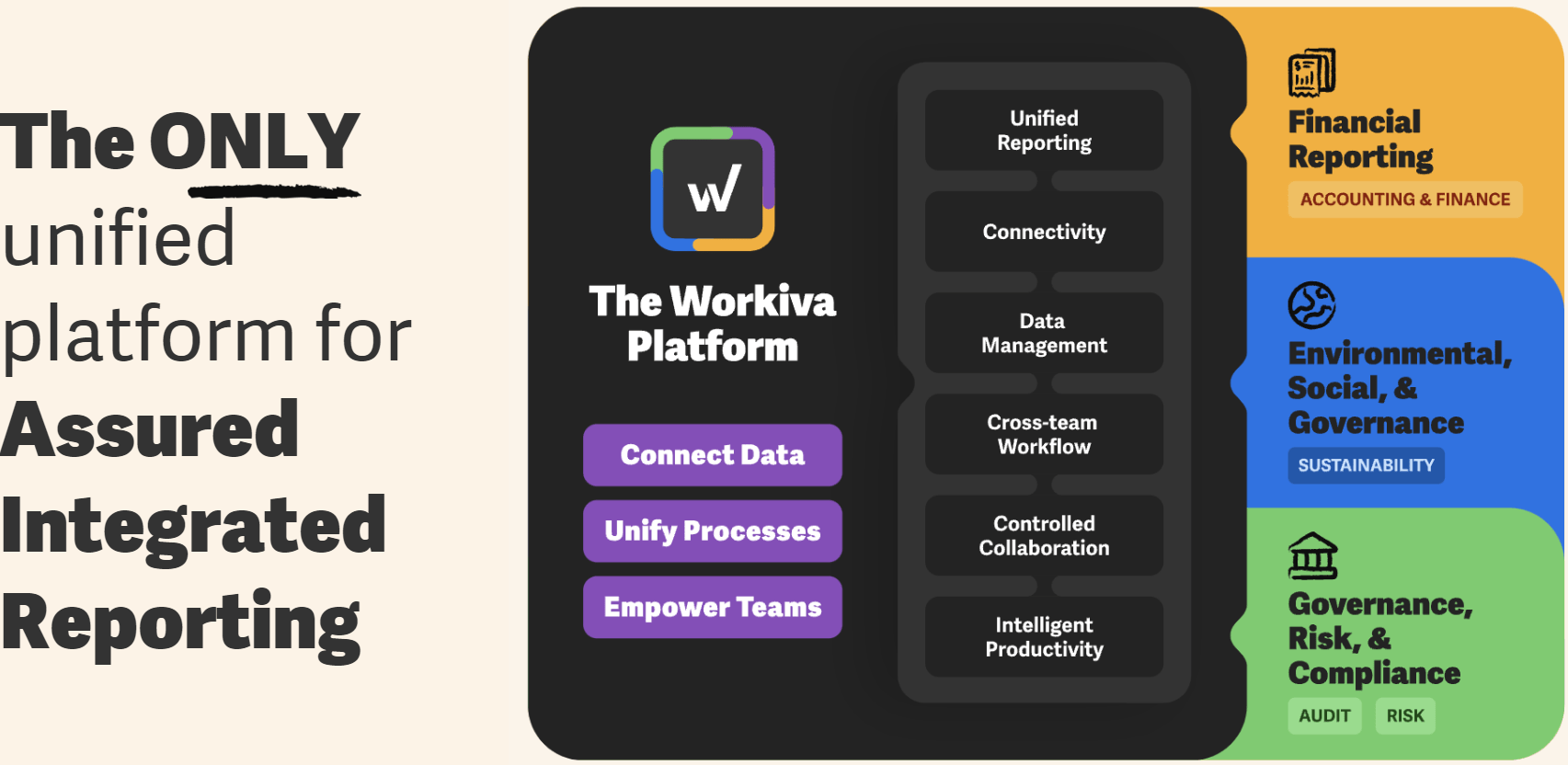

Workiva was founded in 2008 under WebFilings and later renamed Workiva in 2014. Its first product was a solution to aid workers with completing SEC filings. Workiva’s software allows multiple workers to collaborate in real-time, provides functionality to link text and numbers in the document to a single live source, and helps with XBRL tagging, the global standard for exchanging financial and business data.

If you wonder what this XBRL term means, it stands for eXtensible Business Reporting Language. XBRL is the underlying code associated with filing financial statements. It was created to provide an approach for efficiently sorting and comparing financial data.

Workiva’s business (Author)

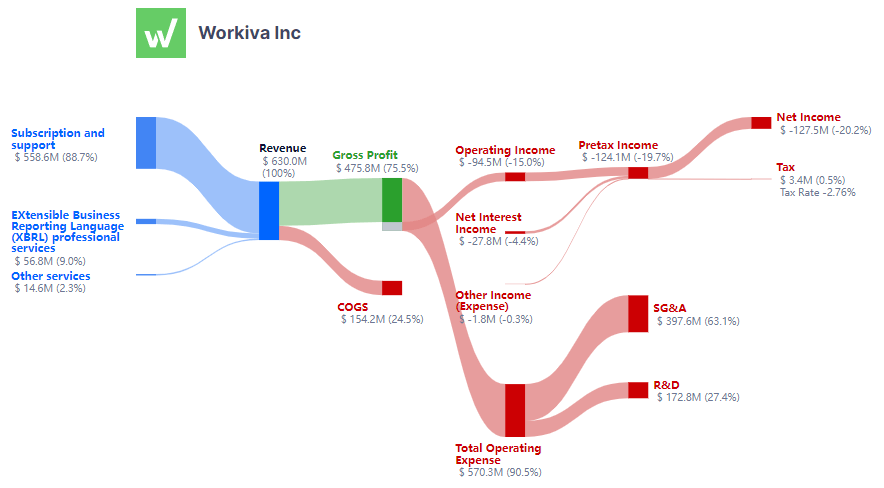

Roughly 90% of Workiva’s revenue comes from subscriptions to its platform, and investors should focus on this. The subscriptions are centred around three product offerings: financial (SEC Reporting), Sustainability (ESG Reporting), and GRC (Governance, Risk, and Compliance Reporting).

Company Investor Relations

Key Value Drivers are components of an investment case that generate the bulk of financial progress and drive future returns. In the case of Workiva, two key value drivers are driving performance and are worth pointing out.

First Key Value Driver

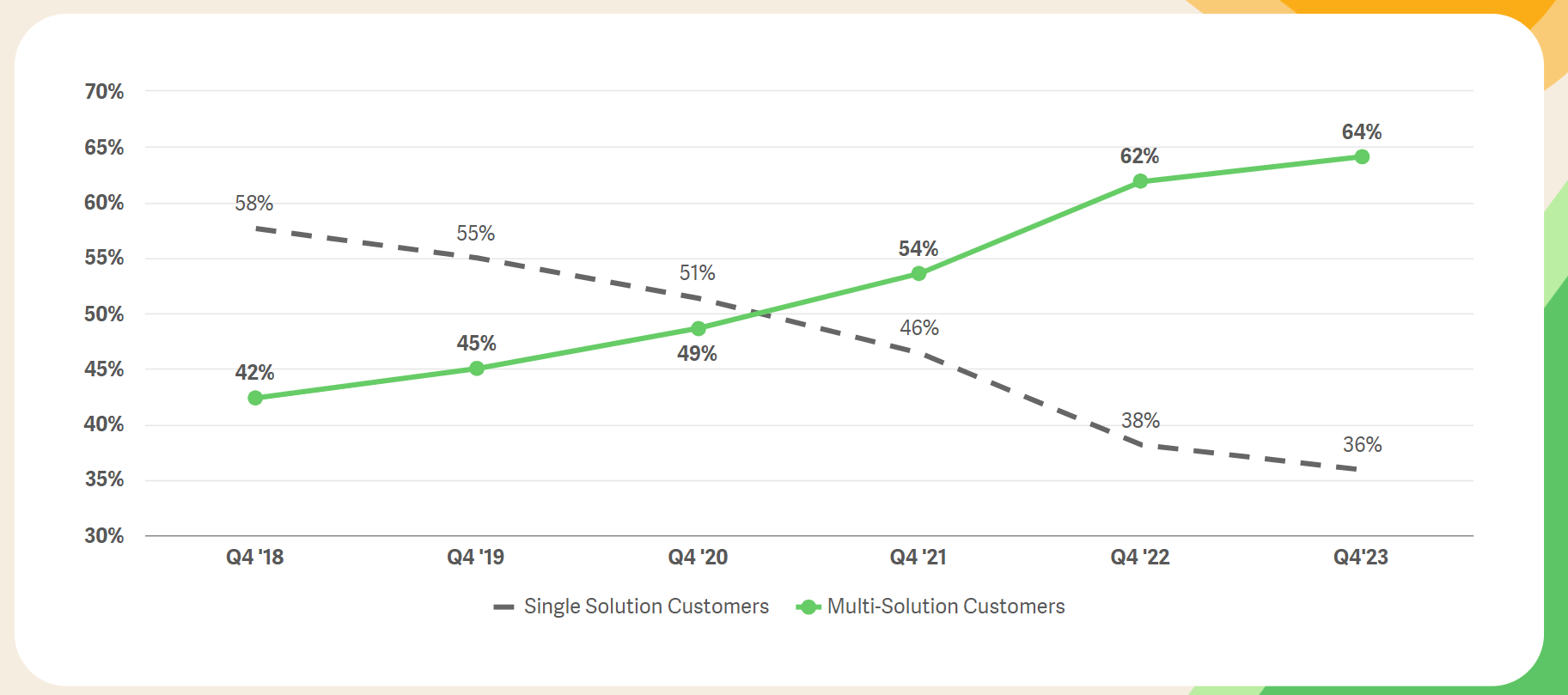

The first key driver of this investment is Workiva’s ability to continue cross-selling and upselling products to its existing customers. Customers subscribing to multiple product solutions significantly bump ACV and contribute to net revenue retention. Workiva’s sales teams successfully promote their offerings to existing customers, and take-up rates for multiple solutions are accelerating. In Q4 2018, the percentage of customers who subscribed to multiple solutions was 42%, which steadily grew to 64% in Q4 2023. Workiva’s solutions satisfy the needs of organisations and help bridge the gap between the organisations’ current practices and new reporting standards (ESG, Disclosure and Risk). This is a crucial driver to the investment case, and Julie, the CEO’s recent presentation at the 2024 Morgan Stanley Conference, confirms their focus on cross-selling.

Workiva 10Q Filing

The incentivization of sales employees to push for multi-product adoption will continue to drive up cross-selling, and I believe 75% of customers will subscribe to multiple-product solutions by 2025. This will also drive net revenue retention rates higher than 110% in Q4 2023. Julie Iskow explicitly mentioned that “large contract accounts continue to grow, we put heavy emphasis on multi-solution and account expansion” at the MS TMT conference. Considering that multi-solution penetration grew 19% in the past 4 years, it is reasonable to model that it will grow by 11% to 75% over the next 3 years. Especially during a period when management is focused on cross-selling incentivisation. I currently approximate that Workiva’s ESG solution accounts for ~8% of revenue, and the recent SEC ruling (explained below) will contribute to multi-solution adoption.

Second Key Value Driver

The second key value driver is the success of its international market expansion. A slew of government regulations push for greater transparency on ESG reporting standards. These are significant drivers of demand for Workiva’s Reporting software. The SEC just finalized the SEC disclosure rules with an 886-page report. The main relevant takeaway from this report is that the SEC will require companies to disclose Scope 1 emissions and Scope 2 emissions if they are deemed material. XBRL tagging will be required for filers in 2026. Despite how long it takes for the full regulation to kick in, roughly in 2030, ESG XBRL tagging will be required by 2026, and Workiva’s solutions will benefit significantly from this.

Workiva has invested significantly in Sales and Marketing to drive growth in Europe and its international markets. According to their TAM assessments, their TAM in North America is ~$ $11.6 bn; in EMEA, it’s $7.5bn, and in APAC, it’s $5.9bn. Considering the size of this opportunity, Workiva is well placed to continue gaining a share in the European markets and growing its wallet share with each customer every year.

Investor Presentation (Investor Presentation)

Growth in its International business has been significant, but it hasn’t been firing on all four cylinders. Based on the CEO’s recent comments on the Earnings call and the MS TMT Conference Webcast, the International salesforce has been correctly incentivized to drive growth. The right go-to-market partnerships have also been formed to drive this motion. As a reminder, international business has grown from $27M in 2020 to $93mn in 2023. I think 20% CAGR is achievable for that part of the business over the coming three years.

Model Evolution and Valuation

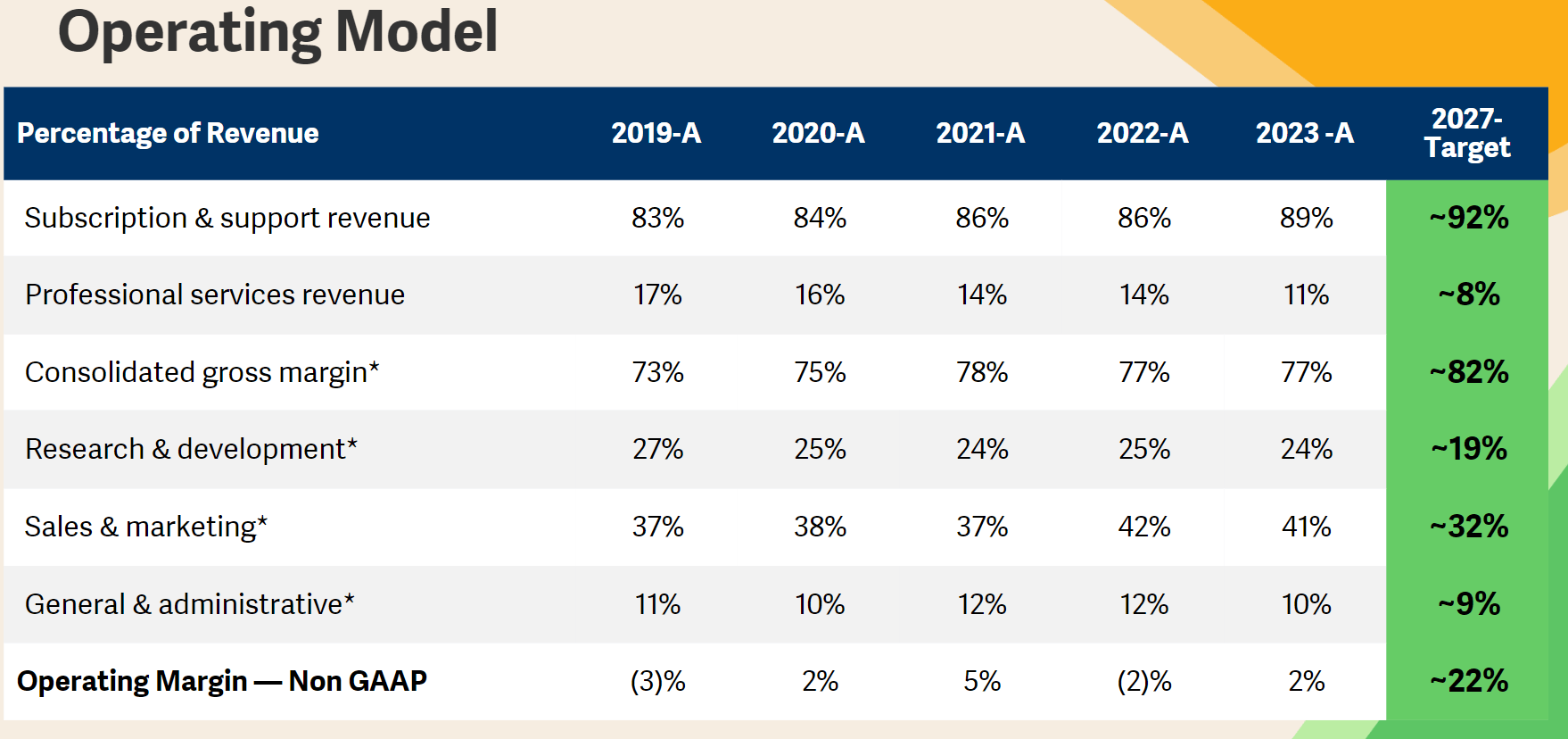

Workiva’s operating model has continued to strengthen over the past four years. Workiva’s financial targets for 2027 are ambitious but paint a realistic picture of what is achievable, especially compared to other SaaS businesses.

Investor Presentation

Consensus estimates are aligned with management’s 17% guidance for the following two years, but I believe that as these regulatory tailwinds kick in and the international sales motion fires on all four cylinders, growth will surpass estimates. My modelling expectations are based on management’s stated ambitions and the key value drivers exemplified earlier.

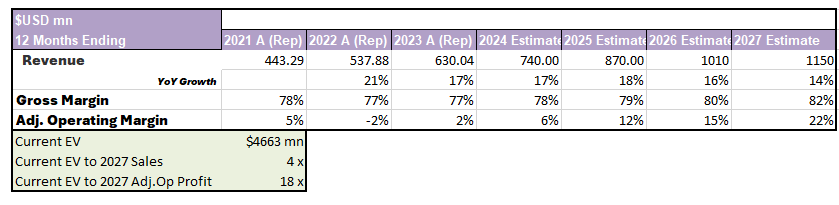

Author’s Model using Refinitiv Data

Risk Factors

While management is strongly aligned with shareholders, with insider share ownership being around 5%, there is a risk that strategic execution does not shine through. Sceptics will question Workiva’s lack of substantial growth in the European markets over the past 3 years. However, I would argue that Workiva’s management has addressed the gaps in its European salesforce and now has the proper sales structure, strategy and go-to-market plan to execute effectively.

Another risk to the case may be the lack of regulatory momentum driving demand for Workiva’s ESG and Risk reporting software. While that may be possible, regulatory announcements over the past two years have significantly favoured further and deeper disclosure of environmental emissions and practices. It is at the top of the minds of leading politicians worldwide.

Conclusion

I believe Workiva’s strategic focus on go-to-market is well-timed with the regulatory growth trends that will stimulate further interest in its subscription offerings. Management’s focus on profitable growth will also improve unit economics and overall profitability. In light of my fundamental thesis, composed of the two key value drivers and the reasonable valuation of 4x sales and 18x EV/EBIT based on my 2027 projections, I believe Workiva offers an attractive risk/reward profile for the next 3 years. It will be essential to keep a close eye on the quality of management’s execution, which will validate the investment case.

{kind=link}