Conservative hybrid funds are aimed at investors seeking relatively-lower volatility than equity-heavy funds, while retaining limited equity exposure for potential upside.

In line with regulatory mandate, these schemes invest predominantly in debt, with a smaller equity allocation. They may be less volatile than pure equity funds while potentially offering returns higher than traditional fixed-income avenues.

The category may appeal to cautious investors and savers with medium-term goals of three-five years who are unwilling to take sharp equity-market swings.

Within the category, SBI Conservative Hybrid Fund follows a relatively higher-yielding debt strategy than many of its peers.

Unlike most peers that largely stick to high-quality sovereign and AAA-rated papers, the fund tactically combines active duration calls with a meaningful allocation to AA-rated debt instruments. This can increase the interest income earned by the portfolio (accrual income), but it also exposes investors to greater credit risk if an issuer’s ability to repay weakens.

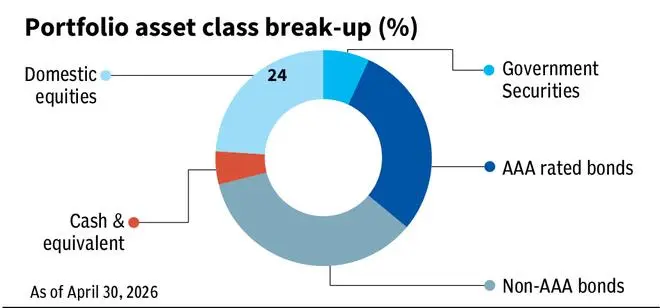

The fund has generally maintained close to 25 per cent in equity and 75 per cent in debt across market cycles.

Active duration

On the debt side, the fund seeks returns through a mix of interest-rate calls and higher interest income from selected corporate bonds. The fund generally keeps its Macaulay duration, a measure of the average time taken to receive bond cash flows, within a two-five-year range. It is currently near the shorter end, at around 2.4 years.

The fund has reduced duration over the past year because yields in the segments it had favoured have already eased, reducing the potential benefit from holding longer-duration bonds. It is, therefore, holding shorter-duration bonds and relying more on regular interest income from its debt investments.

High-yield opportunity

A key source of additional yield is the fund’s exposure to corporate bonds rated below AAA. These currently make up about 35 per cent of the portfolio and may rise to 45 per cent when the manager sees opportunities. The strategy seeks to earn the extra yield offered by corporate bonds over government securities, in return for taking higher issuer risk.

Of the total portfolio, about 10 per cent is in AA+ rated bonds, 17 per cent in AA-rated bonds and 8 per cent in AA- and lower-rated papers. A few names in the AA and below segments include GMR Airports, Avanse Financial Services, Infopark Properties, JTPM Metal Traders and Aditya Birla Renewables. According to the latest portfolio, AAA-rated bonds accounted for 24 per cent of assets, while government securities accounted for 7 per cent.

Within government securities, the fund’s duration is around four years, compared with roughly seven years for its benchmark. This reflects the manager’s view that longer-maturity government bonds offer limited scope for meaningful outperformance.

The other funds in the category that hold material non-AAA exposure include Nippon India Conservative Hybrid (54 per cent as of April 2026) and ICICI Pru Regular Savings (42 per cent).

Flexi-cap equity strategy

The equity portfolio is measured against the BSE 500. It typically holds around 40 stocks and can invest across large-, mid- and small-cap companies. The fund’s equity strategy aims to identify stocks with strong earnings potential, robust financials, high governance standards and sound ESG profiles.

The fund’s large-cap exposure can range between 30 per cent and 100 per cent of the equity portion, mid-cap exposure between 0 and 70 per cent, and small-cap exposure between 0 and 50 per cent. On an average, over the past five years, the fund has allocated around 10 per cent of its total assets to large-caps, 6 per cent to mid-caps and 8 per cent to small-caps.

Currently, the equity portfolio has a strong small-cap tilt, with exposure close to the fund’s stated upper limit of 50 per cent of its equity portion.

According to the manager, recent corrections have created stock-specific opportunities in small-caps after sharp declines in several companies. Large-cap exposure remains near the lower end of the fund’s mandated range at around 32 per cent of the equity portion, while mid-caps account for the remaining portion. As of April 2026, the large-, mid-, and small-cap allocations stood at 8 per cent, 4 per cent, and 12 per cent of the total assets, respectively.

The equity allocation is currently fully invested, with the fund maintaining close to the maximum permissible 25 per cent equity exposure and negligible cash holdings on the equity side.

Performance

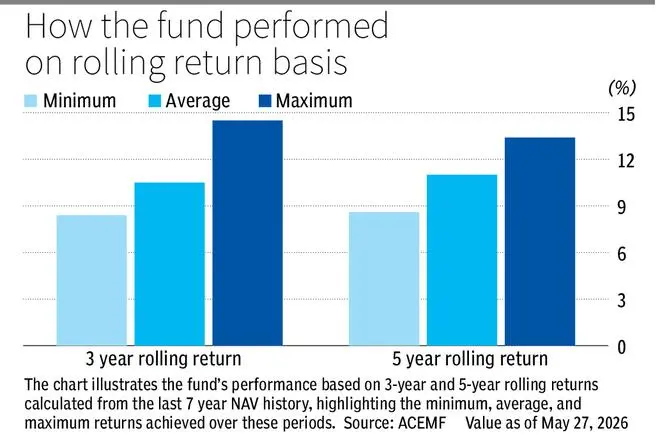

Across five-year rolling periods observed during the past seven years, the fund delivered an average annualised return of 11 per cent, against 9 per cent for the category.

Across these five-year rolling periods, annualised returns ranged from 8.6 per cent to 13.4 per cent.

Across three-year rolling periods, the fund delivered an average annualised return of 10.5 per cent, against the category average of 8.8 per cent.

As of April 2026, the debt portfolio’s yield to maturity, an indicative yield assuming securities are held to maturity and repayments occur as scheduled, was 8 per cent, against the category average of 7.4 per cent.

The expense ratio for the regular plan is 1.5 per cent, slightly below the category average of 1.6 per cent. However, its direct plan expense ratio is 1.07 per cent, above the category average of 0.84 per cent.

Given its sizeable exposure to lower-rated debt and its small-cap tilt within equities, the fund may suit investors willing to accept moderate credit and equity risk, with an investment horizon of at least five years.

Published on May 30, 2026