Passive investing is gathering momentum in India, with investors increasingly weighing index strategies to identify the most efficient route to long-term wealth creation. The Nifty 500, which covers about 92 per cent of listed market capitalisation on the NSE, serves as a broad proxy for the equity market. For many, a single index fund or exchange traded fund (ETF) tracking the Nifty 500 offers a simple, low-maintenance way to gain diversified exposure.

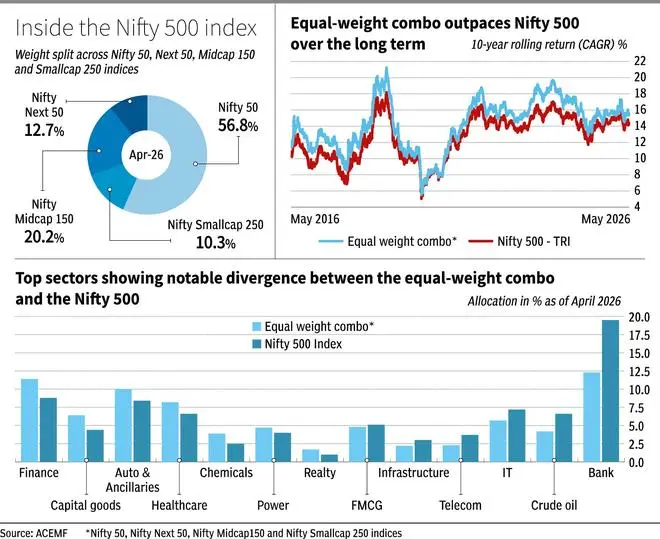

Yet, a bl.portfolio analysis shows that a structured mix of the Nifty 50, Nifty Next 50, Nifty Midcap 150 and Nifty Smallcap 250 can deliver superior long-term outcomes compared to the Nifty 500 alone. Based on 10-year rolling return data over the last 20 years, the Nifty 500 TRI generated an average CAGR of 12.7 per cent. An equal-weight allocation across the four indices, however, delivered about 14.3 per cent. This indicates an outperformance of 1.60 percentage points that can meaningfully enhance long-term compounding.

For investors starting early, a simple equal allocation across these indices offers exposure across the full market-cap spectrum of large-, mid- and small-caps.

Large-cap bias

The limitation of the Nifty 500 lies in its construction. As of April 2026, nearly 57 per cent of the index weight is concentrated in the Nifty 50, with the Nifty Next 50 accounting for another 13 per cent. Mid-caps and small-caps together account for just 30 per cent, at 20 per cent and 10 per cent respectively. In effect, close to 70 per cent of the index is tilted towards the top 100 companies — large-caps.

While this bias lends stability, it also skews the portfolio towards mature businesses where earnings growth may taper over time. In an emerging market like India, mid-sized and emerging companies often contribute alpha, capturing incremental growth beyond large, mature firms.

This skew towards large-caps of Nifty 500 is inherent to the free-float market-cap methodology. Because the Nifty 500 weights stocks by free-float market capitalisation, larger companies automatically get a bigger share, creating a built-in large-cap tilt. But for investors seeking true market-wide participation, such concentration can act as a structural drag.

A multi-index allocation helps address this imbalance by distributing exposure more evenly across market segments.

Why a combination works

The advantage of this Nifty 50-Next 50-Midcap-Smallcap mix shows up not just in returns, but in sector spread and risk management.

Broader sector play: A comparison of sector weights reveals meaningful differences. As of April 2026, banking accounts for 19.5 per cent of the Nifty 500, versus 12.3 per cent in the equal-weight combination, reflecting the index’s heavy dependence on large banks. The combination, however, allocates more to broader financials at 11.4 per cent against 8.8 per cent. This captures NBFCs, microfinance and fintech players that are better represented in mid- and small-cap segments. Similarly, the combination carries higher exposure to capital goods at 6.4 per cent against 4.4 per cent, healthcare at 8.2 per cent against 6.6 per cent, automobiles and ancillaries at 10 per cent against 8.4 per cent, and power at 4.7 per cent against 4 per cent. These sectors are closely aligned with India’s domestic growth narrative involving manufacturing, infrastructure and consumption. One can argue that Nifty 500 remains tilted towards more established, old-economy and export-oriented businesses. Additionally, sectors such as business services, education & training, media & entertainment and plastic products barely exist in the Nifty 500’s effective weight. The combination strategy brings these sectors into the portfolio mix.

Better risk management: Unlike the Nifty 500, where large-caps dominate by default, the combination approach allows investors to consciously set their exposure. An equal 25 per cent allocation balances stability with growth by anchoring the portfolio in large-caps, while ensuring meaningful participation in mid- and small-caps. More aggressive investors can increase their exposure to mid- and small-cap indices during favourable cycles, while conservative investors may tilt toward the Nifty 50 and Next 50. Also, unlike market-cap weighted indices that automatically increase exposure after rallies, a combination strategy creates a disciplined rebalancing framework. Indian equities exhibit clear cyclical leadership. Large-caps tend to outperform during global risk-off phases, mid-caps during steady domestic growth, and small-caps in liquidity-driven rallies. The bl.portfolio long-term asset allocation grid, too, reflects this trend. A multi-index strategy automatically captures this rotation, improving returns across cycles. No single segment leads indefinitely; the advantage lies in systematic participation across them.

Takeaways

Around 10 passive funds currently track the Nifty 500 and BSE 500, managing over ₹5,500 crore. While the Nifty 500 remains a convenient and broadly diversified benchmark, its inherent large-cap bias may constrain its effectiveness for long-term, market-wide participation.

A combination approach spanning the Nifty 50, Nifty Next 50, Nifty Midcap 150 and Nifty Smallcap 250 offers a more nuanced alternative. It reduces concentration risk, enhances sectoral breadth and gives investors greater control over allocation and rebalancing.

Also, comparing the yearly returns over the last 20 years shows that the combination strategy outperformed the Nifty 500 in 12 out of 20 periods.

This multi-index approach helps long-term investors earn steadier returns through market ups and downs.

That said, a multi-index combination is more complex than a single index, requiring monitoring, rebalancing and awareness of overlapping exposures. Trading costs, liquidity constraints in smaller indices, short-term underperformance during large-cap rallies, sector concentration and limited historical coverage of extreme events mean disciplined rebalancing is essential.

Published on May 23, 2026