Pogonici

By Peter Bourbeau & Margaret Vitrano

Staying Disciplined in a Broadening Market

Market Overview

The positive momentum of 2023 extended into the first quarter as a likely economic soft landing and being past the peak of monetary tightening sent stocks broadly higher. The S&P 500 Index (SP500, SPX) advanced 10.56% for its best start since 2019, boosted by solid corporate earnings and continued enthusiasm for generative artificial intelligence (AI). While the market showed some signs of broadening, mega cap growth stocks maintained their leadership with the Russell Top 200 Growth Index (11.70%) being the best performing segment for the quarter.

The likelihood of slowing economic growth and a more palatable rate environment going forward enabled growth stocks to maintain a premium over value stocks, with the benchmark Russell 1000 Growth Index rising 11.41% and outperforming the Russell 1000 Value Index by 242 basis points. Communication services (+17.34%) and information technology (IT, +12.68%) continued to outperform the benchmark, but more encouraging was greater participation in the quarter among utilities (+24.11%), materials (+13.56%), health care (+11.68%) and financials (+11.28%) stocks.

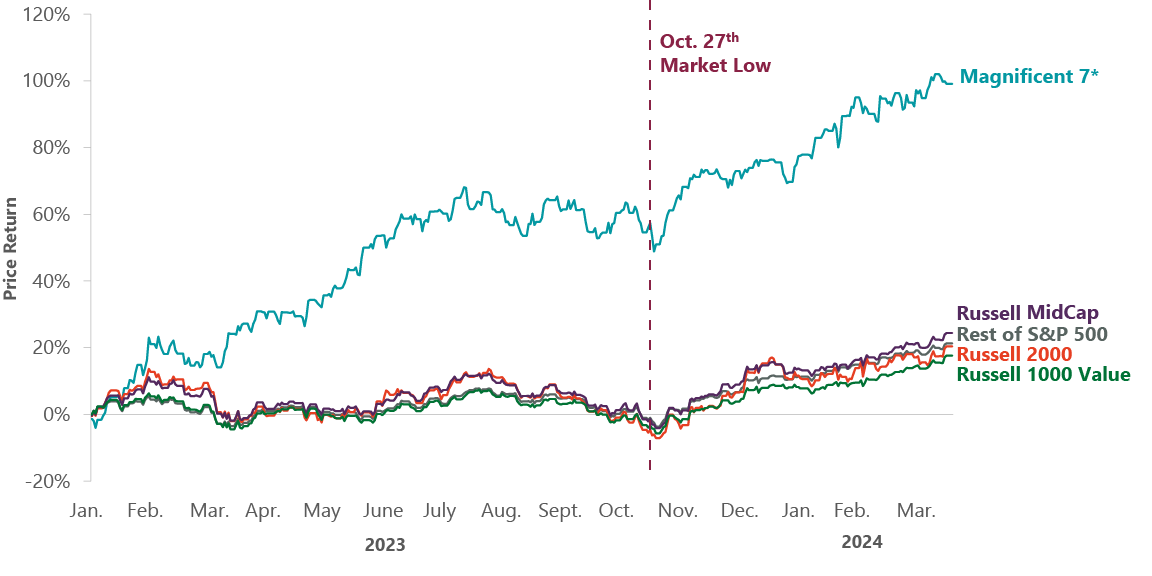

While market performance remained top heavy, divergence began to emerge among the Magnificent Seven (Alphabet (GOOGL), Amazon.com (AMZN), Apple (AAPL), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA) and Tesla (TSLA)), a basket of mega cap growth stocks that led the concentrated equity rally in 2023. The group constitutes 48% of the Russell 1000 Growth Index while the ClearBridge Large Cap Growth Strategy maintains exposure of 35.7%. This underweight enables us to own good businesses outside the group, like electrical components maker Eaton (ETN), and maintain a portfolio diversified across the select, stable and cyclical growth companies we target.

The Strategy outperformed its benchmark in the quarter due to a combination of active management of our mega cap exposure as well as strong stock selection across the rest of our growth universe. We tactically trimmed our overweight positions in all three to manage position sizing and fund opportunities in more attractively priced areas of the portfolio. We maintain exposure to six of the Magnificent Seven, with overweights in Nvidia, Meta and Amazon.com, which outperformed for the quarter. The Strategy is underweight Microsoft, Apple and Tesla, with the latter two suffering losses for the first three months of the year.

Exhibit 1: Actively Managing for Greater Market Participation

*Magnificent 7 data is cap weighted and refers to the following set of stocks: Microsoft (MSFT), Amazon (AMZN), Meta (META), Apple (AAPL), Google parent Alphabet (GOOGL), Nvidia (NVDA), and Tesla (TSLA). Data as of March 31, 2024. Sources: FactSet, Russell, S&P.

Complementing those stocks, the Strategy delivered solid results across our industrials holdings as well as cyclical names in the consumer staples and semiconductor areas. We are encouraged that outperformance has continued in step with increased participation across the market from the October lows. The likelihood of a soft landing, rather than a recession, has supported several early-cycle names, including mass market retailer Target and semiconductor equipment maker ASML (ASML).

Portfolio Positioning

Given our view that the overall market looks expensive, mostly due to mega cap valuations, the low likelihood that technology can continue to deliver well above market returns and an expected slowdown in economic growth, risk management has guided our recent positioning activity. We have been consistently trimming from the select bucket and redeploying into undervalued stable and cyclical names, while also being cognizant of position sizing to maintain the latitude to add to names when prices become attractive.

During the first quarter, we continued to trim IT stocks into strength to manage risk while also adding to high-conviction positions. For example, we trimmed our active weight in Palo Alto Networks after the information security software maker lowered its guidance in part due to a new emphasis on providing short-term discounts on product bundles to pursue its consolidation opportunity more aggressively. While this strategy should position the company more strongly in the future, it potentially increases volatility in operating results in the near-to-medium term. Part of the proceeds were redeployed into enterprise resource planning and finance software maker Workday, as we believe its products are well-positioned for consistent, robust subscription growth with potentially further upside as new investment initiatives scale.

We were also active in adding to stable bucket investments PayPal (PYPL) and UnitedHealth Group (UNH) where negative near-term sentiment led to more attractive risk/reward profiles. We added to electronic payments provider PayPal as we have growing confidence that new CEO Alex Chriss’s strategic focus areas can improve the company’s performance, particularly in the key branded business. We added to our UnitedHealth position after shares were pressured due to fears over competition among managed care providers and rising medical loss ratios in the industry. We believe the company will be able to “re-price” for higher medical costs, making this pressure transitory and we see competitive concerns as overblown.

Outlook

Stocks have been discounting a slowing economy with no recession but inclusive of rate cuts. We believe this has been the driver of momentum over the last year and that the market has downplayed fundamentals in the hopes of easier financial conditions in the future. If the economy dampens but avoids a recession, we should start to see early cyclicals work. Typically that would include industrials, semiconductors and consumer discretionary. The Philadelphia Semiconductor Index has already seen a nice move (up 64.9% in 2023), so we do not expect to see the same early cyclical recovery in that area. However, we would expect to see improvement in industrials and retailers. This was part of the motivation for our purchases of Target and Union Pacific last year, which should benefit as investors start looking toward the end of a slowdown.

If the economy is in a higher-for-longer rates scenario, we believe there may be more risk in the most expensive names in the market. While we do own some of those companies in the portfolio, we have been trimming them in favor of more reasonably priced growth businesses with good cash flow support for more restrictive conditions. In a higher-rate environment, companies with lower free cash flow yields are likely to see less multiple compression.

One of our larger macro concerns is the cadence of rate cuts the market is pricing in. The Fed doesn’t want to be wrong and have to reverse course with rate cuts if one (or both) of the pillars of its dual mandate of price stability and unemployment remain stubborn. Many components of input costs are now reversing higher after a prior decline, including crude oil, materials, industrial metals and agriculture. In addition, unemployment remains very low and labor costs elevated. The questions we now face are whether the neutral rate is higher than 2% and inflation structurally higher than in decades past, but we are certain it will take some time to settle this debate.

Preparing for a range of outcomes is our rationale for diversifying across the growth buckets. Beyond broader sector exposure, we want to own companies with different drivers that are able to perform in different kinds of markets. Areas we have been populating on our whiteboard include consumer discretionary and health care, as well as financials names with good free cash flow support.

Portfolio Highlights

The ClearBridge Large Cap Growth Strategy outperformed its benchmark in the first quarter. On an absolute basis, the Strategy posted gains across all 10 sectors in which it was invested (out of 11 sectors total). The primary contributors to performance were the IT, communication services and industrials sectors.

Relative to the benchmark, overall stock selection contributed to performance. In particular, positive stock selection in the communication services, IT, industrials and consumer discretionary sectors and an underweight to consumer discretionary drove results. Conversely, stock selection in the health care and financials sectors detracted from performance.

On an individual stock basis, the leading absolute contributors were positions in Nvidia, Meta Platforms, Amazon.com, Microsoft and Netflix. The primary detractors were Apple, Adobe, Tesla, Atlassian and Zoetis.

During the period the Strategy did not initiate any new positions or exit any existing holdings.

Peter Bourbeau, Managing Director, Portfolio Manager

Margaret Vitrano, Managing Director, Portfolio Manager

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication.

Performance source: Internal. Benchmark source: Standard & Poor’s.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

{kind=link}