Alistair Berg

By Derek Deutsch, CFA, & Mary Jane McQuillen

Staying Active in a Concentrated Market – Market Overview

U.S. equities continued their upward march in the first quarter as the momentum rally, begun following November’s inflation print, showed few signs of flagging. Behind the rally was strong GDP growth, the fading of recession fears, and fervor for the main investor themes in the last year: AI and GLP-1s.

Cyclical sectors in the benchmark Russell 3000 Index such as energy (13.13%), financials (11.71%) and industrials (11.11%) performed well on an improving economic outlook. Communication services (14.65%), which led the index, and information technology (IT; 11.81%) continued to benefit from AI enthusiasm. Rate-sensitive real estate (1.14%) and utilities (4.83%), meanwhile, trailed amid signs anticipated rate cuts from the Federal Reserve would be pushed out.

The Strategy delivered strong absolute performance driven by industrials and consumer discretionary holdings but trailed the benchmark largely due to relative IT positioning, as we do not own Nvidia (NVDA), whose 87% rise in the quarter accounted for ~21% of the index’s total return.

IT holdings such as Microsoft (MSFT), ASML (ASML) and Lam Research (LRCX), meanwhile, were leading contributors in the quarter – all benefiting from AI connections. Microsoft’s leadership position in generative AI is driving a positive inflection for Azure growth and adoption of its Copilot offering. Both ASML and Lam Research are semiconductor capital equipment companies seeing surging demand as AI build-outs need more and more chips. ASML, a leading supplier of extreme ultraviolet (EUV) lithography systems to the semiconductor industry, is benefiting from structurally rising EUV adoption not only in memory chips for AI (which handle data storage) but also in logic chips (which do the heavy computation), as well as the bottoming of logic semi capex. Lam focuses on semicap equipment used for making integrated circuits and saw memory-chip-related sales up 40% quarter over quarter, driven by memory supply growth for AI.

Our second-largest position, Apple (AAPL), meanwhile, declined as lower iPhone sales in the U.S. and China disappointed, an antitrust lawsuit and uncertainty concerning its next major revenue driver, in spatial computing, weighed on shares. However, we believe these issues are manageable and that the company is well-positioned going forward.

In industrials, Eaton (ETN), whose electrical equipment products enable the electrification of the power grid and, importantly, electrical vehicle charging infrastructure, posted strong results and issued positive guidance for FY24. Backlogs remained steady in the fourth quarter, while Eaton saw better order intake than management anticipated. The mega projects pipeline will continue to be a tailwind through next year, helped by a $32 billion jump in capex by hyperscale providers for AI. Likewise, Trane Technologies (TT) continued to perform well, delivering earnings ahead of expectations and benefiting from strong commercial HVAC booking growth.

Portfolio Positioning

We were active in seizing opportunities, as a concentrated market left pockets where excellent assets were undervalued. New additions were mostly IT companies such as Broadcom (AVGO), Marvell Technology (MRVL), Adobe (ADBE) and Dell (DELL). AI exposure is a common quality of these companies, although each exposure is unique.

Broadcom is a leading semiconductor company and increasingly a hybrid software company after a series of strategic acquisitions. While some of Broadcom’s end markets are in a down cycle (storage and broadband), AI is driving strong growth in the networking segment, which should more than offset the declines in the weaker segments. Broadcom is considered a best-in-class ESG company with solid management and governance, a leader in human capital management and a responsible manufacturer of products that promote greater resource efficiency.

Marvell is a fabless semiconductor company levered to the data center end market with exposure to enterprise networking, telecom, consumer and auto/industrial end markets. The key drivers to the thesis for Marvell are multiple idiosyncratic product cycles in the data center end market, including those tied to generative AI and traditional cloud infrastructure.

Adobe is a developer of cloud software for marketing and related creative applications. Adobe offers a variety of application software products used for digital media, document productivity and marketing optimization. We believe Adobe will deliver a combination of high growth and margin expansion driven by the monetization of AI products, pricing benefits in the enterprise market and margin leverage in digital media. We believe investor concerns about the timing of pricing benefits has created an attractive entry point. Adobe performs above peers on data privacy and security, human capital management and disclosure.

Dell is a technology hardware company making commercial and consumer personal computers, servers and storage solutions. Dell is enjoying high demand for its AI-optimized servers, while we believe Dell’s valuation underappreciates a nascent PC upcycle. To fund Dell, we sold Keysight Technologies (KEYS), which provides electronics test and measurement equipment and software to the communications and electronics industries, and for which an expected rebound in several end markets, including semiconductor projects, electronics production and industrial, will likely be delayed into 2025, leaving shares rangebound.

We also re-initiated a position in Enphase Energy (ENPH), a maker of microinverters for solar panels, which we had previously owned and had sold in 2023 because of lack of clarity on demand and industry destocking. The company now has stronger visibility on the bottom in destocking and improving demand. At the same time, Enphase has preserved its margins even as demand has decreased, which suggests pricing and profitability resilience. Given an end to destocking, Enphase’s consistent profitability and potential for long-term growth skew its risk/reward prospects in our favor again.

Resource efficiency and responsible consumption are central sustainability investment themes in the portfolio, in support of which in the first quarter we added LKQ (LKQ), the largest wholesale distributor of “like quality and kind” auto replacement parts. LKQ is the dominant player in an industry with stable demand that is uncorrelated to the macroeconomy: demand is driven by repairable car insurance claims, which are a function of vehicle miles traveled (VMT) and weather and have grown steadily for 25+ years. LKQ is the world’s largest recycler of cars at end-of-life, recovering greater than 90% of the materials from scrapped cars for reuse or recycling.

We exited other positions where our thesis in the stock became untenable due largely to stock-specific developments. These included Etsy (ETSY), in the consumer discretionary sector, which was unable to drive the gross merchandise sales growth we had hoped for as the post-COVID environment became more challenging and competitive than expected. In utilities, underperformance at some of Brookfield Renewable’s (BEPC) wind, solar and hydro assets have persisted longer than expected. Combined with the company’s elevated payout ratio, this reduced our confidence level in the business model, creating an unfavorable risk-reward prospect. Also in the utilities sector, we exited Ormat Technologies (ORA). Operational execution in the geothermal business has been less consistent than expected, and the profitability of the smaller storage business has been more volatile than we anticipated.

Outlook

The economic outlook is improving, helped by a strong labor market, although we may continue to see some heightened volatility as the pivot to lower Fed rates is a subject of intense market debate. But at a high level, it appears that the odds of a recession have diminished significantly. Our outlook for corporate earnings is likewise constructive, which should be a tailwind for performance for the remainder of the year.

Portfolio Highlights

The ClearBridge Sustainability Leaders Strategy underperformed its Russell 3000 Index benchmark during the first quarter. On an absolute basis, the Strategy had gains in nine of 10 sectors in which it was invested (out of 11 sectors total). The main contributors were the IT and industrials sectors, while the utilities sector was the sole detractor.

On a relative basis, overall stock selection and sector allocation detracted. Stock selection in the IT, health care and utilities sectors were the main detractors, while stock selection in the industrials, consumer discretionary, consumer staples, financials and materials sectors proved beneficial.

On an individual stock basis, Microsoft, Eaton, Williams-Sonoma, JPMorgan Chase and Hartford Financial Services were the largest contributors to absolute performance in the quarter. The main detractors from absolute returns were positions in Apple, Shoals Technologies (SHLS), Nike (NKE), SolarEdge Technologies (SEDG) and Gilead Sciences (GILD).

ESG Investment: AI Sustainability Opportunities and Risks

Artificial intelligence (AI) is transforming the investment landscape, and while its rapid development sparks some valid social and environmental caution, it also brings with it enormous potential for helping sustainability goals, with better data to improve energy efficiency, optimize renewable energy, make agriculture more sustainable and improve human health. ClearBridge is closely watching these opportunities even while we observe AI’s energy intensity and social dimensions as the phenomenon plays out in our portfolio companies across sectors.

On the regulatory front, the world’s first comprehensive AI law, the EU’s AI Act (AIA), will come into force later in 2024. The AIA classifies AI systems according to the risk they pose to users: there is unacceptable risk (such as emotion recognition in schools and workplaces), high risk (such as critical infrastructure and medical devices), limited risk (such as chatbots, which carry the risk of manipulation or deceit) and minimal risk (such as spam filters). Each level of risk is subject to different requirements, and there are heavy fines at the company level for noncompliance. President Biden also issued an executive order on safe, secure and trustworthy AI in October 2023, aimed at establishing standards for AI safety and security, protecting privacy, equity and civil rights, and supporting consumers and workers.

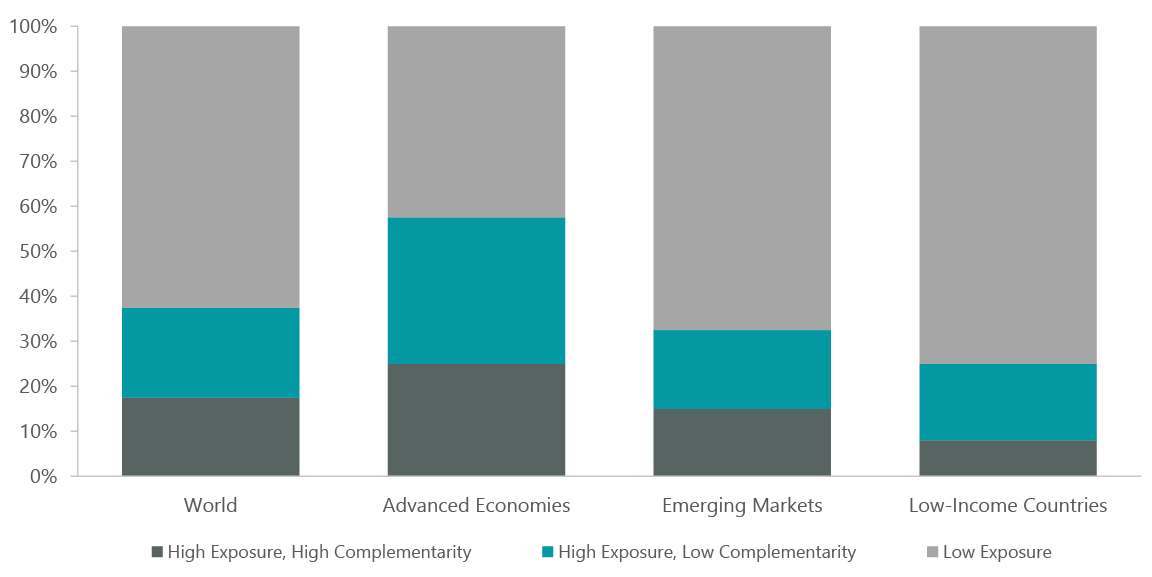

On the labor front, AI can boost productivity, but automation has always threatened labor disruption, potentially deepening global inequalities as AI growth may favor advanced economies with sufficient infrastructure and skilled workforces (Exhibit 1). Hiring algorithms may also rely on and perpetuate race and gender biases. Almost 40% of global employment is exposed to AI.1

Exhibit 1: Employment Shares by AI Exposure and Complementarity

Source: “AI Will Transform the Global Economy. Let’s Make Sure It Benefits Humanity,” Kristalina Georgieva, IMF Blog. Img.org. Jan. 14, 2024. For illustration purposes only. Complementarity implies AI leads to gains in productivity and higher income.

With looming questions of misinformation and digital safety, cybersecurity, and even human capital management, as hiring for AI ethics jobs is picking up,2 it is clear that as AI develops and hits multiple inflection points over the next few years, companies across ClearBridge portfolios will need to negotiate a variety of sustainability-related AI opportunities and risks.

AI and Power Demand Implications

AI is energy intensive, with data centers running the large language models requiring significant electricity and complicating the already complex power supply and demand picture of the energy transition. Overall estimates for data-center-driven U.S. power demand growth vary, but they generally forecast the electric load to roughly double by the end of this decade (from the current 3%-4% to ~8% by 2030).

On the surface, this kind of demand growth should cause generation shortages on the grid, especially in places where the data centers have been expanding rapidly such as Virginia and California.

Factors that could mitigate projected power shortages in the future would be:

- Continued improvement in technologies/efficiency of the data centers

- Expansion of the data center locations toward less congested grids

- An increase in utilization of the existent gas generation capacity and even delays in the scheduled coal plant retirements, which would increase the emissions’ intensity from AI

Another important mitigating factor over the next five years will be faster development of renewable power sources, as many data center hyperscalers have public commitments to carbon-free energy. The renewable projects’ shorter development/construction timeline and locational flexibility to satisfy the data center demand should push demand for renewables higher and improve the renewable projects’ returns. Renewable developers such as NextEra Energy (NEE) and AES (AES) should be beneficiaries of these trends. As highlighted at NextEra’s recent renewable-focused investor day, current forecasts call for renewable capacity to reach between 375 GW and 450 GW over the next seven years (2024-2030). This implies a 13% compound annual growth rate through the end of this decade and suggests a rapid acceleration in renewable development (235 GW of renewables were added over the last 30 years). According to the company, this anticipated power demand acceleration is expected to be driven by consumption growth from data centers (+108%), oil and gas industry (+56%) and chemicals (+14%) between 2025 and 2030.

Over the long term, data center power consumption growth and companies’ green targets should advance the development and utilization of more effective power storage and carbon capture and storage technologies as well as green baseload power solutions, such as green hydrogen and small modular nuclear reactors.

From the regulated utilities’ perspective, the ultimate impact of the data center demand growth will vary by region, but the overall implications for the sector should be positive. Data center additions to regional grids will not only drive incremental investments into the local transmission and distribution systems, but in some cases result in incremental generation needs. In the near-term, utilities located in the territories with planned data center expansions, such as Dominion Energy (D), Southern Company (SO), Sempra (SRE) and CenterPoint Energy (CNP), should benefit from higher required investments into the grid to accommodate additional demand.

AI Impact on Labor Conditions

Prior waves of technology dating back to the 19th century have changed the fabric of the global workforce. AI is similar but potentially more impactful in that it might affect white collar jobs just as much as it does blue collar labor. The power of generative AI (Gen AI) over prior AI advances is its ability to generate creative output. However, most companies are using Gen AI to augment their employees’ capabilities, rather than seeking to replace them. In ClearBridge engagements with technology companies using newly released code generation tools, we find they generally use them to speed up the first draft of a software engineer’s code output. This frees up the engineer to focus on larger problems such as user experience and system design. The risk of AI causing mass unemployment is therefore overstated, while the need to upskill and reskill today’s workforce is likely understated. By 2030, management consulting firm McKinsey estimates that as many as 375 million workers, or roughly 14% of the global workforce might need to switch occupational categories and acquire new skills.3 Just as prior waves of innovation did, the AI wave promises to create demand for new skills around model training, prompt engineering and data science.

While AI can often outperform human counterparts on a growing range of tasks, it lacks human intuition, context awareness and ethical judgment. Recognizing these limitations will help companies use AI more effectively and responsibly. When deploying AI to generate content, the primary ethical considerations are around protection of intellectual property rights and avoidance of unintended bias. Google’s (GOOG)(GOOGL) missteps with Gemini are a recent lesson on how difficult it is to tune an AI system to account for biases and ambiguity. However, Alphabet, Meta (META) and Amazon (AMZN) are also taking the challenge seriously and stepping up their investment in AI ethics and safety. Meta currently has around 40,000 people working on safety and security, with more than $20 billion invested in teams and technology in this area since 2016. Google’s Vertex AI platform provides a suite of tools that cater to the entire AI lifecycle, from data preparation to model deployment and monitoring. By integrating robust security measures, promoting transparency through explainable AI and adhering to stringent ethical guidelines, Vertex AI empowers businesses of all sizes to develop and deploy AI solutions with confidence.

Misinformation and Social Manipulation

AI and Gen AI in particular make it much easier for bad actors to spread misinformation. We have already seen AI being used to impersonate individuals, including the two leading candidates for the U.S. presidential election in 2024. Meta and Google are working to thwart the misuse of AI-generated content on their respective platforms. In August 2023, Google debuted a watermark software for AI content, letting the user know that the content is AI generated. Meta meanwhile ensures its AI-generated content is labeled “imagined with AI” and is expanding this feature to include content created by third-party tools. The company is also focused on election transparency, namely serving over 500 million notifications on its apps since 2020 informing users how and when to vote, and building an industry-leading library of political ads that is publicly available and elucidates the entity funding each ad and who they are targeting. Given how quickly the tools are evolving, including high-quality AI-generated video in the near future, this remains an open area of both risk and opportunity for the world’s leading digital media platforms.

AI’s Potential in Health Care

The growth and increasing complexity of data in health care also makes AI potentially transformative in the sector. In drug discovery and development, for example, some companies are successfully using AI to create and optimize molecules to go into development, largely with applications in chemistry and protein engineering. Some companies are hoping to use AI to pick better targets for drugs, although we are skeptical about the near-term prospects, as the complexity of biology may pose a challenge for current AI models. Other companies are hoping to use AI and advanced computer models to better design clinical trials, although these attempts are in the very early stages.

There is also significant potential for AI in the field of diagnostics, both traditional testing and advanced genetic tests. For traditional methods of diagnosis, like blood/serum based tests and images such as X-rays, CTs and MRIs, AI should be useful for prescreening, enhancing or even replacing human reading of test results. AI models have already been used to develop tests looking for patterns of genes that indicate cancers or the prognosis for cancer.

Along these lines, Hologic (HOLX), a medical technology company focused on women’s health and the leading manufacturer of mammography machines, is incorporating AI in its breast imaging business to assist radiologists in locating possible breast cancer lesions. Siemens Healthineers (OTCPK:SEMHF) (OTCPK:SMMNY), one of the leading manufacturers of CT and MRI machines, is also incorporating AI into its imaging platforms, which provide automatic post-processing of imaging datasets through AI-powered algorithms in order to reduce basic repetitive tasks and increase diagnostic precision when interpreting medical images. The company is the global leader in AI patent applications in health care.

Conclusion

The rapid ascension of large-language model AI in 2023 has made the technology relevant to companies’ futures in nearly every sector. It will be important for AI to be firmly tied to sustainable futures, and we will continue to monitor how ClearBridge portfolio companies and the market at large are navigating AI’s sustainability-related opportunities and risks.

Derek Deutsch, CFA, Managing Director, Portfolio Manager

Mary Jane McQuillen. Head of ESG, Portfolio Manager

|

1 “AI Will Transform the Global Economy. Let’s Make Sure It Benefits Humanity,” Kristalina Georgieva, IMF Blog. Jan. 14, 2024. 2 Barclays Live – 2030 Thematic Roadmap: 150 Trends (Edition 5) – Managing AI’s blind spots 3 “Retraining and Reskilling Workers in the Age of Automation,” Pablo Illanes, Susan Lund, Mona Mourshed, Scott Rutherford, and Magnus Tyreman, McKinsey. Jan. 22, 2018. Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. |

{kind=link}