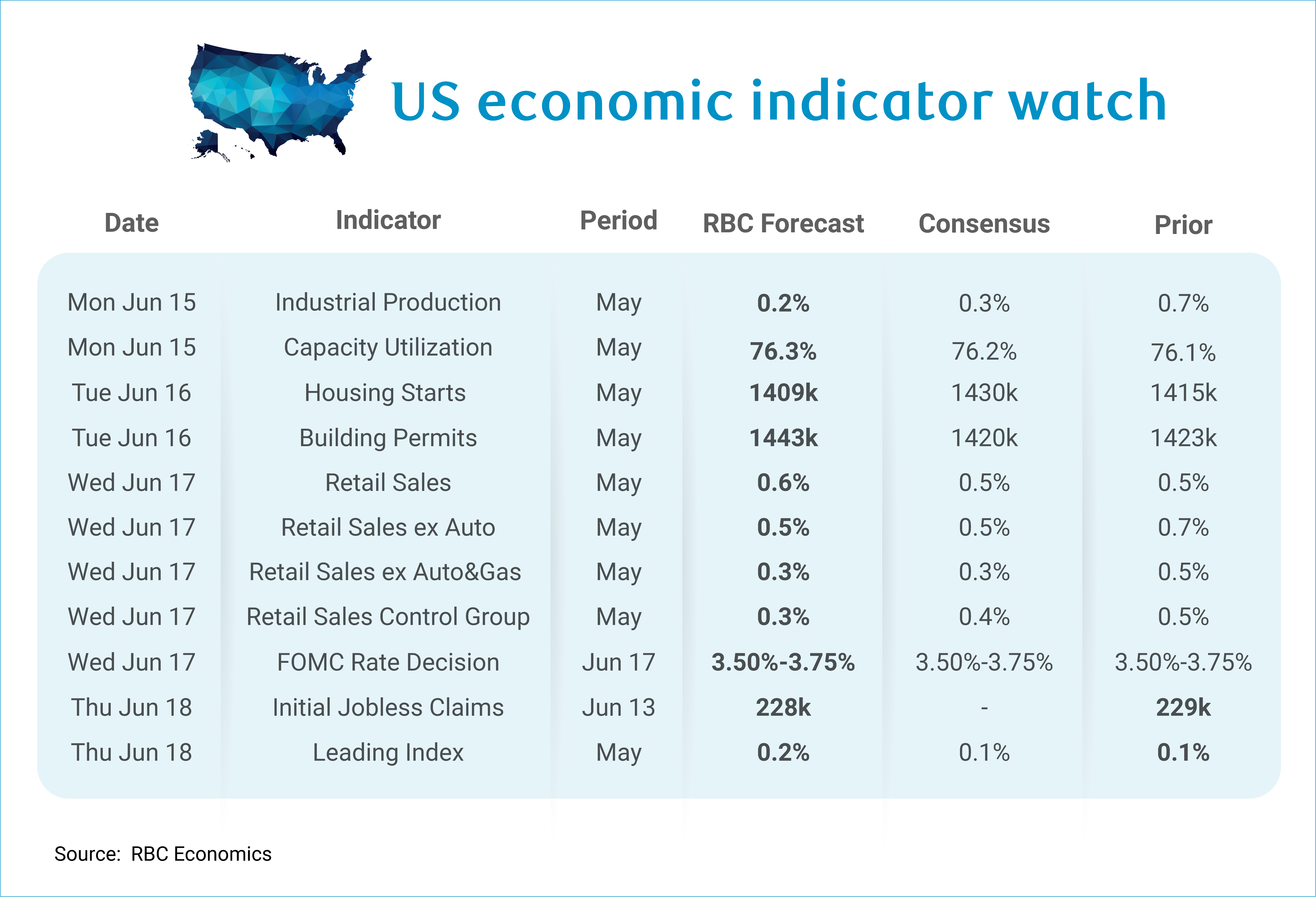

Next week the focus will be on retail sales data as energy prices continue to weigh on consumers. A lackluster report could overshadow the June 17 FOMC meeting, in which we expect no changes to interest rates. However, the bigger event will be the change in leadership as Kevin Warsh takes the reigns at his first meeting as chairman. His first notable change will likely be new language to the Fed’s statement.

The April meeting saw the highest number of dissents since 1992, with most reflective of a pivot language towards two-sided risk. And that’s what current data suggests following a reacceleration in inflation data for May alongside a sizeable upside to nonfarm payrolls and stable unemployment rate. We continue to expect the Fed will remain on hold for the remainder of 2026.

Indeed, the consumer will be top of mind, as we expect the May retail sales report will highlight a theme that we emphasized previously: in the face of higher inflation, consumers maintain spending at the expense of saving. Nominal retail spending is expected to look strong for a third consecutive month in May – we forecast headline retail sales will rise +0.6% m/m. Even stripping out the impact of autos and gasoline sales, we forecast retail sales rose +0.3% m/m.

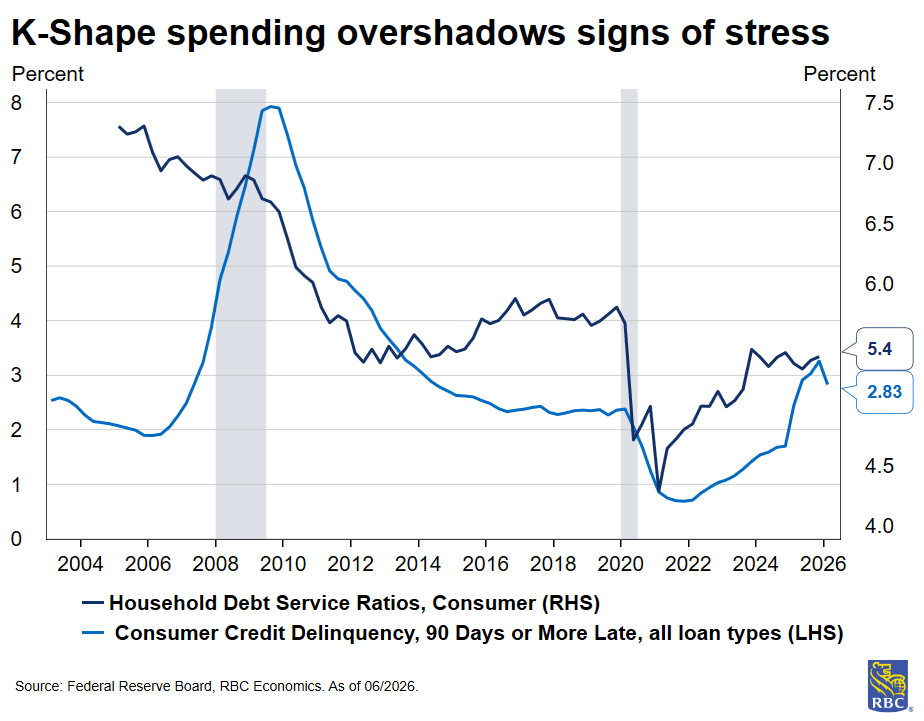

Even stripping out the impact of autos and gasoline sales, we forecast retail sales rose +0.3%. While that sounds robust, in reality, it is in-line with the pace of headline inflation, meaning REAL retail sales will register flat. The consumer is losing steam – real wage growth is negative, the saving rate is falling, and revolving credit is on the rise after pulling back slightly in February.

We wrote earlier that the US economy can absorb the energy shock, and that we do not expect the spike in gasoline prices to lead to demand destruction. The personal savings rate has fallen by a full percentage point (from 3.6% to 2.6%) between February and April. We also estimate higher tax refunds are acting as a meaningful counterweight in absorbing higher gas prices, for now.

Aside from retail sales and the Fed meeting, here’s what else we’re watching next week:

-

Industrial production is expected to tick up by +0.2% m/m after the Manufacturing production index (54.3) signaled continued expansion in May and hours worked held up in the manufacturing sector. This would bring the capacity utilization rate to 76.3%.

-

Our forecast calls for building permit issuance to rise in May. But housing starts did not likely move much.

-

Initial Jobless Claims are expected to report 228k for the week ending June 13th. We expect the low fire environment to continue, as CPI and PPI data signals firms continue to pass higher costs along to consumers.

-

We expect to see the Conference Board’s Leading Index (LEI) improved (+0.2% m/m). Of the ten sub-indices that feed into the LEI, most sub-components either improved or were unchanged.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.