The US–Iran military escalation triggered a sharp risk-off phase across global markets, with crude oil prices surging, bond yields hardening, and concerns around global growth intensifying. Indian equities were no exception. Between February 28, 2026 and April 17, 2026, the Nifty 500 fell sharply during the period before recouping most of the losses, ending only 1.3 per cent lower. But beneath the headline index, the factor strategies showed a clear divergence. These are rule-based portfolios built around specific stock traits such as value, quality, momentum, alpha or low volatility. The quality factor emerged as the outperformer, while the low volatility factor, typically viewed as defensive, lagged the most.

To understand how these strategies behaved during the recent turmoil, we analysed the Nifty500 Value 50, Nifty 500 Low Volatility 50, Nifty500 Quality 50, Nifty500 Momentum 50, and Nifty Alpha 50 indices based on total return performance. Following the onset of the conflict, markets saw a sharp drawdown, with indices bottoming out on March 30. The Nifty 500 fell 11.3 per cent during this phase. The Quality index proved relatively resilient, declining the least at 8 per cent, while momentum and alpha saw the steepest falls of 12.2 per cent. Low volatility and value declined 10 per cent and 11 per cent, respectively.

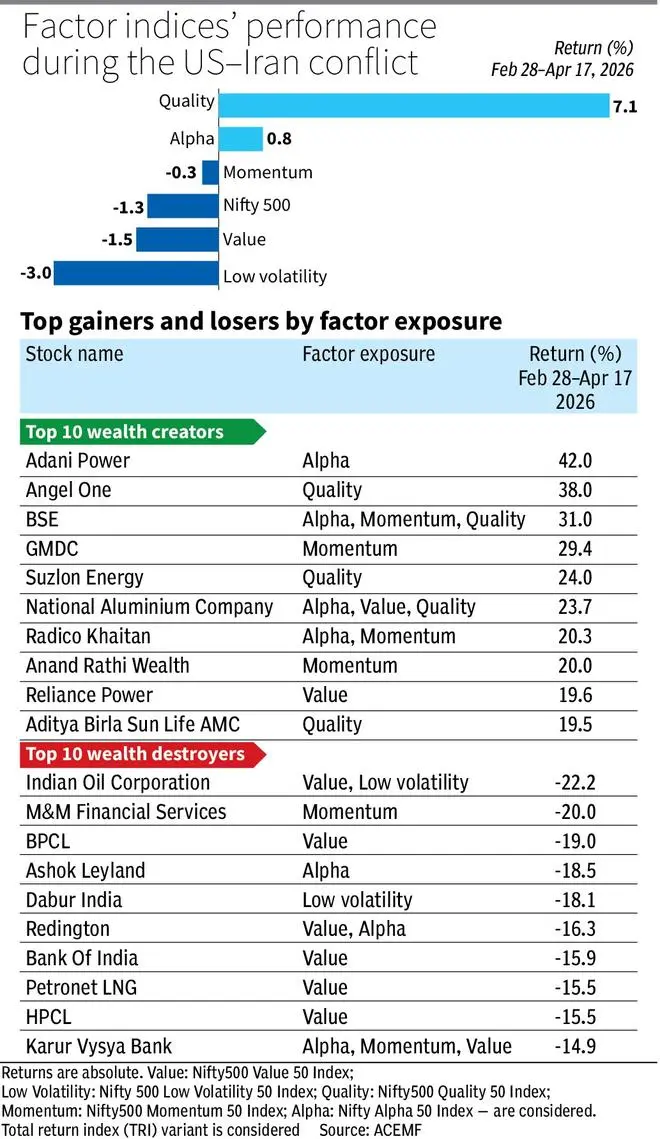

As sentiment improved, markets staged a recovery. Between February 28 and April 17, during the conflict period, the quality index topped the returns chart with a gain of 7.1 per cent, comfortably outperforming the Nifty 500, which remained down 1.3 per cent. In contrast, low volatility (-3 per cent) and value (-1.5 per cent) lagged even the broader market, while momentum (-0.3 per cent) and alpha (0.8 per cent) managed to contain losses.

In India, around 117 factor-based funds, managing nearly ₹51,000 crore as of March 2026, deploy rule-based strategies across momentum, alpha, low volatility, quality, and value. These frameworks aim to capture distinct drivers of returns in a transparent and cost-efficient manner.

Quality

The Quality factor outperformed during the ongoing conflict, driven by its tilt toward companies with strong balance sheets, high return ratios, and stable earnings. Its sector mix, including private-sector financials, IT, consumer businesses, and select pharma, provided resilience in a risk-off environment.

Parts of the portfolio also benefitted from favourable market dynamics. Capital market-linked stocks such as Angel One, BSE and Anand Rathi Wealth surged 38 per cent, 31 per cent, and 20 per cent, respectively during the period between February 27 and April 17. Metals and mining names, including National Aluminium (up 24 per cent) and NMDC (up 10 per cent) gained.

Exposure to defence and industrial themes added further support. Stocks such as ABB India, Mazagon Dock Shipbuilders, and Zen Technologies rose 16–19 per cent during the period, driven by expectations of better earnings growth on possible higher defence spending. These gains helped offset weakness in consumption-oriented names such as Britannia and Colgate-Palmolive, which fell 5 per cent and 7 per cent, respectively, amid cost pressures and subdued demand. Additionally, select IT and pharma names, including Persistent Systems and Natco Pharma, delivered notable gains.

In hindsight, this positioning may have enabled the quality index to provide both downside protection and modest positive returns.

Low volatility

The most notable underperformance came from the Nifty 500 Low Volatility 50 index, which declined by 3 per cent. This outcome highlights that not all defensive factors behave similarly across different types of crises. Low volatility strategies typically select stocks with stable price movements based on historical standard deviation, aiming to limit drawdowns and improve risk-adjusted returns. However, they often carry higher exposure to defensive sectors such as utilities and consumer staples. Utilities are particularly vulnerable to rising yields, as seen during the conflict period, while staples can be hurt when inflation and input costs rise.

Large FMCG names such as Dabur, Colgate-Palmolive, and Godrej Consumer Products saw steep corrections of 7–15 per cent. Insurance and financial stocks also declined as bond yields hardened and growth concerns intensified. ICICI Prudential Life Insurance, HDFC Life Insurance, and SBI Cards and Payment Services fell in the 10–14 per cent range.

Notably, the index had limited exposure to metals, defence, capital market infrastructure, and energy. These are the sectors that drew investor interest during the geopolitical escalation. While select stocks such as Page Industries, Tata Power, and Tech Mahindra gained 11–18 per cent, their weights were insufficient to offset broader losses.

This underperformance suggests that low volatility strategies may fare better in growth slowdowns or earnings-led corrections, but can struggle in inflationary or supply-shock-driven environments.

Momentum

Momentum and alpha factors, though negative, showed relative outperformance compared to the broader market.

The alpha index benefitted from a few standout performers, most notably Adani Power that gained 42 per cent. Exchange and commodity-linked plays such as BSE and MCX, along with metals like National Aluminium, also contributed positively. However, these gains were offset by substantial losses in PSU banks, auto majors, and select financial stocks, which form a significant part of the alpha basket. Stocks such as Ashok Leyland (-17 per cent), Bank of India (-16 per cent), Karur Vysya Bank (-15 per cent), and Eicher Motors (-10 per cent) were a drag on performance.

Momentum strategies, which chase recent outperformers, drew some support from exposure to capital markets and select pharma, capital goods, and energy names. However, names such as Bajaj Finance, Cholamandalam Investment Finance, and Mahindra Finance recorded steep declines of 9–20 per cent. Auto stocks, which had strong prior momentum, also corrected sharply.

Overall, the episode highlights a key limitation of momentum investing: during sudden external shocks, past trends can break down quickly, exposing these strategies to drawdowns.

Value

The Nifty 500 Value 50 index, which tracks relatively undervalued stocks, is often seen as better placed in market corrections. Yet, it fell 1.5 per cent and lagged the Nifty 500.

Top gainers included National Aluminium, Reliance Power, Hindalco Industries, and NMDC, which delivered gains of 10–24 per cent. However, Indian Oil, BPCL, and HPCL declined sharply by 16–22 per cent as rising crude prices stoked concerns over their marketing margins.

Value indices also carry significant weights in PSU banks. Stocks such as Bank of Baroda, Punjab National Bank, SBI, and Bank of India posted double-digit losses of up to 16 per cent. Thus, losses in OMCs and PSBs more than offset the gains in metals, causing the index to lag.

Takeaway

The US–Iran conflict offered a live stress test for factor strategies, revealing how differently they behave under geopolitical and inflationary shocks.

Quality emerged as the clear winner, rewarding investors with both downside protection and positive returns. Momentum and alpha, while negative, managed to contain losses better than the broader market, aided by select sector tailwinds. Low volatility was a disappointment, showing that a defensive tag does not always mean safety in such crises. Value, too, underwhelmed, showing that lower valuations alone do not guarantee resilience in every correction.

The lesson for investors is that they should evaluate factor strategies not just on historical risk metrics, but also on their underlying sector composition and macro sensitivity before investing.

Published on April 18, 2026