Global markets are wrestling with mixed signals, from firm US consumer spending and persistent inflation readings to ongoing policy support and industrial strength in China. In this setting, many investors are looking past short term headlines and focusing on companies where analysts see healthy earnings growth potential and balance sheets that can handle bumps along the way. This is exactly what the Healthy high growth potential screener targets. It highlights stocks that combine expected earnings growth over the next 3 years with acceptable financial positions. Below, the article reveals 3 of the best stocks from this screener to consider for further research.

Kioxia Holdings (TSE:285A)

Overview: Kioxia Holdings is a Japanese semiconductor company that designs, manufactures, and sells flash memory chips and solid state drives used in data centers, smartphones, PCs, and other smart devices across Japan, North America, Europe, and Asia. It also supports these products with software development, energy management services, and engineering and customer support operations.

Operations: Kioxia generates all of its ¥2,337,628m revenue from its Memory Business, with sales spread across markets such as the United States, China, Japan, Taiwan, and the rest of Asia and Europe.

Market Cap: ¥50.3t

Investors looking at Kioxia Holdings are seeing a pure play on memory used in AI data centers, with earnings forecast to grow strongly and a net profit margin of 23.7% that is higher than last year. The stock has attracted attention after a very large share price move in 2026. However, it still trades well below one estimate of fair value based on future cash flows, which suggests the market may not be fully pricing in its earnings potential. At the same time, a very high P/E, heavy reliance on external borrowing, sharp share price swings, and an active patent investigation mean risk is clearly part of the story.

Kioxia Holdings appears to be a pure AI memory play, with earnings forecasts and profit margins pointing one way, while a very high P/E and heavy borrowing tell another. Get the full picture with the 3 key rewards and 2 important warning signs (1 is major!)

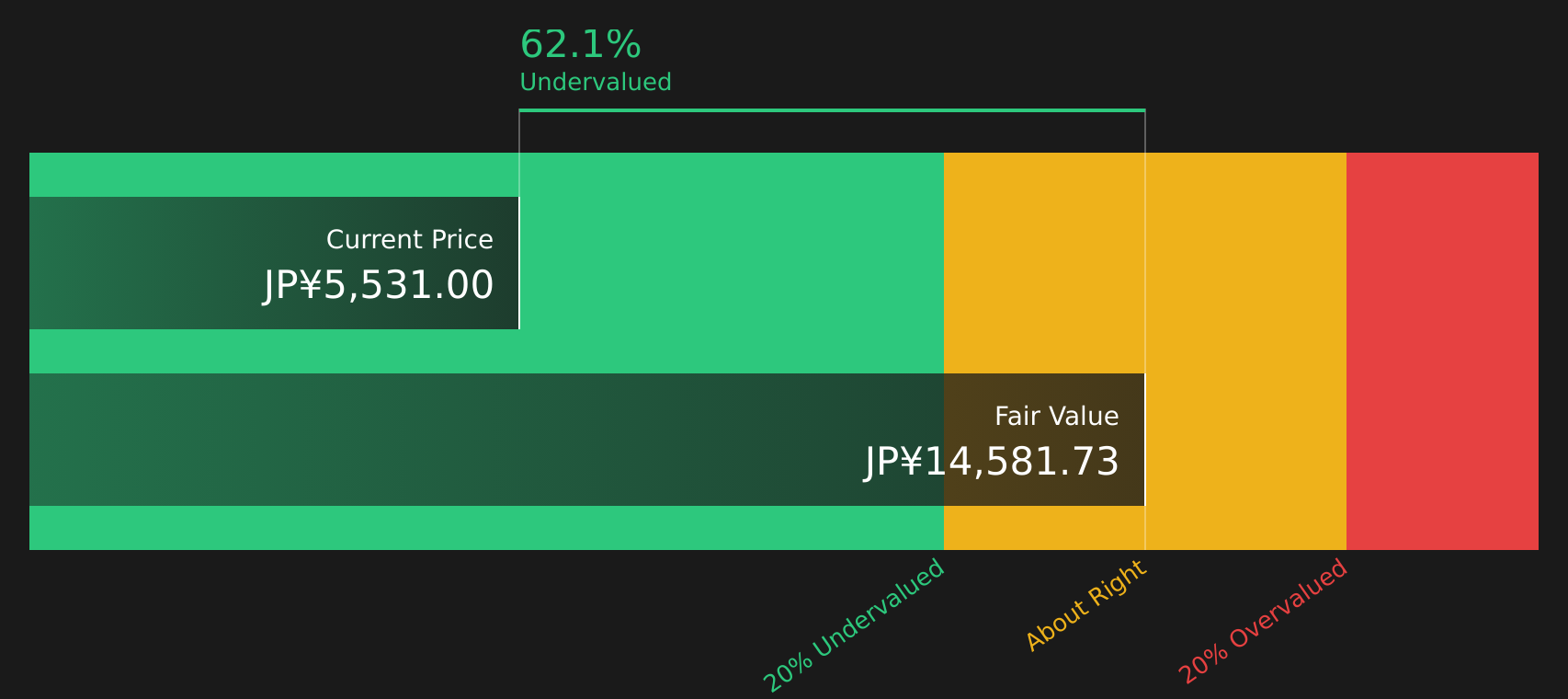

Baycurrent (TSE:6532)

Overview: Baycurrent is a Japan based consulting group that helps companies plan and execute projects across AI, digital transformation, sustainability, corporate finance, operations, and IT systems, serving clients in sectors from finance and industrials to healthcare, telecoms, retail, and energy.

Operations: Baycurrent generates all of its ¥148,332m revenue from its Consulting Business in Japan.

Market Cap: ¥834.0b

Baycurrent appears in a growth focused screener because it combines double digit earnings growth, high quality profits, and a 32.3% Return on Equity with a share price that some analysts view as trading well below their estimate of fair value. Forecast earnings and revenue growth above 20% a year indicate that the consulting model is scaling, while margins above 25% point to strong pricing power with blue chip clients. At the same time, a relatively high P/E, elevated share price volatility, full reliance on external borrowing, and generous CEO pay highlight that execution risk is significant. For investors comfortable with those trade offs, Baycurrent is the kind of stock that may merit closer analysis beyond the headlines.

Baycurrent’s earnings growth and high margins are grabbing attention, but the real story may lie in how those expectations compare with today’s valuation and volatility, as outlined in the analyst forecasts for Baycurrent

Furukawa Electric (TSE:5801)

Overview: Furukawa Electric is a Japanese industrial group that supplies optical fiber and network gear, power cables and energy infrastructure, auto wire harnesses, and metal products that sit behind everything from telecoms networks to electric vehicles and factories worldwide.

Operations: Furukawa Electric generates most of its ¥1,300,558m revenue from Electrical Electronics at ¥765,067m, followed by Infrastructure at ¥370,856m, Functional Products at ¥161,089m, Service, Development, Etc. at ¥42,208m, and an unallocated adjustment of ¥31,662m.

Market Cap: ¥3.2t

Furukawa Electric catches the eye in a growth focused screener because earnings are forecast to rise around 21.6% a year, with recent profit growth and a higher net margin of 5.5% pointing to use of its broad portfolio in optical networks, auto wire harnesses and energy infrastructure. Revenue is also projected to grow faster than the Japanese market, and index additions in 2026 may increase attention from larger investors. At the same time, a P/E above peers, heavy use of external borrowing and very volatile trading mean you are paying up while accepting higher risk. With board changes still bedding in and one off items affecting recent results, the question is whether this growth story can justify today’s richer valuation.

Furukawa Electric’s rising earnings forecasts, profit growth and richer P/E hint at a story where growth and risk may be pulling apart, and the real tension sits inside the analyst forecasts for Furukawa Electric

The stocks covered here are just a starting point, with the full Healthy high growth potential screener surfacing 60 more companies that analysts expect to post strong earnings growth while keeping their financial position within set criteria through the Healthy high growth potential screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction ideas from that broader list.

Take Control of Your Investment Journey

If Furukawa Electric or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Momentum Flies?

New stock ideas can move from quiet to flying quickly, so use fresh screeners to spot potential breakouts before the crowd, while it matters, and get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Kioxia Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com