Gold managed to bounce a bit on Friday, although it was too little to prevent a weekly decline. On the week, the metal fell 2.5%, making its second consecutive weekly decline. Though gold again managed to hold its own above the key $4,000 level on a daily and weekly closing basis, the metal was now flat on the month. The struggles come as the dollar was looking to steady itself after suffering a double dose of inflation surprises last week with both CPI and PPI coming in weaker than expected. Meanwhile, we saw a bit of a risk off trade creeping into the stock markets with chipmakers under pressure on Wall Street, while Europe was again troubled by the escalation of tensions in the Middle East. We will maintain a modestly bearish view on the near-term gold outlook heading into the new week.

What factors have weighed on the gold outlook?

While the weaker inflation data from the US held back the dollar against certain currencies, it is worth remembering that one month’s worth of data is not going to impact the Fed’s thinking much and that’s something Chris Waller highlighted during the week. Waller, like most of his other FOMC colleagues, wants to see a clear disinflationary trend over the course of a few months. That’s not going to be the case if oil prices now remain elevated after making a comeback in recent days due to the re-escalation of tension between the US and Iran.

Even if some of the near-term economic data softens, persistently high energy prices would make it difficult for the Fed to adopt a more dovish stance. That is one of the reasons why we’re seeing the US dollar regained a bit of momentum towards the end of last week, particularly against currencies whose economies are heavily reliant on imported energy, or those where interest rates are low, such as the Swiss franc and the Japanese yen. For the same reason, investors are preferring the dollar over the zero-yielding gold.

On top of these macro factors, momentum has been completely lost in gold which is discouraging speculative traders wanting to ride the wave. While gold was flattish on the monthly time frame thanks to a small recovery on Friday, the yellow metal has been on a monthly losing streak. It fell more than 11% in June, which was its fourth consecutive losing month. Thus, the path of least resistance and the gold outlook remain modestly to the downside, and I am still expecting a breakdown below the $4,000 level soon.

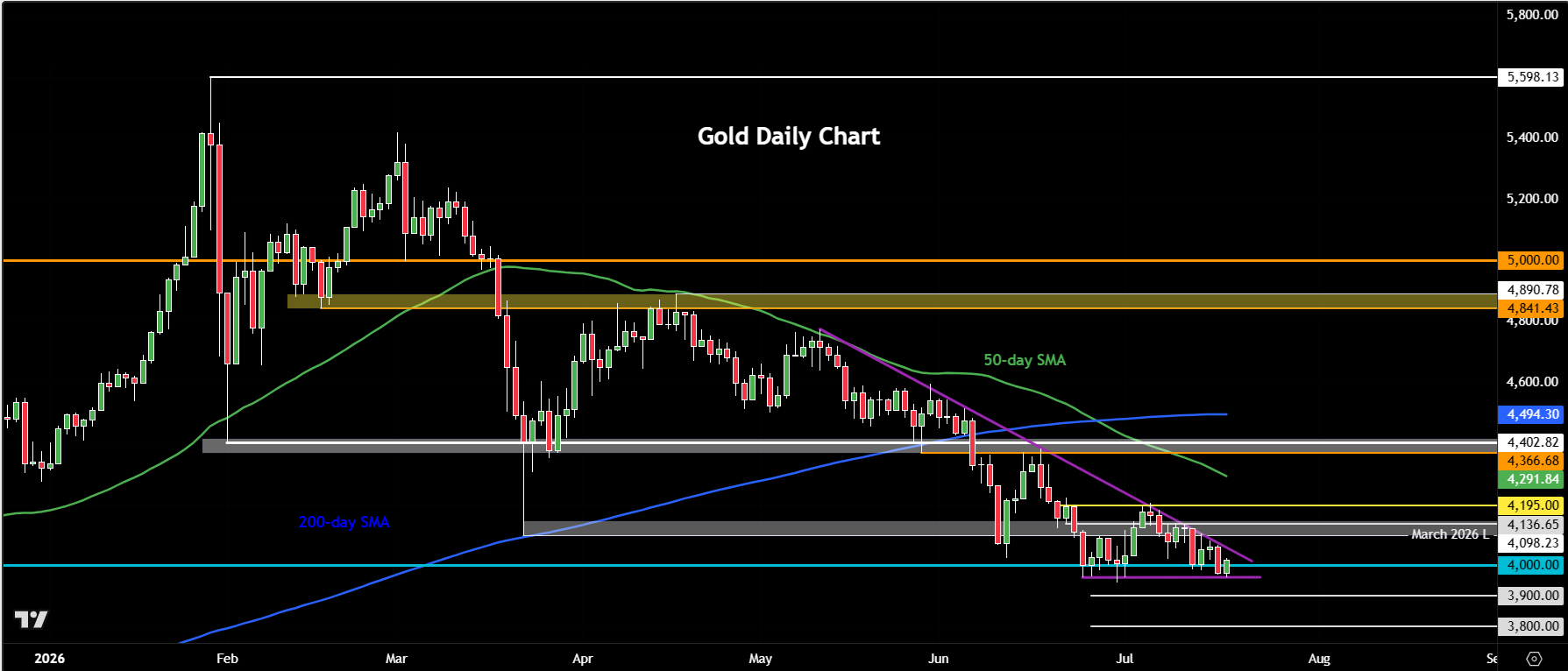

Technical gold outlook and key levels to watch

From a technical analysis point of view, our gold outlook remains bearish. The metal has struggled in recent days to climb back above the $4,100 level, and instead it has remained below both the bearish trend line and the 21-day exponential average. The 50-day crossed below the 200-day average not so long ago and that further aids the bearish narrative.

Thus, I’m looking for a break below the $4,000 level in the days ahead. If we get a daily close beneath it, then the next downside targets come in around $3,900, followed by $3,800.

Resistance above the $4100 area comes in around $4,136 initially, followed by $4,200 and then at $4275.

In short, with energy prices firming and little evidence that the US economy is slowing enough to offset inflation risks, the fundamental backdrop continues to favour the dollar. That leaves zero- and low-yielding assets like the yen, franc and gold particularly vulnerable.

Week ahead: UK CPI, ECB rate decision and global PMIs

The data calendar for the week ahead doesn’t look particularly important for the gold outlook, although the metal may still get some indirect reaction from the reaction of foreign currencies against the US dollar.

UK CPI is due on Wednesday, July 22. Uk inflation has been moderating in recent months, falling to 2.8% y/y in May and it is expected to fall further in June. Analysts expect a headline rate of 2.7%. Core CPI is also expected to fall to 2.5% from 2.6%. If inflation proves to be weaker, then this may provide some downward pressure on GBP. In any case, rising oil prices risk reviving stagflation concerns, which could keep pressure on GBP/USD.

ECB’s rate decision is on Thursday, July 23. Although ECB policymakers are widely expected to leave interest rates unchanged, rising energy prices have injected a degree of uncertainty into the outlook. Higher oil prices threaten to revive inflationary pressures while simultaneously weighing on economic growth, raising the spectre of stagflation. Some policymakers may therefore argue for maintaining a hawkish bias to preserve the ECB’s inflation-fighting credibility.

Global PMIs are due for release on Friday, July 24. The PMI surveys will offer a timely snapshot of business activity across the major economies and could shape expectations for both European growth and the direction of the euro over the coming weeks. Also worth keeping an eye on UK PMIs where the economy faces similar challenges (high oil and low growth).