RobsonPL

Credit Agricole (OTCPK:CRARF) offers a high-dividend yield that is sustainable, being the most attractive feature of its investment case.

Company Overview

Credit Agricole is based in France and is one of Europe’s largest banks, measured by its total assets of close to €2.2 trillion at the end of 2023. While the bank is currently present in 46 countries around the world, most of its business is generated in its domestic market, which represents the vast majority of its revenues and earnings.

Its current market value is about $41 billion, and its shares trade in the U.S. on the over-the-counter market. Its closest competitors are other large French banks, including Societe Generale (OTCPK:SCGLY) and BNP Paribas (OTCQX:BNPQY).

Its business is well diversified across retail and commercial banking, insurance, corporate and investment banking, and asset management. It’s the largest shareholder in Amundi (OTCPK:AMDUF), one of the world’s largest asset managers with assets under management of about $2.5 trillion, with a stake of almost 70%.

Credit Agricole has a different business structure than compared to other European banks because it’s part of a mutual and cooperative group, which has a more complex organization than other financial institutions in the region. At the top of the group, there are about 11.5 million shareholders, who hold stakes in local and regional banks, which in turn hold the majority (56%) of Credit Agricola SA, which is the banking arm of the group, while the rest trades as free float.

While its operations are diversified across several segments of the financial industry, its most important business is retail banking in France, being one of the market leaders in the country. It’s one of the few banks in Europe that maintain a bancassurance business model, which means both banking and insurance are considered core businesses, operating under a cross-selling network approach.

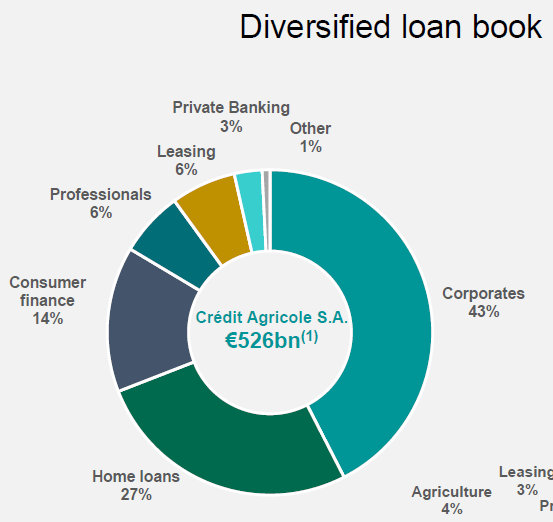

Compared to its closest French peers, Credit Agricole has lower exposure to corporate and investment banking, while it’s more exposed to life insurance and asset management. This means its business profile is less related to capital market activities and should be more stable and recurring over the long term, due to its higher reliance on retail banking and insurance. Its good business diversification is also visible in its loan book composition, which has exposure to several types of clients and activities, as shown in the next graph.

Loan book (Credit Agricole)

Regarding its growth prospects, they are somewhat muted given that the bank is highly exposed to France, which has a mature financial industry and relatively low economic growth potential, a profile that is not expected to change much in the near future. Therefore, Credit Agricole is expected to maintain a relatively stable performance over the long term, considering also that the bank’s risk profile is conservative and large acquisitions are not much likely in the foreseeable future.

Financial Performance

Regarding its financial performance, Credit Agricole has delivered a relatively stable performance over the past few years, even though more recently its revenues and earnings have been supported by higher interest rates.

Indeed, in 2023, Credit Agricole’s revenues amounted to €24.5 billion, an increase of 9.5% YoY, driven by higher net interest income and some small acquisitions in specialized finance. However, as I’ve analyzed some months ago on SocGen, the French banks are amongst the least exposed to higher rates in Europe due to some specific issues in the French banking system.

While most European banks, especially those with a balance sheet more geared to variable-rate loans, have reported strong NII growth across the past few quarters, French banks have reported much lower NII growth compared to its peers. This happens because the French government regulates both mortgage lending rates and deposit rates for some saving products, putting a significant cap on how much French banks can gain from higher market rates.

Nevertheless, due to Credit Agricole’s diversified business model, it was able to report higher revenue growth than SocGen, but still much lower than other European banks that are much more geared to rates.

Revenues (Credit Agricole)

On top of revenue constraints, on the cost side, French banks also have much less leeway to reduce expenses than its European competitors, as the labor law in France is not particularly business-friendly. This makes the bank’s cost base somewhat sticky and explains why French banks are amongst the least efficient banks in Europe, measured by cost-to-income ratios above 60%, while the most efficient banks have cost-to-income ratios closer to 40%.

Moreover, the inflationary environment over the past couple of years was also another challenge for French banks, and Credit Agricole was no exception. Its annual expenses increased by 8.9% YoY in 2023, which means the bank’s operating jaws (revenue growth minus cost growth) were quite low.

This is a negative outcome considering that most European banks improved considerably their efficiency levels over the past year, as revenue growth was generally much higher than cost growth, a profile that was not achieved by French banks. Nevertheless, Credit Agricole improved a little bit its efficiency and reported a cost-to-income ratio of 55%, which is not amongst the best in Europe, but compares well with BNP Paribas (cost-to-income ratio of 69%) and SocGen (73%).

Credit Agricole’s cost-to-income ratio was already below its 2025 target of being below 58%; thus the bank seems to be comfortable with its efficiency level and therefore cost-cutting is not expected to be an important factor for earnings growth over the next few years.

Regarding its asset quality, it has remained at good levels, given that its cost of risk ratio was 33 basis points (bps) in 2023, a level that was relatively unchanged from the previous year. In the medium term, Credit Agricole expects its cost of risk ratio to be about 40 bps, which means its annual provisions should remain at acceptable levels during the next few years if economic conditions remain supportive in Europe and the unemployment rate doesn’t increase much in the near term.

Credit Agricole’s positive operating momentum was also visible in its bottom-line, given that its net income increased by 11% YoY to €5.9 billion, and its return on tangible equity (RoTE) ratio, a key measure of profitability in the banking sector, was 12.6%.

Regarding its capital position, the bank had a CET1 ratio of 11.8% at the end of 2023, a level that is below the average of the European banking sector. While its CET1 ratio is somewhat lower than compared to its peers, it’s quite comfortable above its capital requirements, which is currently a level of 8.2%, thus Credit Agricole has an acceptable capital position.

This is an important support for its shareholder remuneration policy, which is focused on its dividend. Its track record is quite positive, as the bank has been able to deliver a growing dividend over the past few years.

Dividend (Credit Agricole)

However, its last annual dividend, related to 2023 earnings, was unchanged from the previous years at €1.05 per share, even though some part of its dividend in the past couple of years was related to its dividend suspension during the pandemic (dividend suspension in 2020, related to 2019 earnings), thus its ‘normal’ dividend increased from €0.85 to €1.05 per share.

At its current share price, Credit Agricole offers a dividend yield of about 8.6%, which is quite attractive for income investors. While this could be a sign of a risky dividend, this is not, in my opinion, Credit Agricole’s case, given that its dividend payout ratio is only 58% based on underlying earnings, which is a very acceptable payout ratio and shows that the bank’s dividend is sustainable.

Going forward, its dividend is not expected to grow much in the coming years according to street estimates, given that analysts expect its earnings to be rather flat in the near future as the bank should be penalized by lower interest rates ahead.

Conclusion

Credit Agricole has a good business diversification, but its growth prospects are somewhat muted and the bank’s high exposure to its domestic market is not particularly positive over the long term due to some structural issues affecting the financial industry in the country.

This makes its high-dividend yield the most interesting feature of its investment case, which is justified mainly by a low valuation rather than poor dividend sustainability. Indeed, Credit Agricole is currently trading at 0.6x book value, at a significant discount to the European banking sector average at 0.92x book value. Despite this discount, I think Credit Agricole’s valuation is justified by its weaker growth prospects and capital position; thus, yield is the main reason to buy its shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}