The US dollar’s strengthening last year to a 20-year high had major

implications for the global economy. We examine these spillovers from the

currency’s appreciation in our latest External Sector Report.

Building on recent

research

by Maurice Obstfeld and Haonan Zhou, we find that negative spillovers from

US dollar appreciations fall disproportionately on emerging market

economies when compared with smaller advanced economies.

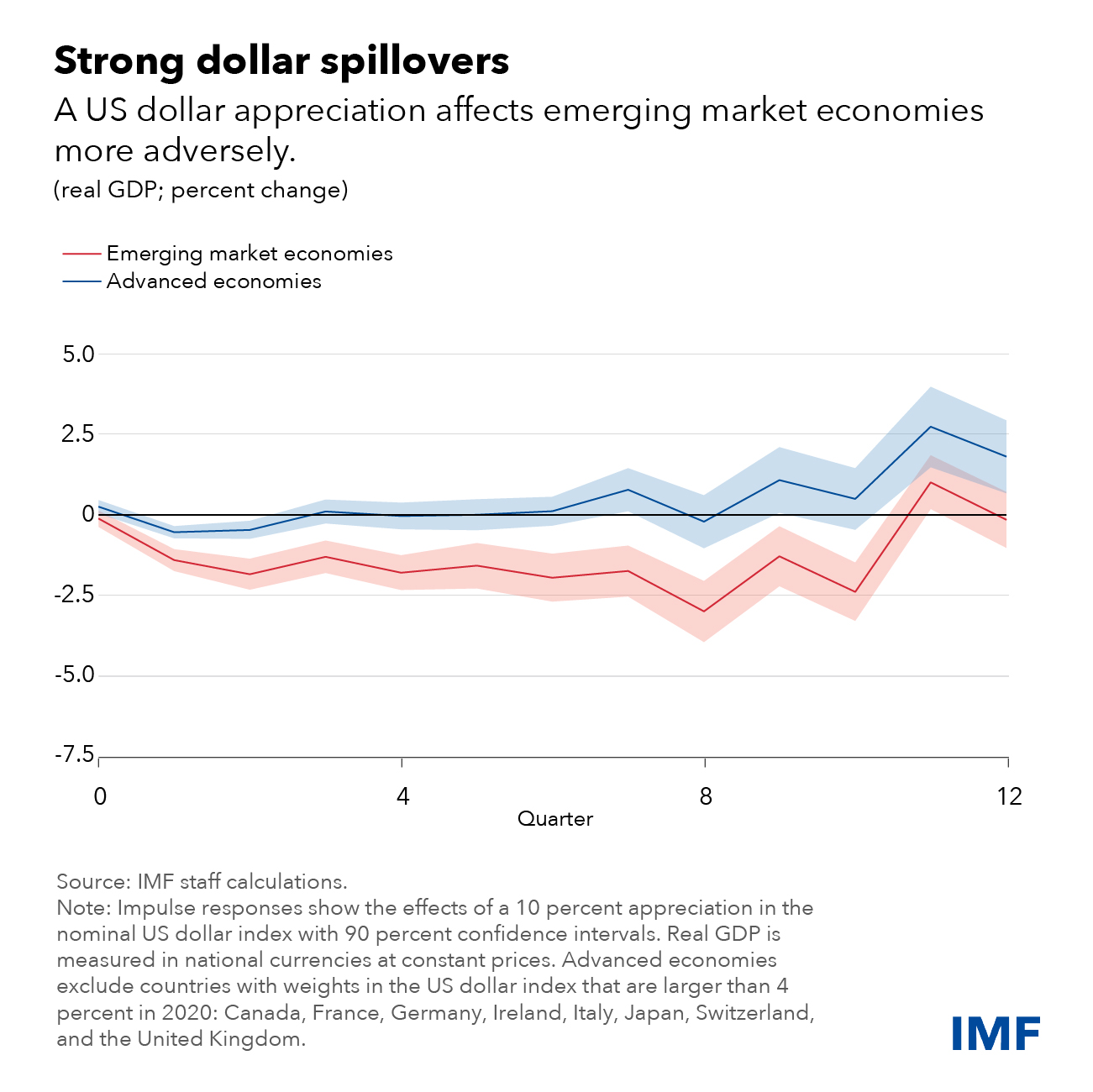

In emerging market economies, a 10 percent US dollar appreciation, linked

to global financial market forces, decreases economic output by 1.9 percent

after one year, and this drag lingers for two and a half years. In

contrast, the negative effects in advanced economies are considerably

smaller in size, peaking at 0.6 percent after one quarter and are largely

gone in a year.

In emerging market economies, the effects of the strong dollar spread via

trade and financial channels. Their real trade volumes decline more

sharply, with imports dropping twice as much as exports. Emerging market

economies also tend to suffer disproportionately across other key metrics:

worsening credit availability, diminished capital inflows, tighter monetary

policy on impact, and bigger stock-market declines.

External sector implications

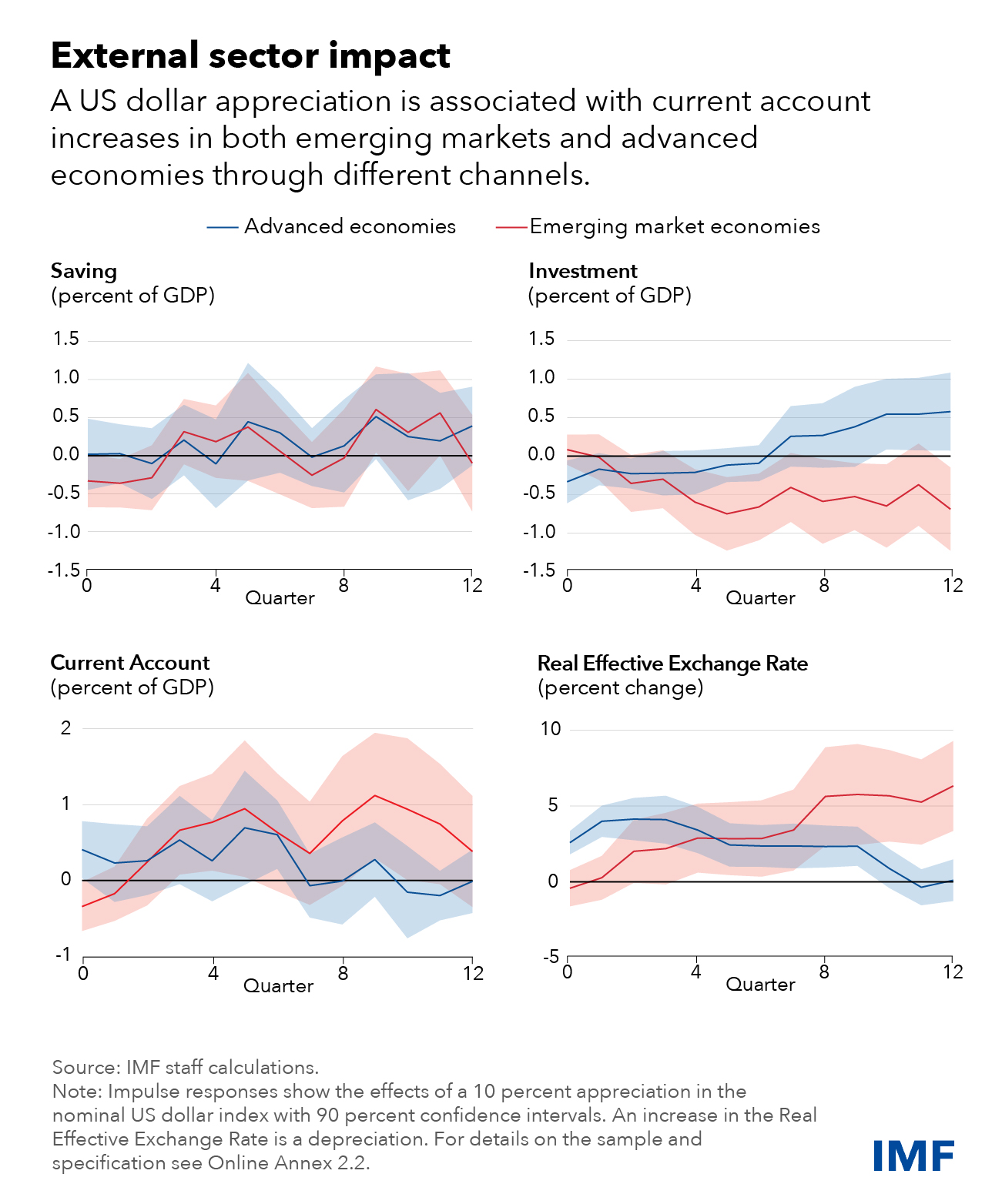

In addition, US dollar appreciations impact the current account, which

captures the change in saving-investment balances of countries.

As a share of gross domestic product, current account balances (saving

minus investment) increase in both emerging market economies and smaller

advanced economies, because of a depressed investment rate (there is no

clear systematic response for saving). However, the effect is larger and

more persistent for emerging market economies.

Exchange rate depreciation and accommodative monetary policy facilitate the

external sector adjustment for advanced economies. In emerging market

economies, fear of letting the exchange rate fluctuate and lack of monetary

policy accommodation magnify the increase in the current account.

There, the income compression channel—where lower income leads to a decline

in the purchase of imported items—plays a relatively bigger role. The

external sector adjustment in emerging market economies is further hindered

by their heightened exposure to the US dollar through trade invoicing and

liability denomination.

Policies

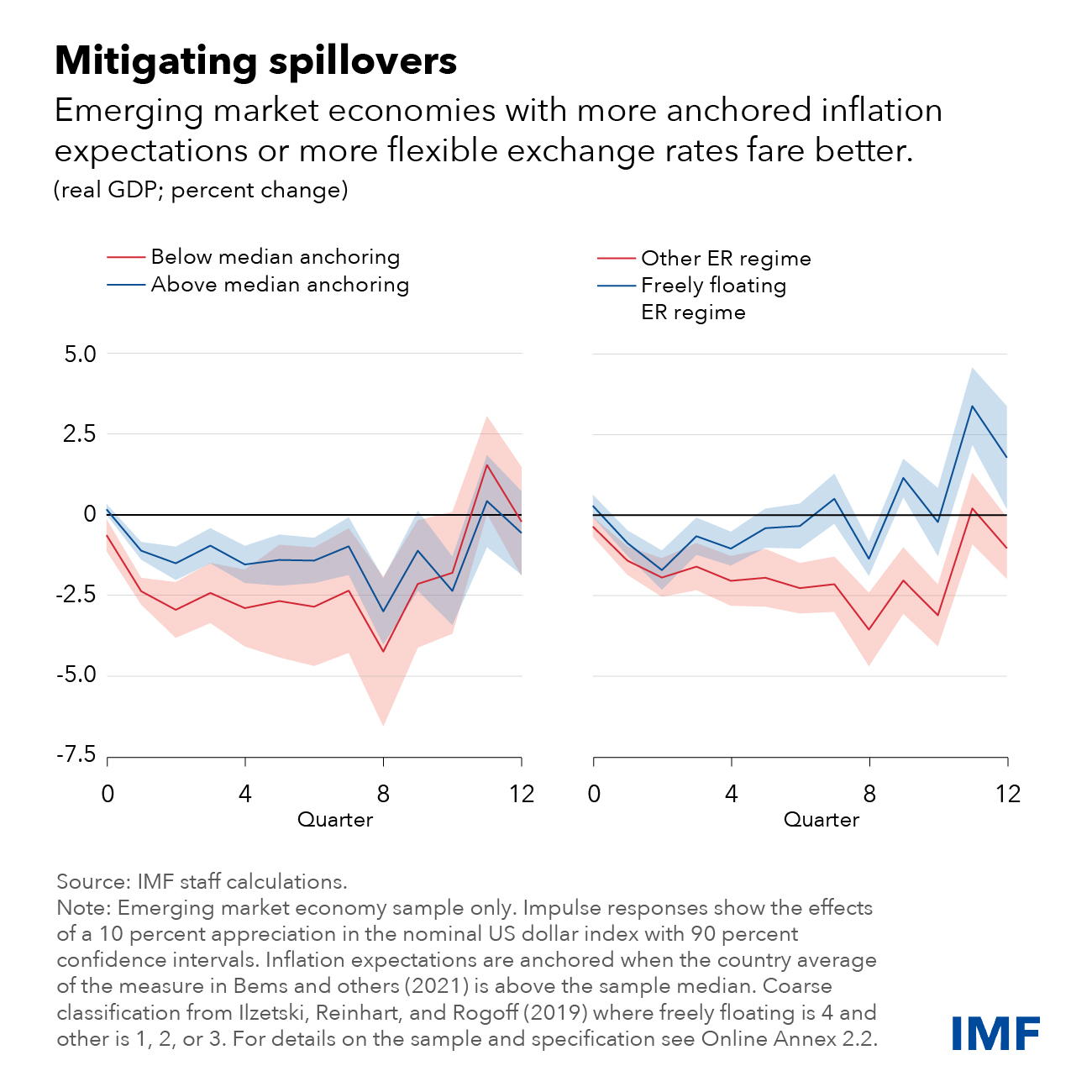

Emerging market economies with more anchored inflation expectations or more

flexible exchange rate regimes fare better.

More anchored inflation expectations help by allowing more freedom in the

response of monetary policy. After a depreciation, a country can run a

looser monetary policy if expectations are anchored. The result is a

shallower initial decline in real output. In turn, emerging market

economies with more flexible exchange rate regimes tend to enjoy a faster

economic recovery owing to a sizable immediate exchange rate depreciation.

Flexible exchange rate regimes can be

supported and facilitated by domestic financial market development that helps lessen the sensitivity of domestic borrowing conditions to the

exchange rate. Sustained longer-term commitments to improving fiscal and

monetary frameworks help anchor inflation

expectations. This includes ensuring a well-balanced mix of fiscal and monetary

policies, enhancing central bank independence, and continuing to strengthen

the effectiveness of communications.

Global effects

Global current account balances are calculated as the sum of absolute current account balances across

countries. It is a key metric in the IMF’s External Sector Report as it can

indicate increasing financial vulnerabilities and rising trade tensions.

Our research shows that a 10 percent appreciation is associated with a

decline in global current account balances by 0.4 percent of world GDP

after one year. The magnitude of the decline is economically significant,

as average global balances over the last two decades were about 3.5 percent

of world GDP, with a standard deviation of 0.7 percent.

The decline in global balances reflects a broad-based contraction in trade

in the presence of

dominant currency pricing, facilitated by narrowing commodity trade balances, given falling

commodity prices that have historically accompanied appreciations of the US

dollar.

In emerging market economies with severe financial frictions and balance

sheet vulnerabilities, macroprudential and capital flow management measures

could help mitigate negative cross-border spillovers.

{kind=link}