BlackJack3D

Technology and the digital transformation have been a strong macro trend that many investors have been riding for the past couple decades – with some notable “hiccups” here and there (for example the dot-com bubble). One thing that is always difficult is to identify those companies that will be part of the winning side of the macrotrend. By this I don’t mean solely that will survive the inevitable market turmoil, but also that they will perform better than the sector average. A simple solution to this problem has always been to find a good investment fund whose managers could potentially achieve better risk-adjusted returns than their benchmark.

Overview of STK’s strategy

Columbia Seligman Premium Technology Growth Fund (NYSE:STK) promises to do just that. In STK’s own words they “Target long-term capital appreciation and current income with a portfolio of technology stocks and an option overlay strategy designed to mitigate downside volatility and generate income”. Basically, their approach incorporates an option overlay strategy to manage downside volatility and generate additional income. The benefits include a focused portfolio constructed through a rules-based strategy, striving for consistent performance while reducing risk. Investments are chosen through thorough bottom-up fundamental and valuation analyses, utilizing a growth-at-a-reasonable-price (GARP) style for more stable performance compared to peers.

Recent performance

STK’s strategy is definitively interesting for many investors as it allows to be part of the significant growth we are seeing in the technological sector while still enjoying a pretty good quarterly dividend. In fact, according to the Fund’s 2023 annual report they distributed $2.1013 per share in 2023: four quarterly dividends of $0.4586 plus an additional December dividend of $0.2669. This means that if you’d bought a share of the Fund on January 3rd 2023 at opening $23.36 you would have seen a dividend yield of almost 9%. With a price appreciation of almost 37.29%, given that the market price of one share reached $32.07 by the end of 2023, an investor would have seen a roughly 46% return in one year. To this, we should remove the 1.13% annual fund expenses.

At first glance this seems like a rewarding strategy and return, but of course we should see how it stands against the benchmark and its competition. The Fund identifies the S&P North American Technology Sector Index as their benchmark, and unfortunately they indeed underperformed compared to it in 2023, with the index returning 61.13%. We’ll see more on why this was the case in the following sections.

Holdings and impact on performance

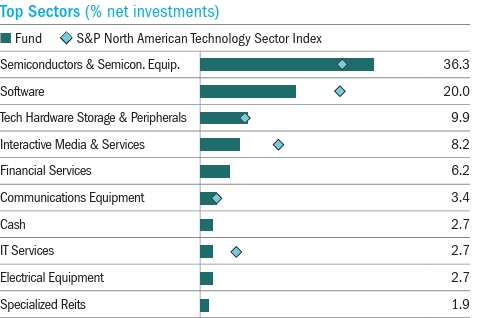

STK is a relatively highly concentrated Fund, with its roughly $428 million net assets as of March 2024 invested in just 62 companies. Furthermore, as seen below, the top 10 holdings constitute about 41% of the total investments. It’s not surprising that the Fund managers describe their portfolio as “conviction-weighted”. Furthermore, we see in the table the comparison with the index and it becomes clearer how the strategy is leaning on a generally higher concentration on fewer stocks. For reference, the index mentioned is composed of 279 different constituents. The second picture shows the top sector percentage of the portfolio compared to the index.

STK Top Holdings (Columbia Threadneedle – Columbia Seligman Premium Technology Growth Fund)

STK Top Sector Investments (Factsheet: Columbia Seligman Premium Technology Growth Fund )

Looking at the top holdings and sectors, at the complete list, and what the Fund managers state in their annual report, we can get a first idea of why the Fund underperformed the index in the past year. In fact, some stocks noticeably dragged down the fund’s performance. Some holdings in the industrials sector and a lack of exposure to healthcare had a negative impact on overall performance. Furthermore, the fund’s choices in the semiconductor industry resulted in underperformance compared to the benchmark. Additionally, maintaining a lower-than-average position in the communication services sector, along with specific stock picks, further affected the fund’s relative performance. Companies such as Bloom Energy Corp. (BE), Fidelity National Information Services, Inc. (FIS), and Thoughtworks Holding, Inc. (TWKS) were detrimental to absolute returns, with the latter no longer part of the portfolio. Finally, the extremely strong performance of NVIDIA Corp. (NVDA) and Meta Platforms, Inc. (META) and their underrepresentation in the Fund compared to the index only exacerbated the Fund’s relative underperformance during the year.

On the positive side, some stocks and sectors were able to reduce the negative effect of the choices made above. For instance, absolute positive performance was significantly boosted by investments in the semiconductors, software, and technology hardware sectors within the information technology industry. Holdings in the communication services sector, particularly in interactive media, also lifted absolute returns. In comparison to the benchmark, positive contributions stemmed from choices in communications equipment and technology hardware. For example, stocks such as Lam Research Corp. (LRCX), Broadcom Inc. (AVGO) proved good selections in driving absolute performance since they have experienced strong performance and they were greatly overweighted compared to the index. Finally, although Apple, Inc. (AAPL) has had a good performance in 2023 it was still lower than the overall performance of the Fund and of the index, therefore the underweight of this was positive.

Is it a good time to buy?

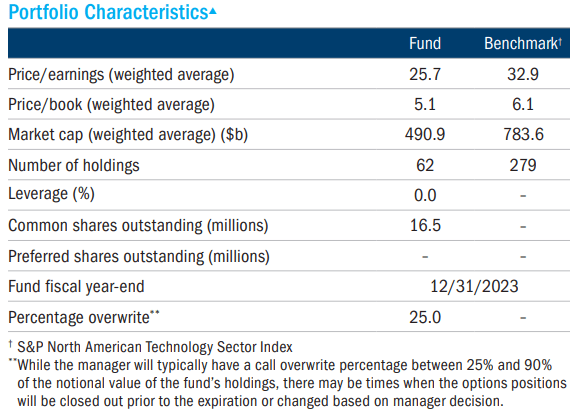

As with most technology stocks there is always a big question mark on when it is the right moment to buy some stocks. Funds or ETFs that invest in the technology sector are no different. In fact, most of the times technology stocks tend to be overvalued (metrics-wise) compared to rest of the market. However, we see in the picture below that as of end of last year the P/E and P/B ratios of the Fund compared to the index were quite lower, showing that perhaps the selection of the Fund is undervalued compared to its sector. If this is the case, we would expect the selected stocks to appreciate more relative to the index and perhaps lead to higher returns, contrary to what happened in the past year.

STK Portfolio Characteristics vs Index (Factsheet: Columbia Seligman Premium Technology Growth Fund )

To me, when dealing with Funds and ETFs there is not really a “best moment” to invest as these instruments tend to be relatively diversified and, short of a big crisis that makes prices plummet, they shouldn’t experience extreme movements. Therefore, I believe that if we align with the approach and strategy of the Fund the best strategy is to do a dollar-cost-averaging strategy and distribute acquisition of shares in time.

Risks toward investing

Funds such as STK that rely on the stock-picking abilities of the fund managers can present several risks, particularly concerning the technology industry in which this Fund invests in. On one side, STK offers relatively diversified access to a relatively fresh market, where it’s challenging for many to pinpoint the companies poised to lead in these major trends. Furthermore, having an experienced team with a demonstrated background in choosing high-performing stocks in this space can bring a great value for investors that lack the time and expertise to do so on their own.

Conversely, compared to a traditional passive ETF the stock-picking entails the risk of missing on stocks that have unpredicted boosts in growth (such as Nvidia or Meta in STK’s case) leading to a risk of underperforming the index. This risk is particularly high for funds with active management as the higher annual expenses do play a role in long-term returns for investors. Finally, if an investor chooses to place money into this Fund as they have confidence in the Fund manager’s ability, there is also the long-term risk of the manager leaving the fund and the ability of the following manager not being at the same level.

Conclusions

Investing in a fund such as STK should not be only about the replication of the benchmark index, the S&P North American Technology Sector Index. In fact, the Fund provides additional perks such as regular quarterly dividends that as of today’s prices (roughly $32/share as of March 25, 2024) represent a 5.78% dividend yield. The Fund is able to return these dividends to investors thanks to their option-writing strategy which allows them to collect premiums of their holdings, as technology companies are not usually the best for dividend-seeking investors.

However, as the picture below shows, the returns provided by STK are not able to match those of the benchmark, and the difference has only increased in the past year. While the graph below doesn’t include dividends for STH, even if we included them the returns would still be lower.

Return comparison STK vs Index (Google Finance)

So should you invest in STK? I think that the investment is sound if you:

- Want to be exposed to the technology sector and its promise for higher-than-average growth,

- Want a diversified investment portfolio but not as diversified as a traditional index-replicating ETF, with the hopes of some of the picked stocks to overperform,

- Are interested in having a regular dividend for some quarterly cash flows, whether you decide to reinvest them into the Fund itself or elsewhere. This point is especially important for me, as it is what would make this Fund an interesting addition to my portfolio.

However, I think that there might be better options and I would therefore not recommend buying stock of STK. To me, the dividends to not justify the returns that are so much lower than those of the index.

{kind=link}