FatCamera

Introduction

As you guys probably know, I like dividend growth investing. With dividend growth investing, you can compound your wealth in a sustainable way and if you invest in dividend growth stocks, the chances are high that you have exposure to high-quality and resilient companies.

The composition of a dividend growth portfolio depends heavily on your time horizon, but if you have a lot of time on your side, it is a good idea to also buy some companies with high dividend growth rates.

This brought my attention to Zoetis Inc. (NYSE:ZTS). The company is operating in the animal healthcare sector, which has an anti-cyclical character. Despite the fact that the share price of ZTS is almost the same compared to H2 2021, it still has outperformed the S&P 500 index on a 5Y basis.

5Y total return (YCharts)

The dividend yield of ZTS is only 0.79%, but with a 5Y CAGR of 23.5% the dividend growth is really impressive.

Today, I want to analyze the company to see if the stock is a buy at current prices.

Company overview

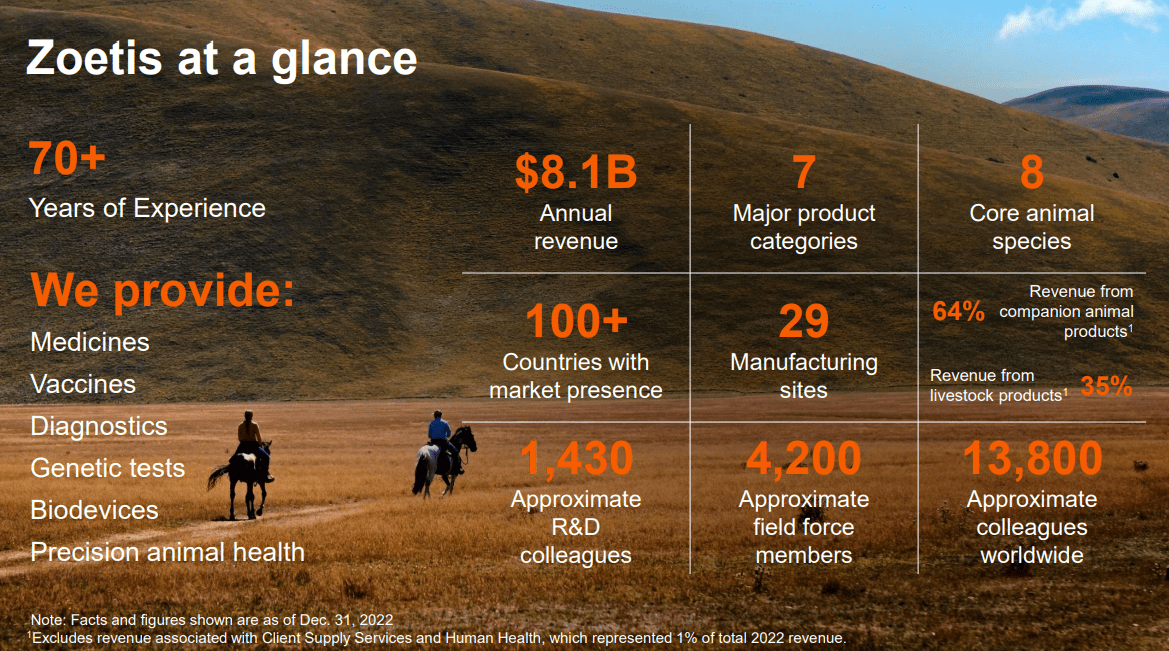

ZTS was founded in 1952 and is headquartered in Parsippany, New Jersey. The company is a world leader in animal health and has a market cap of $90.3 billion.

What is interesting to know is that ZTS is actually a spin-off from Pfizer Inc. (PFE) and since then (2013) it operates as an independent animal health company.

ZTS has a broad product portfolio when it comes to detection, treatment and prevention of animal disease such as: medicines, vaccines and diagnostics.

ZTS company overview (investor overview 2023)

ZTS is serving a lot of customers worldwide, but the US is by far their biggest market with 54% of total revenue.

Revenue distribution (investor overview 2023)

Looking further into more specific data, companion animals are 65% of total revenue. The company also offers a variety of livestock products, which prevents or treat diseases and enables sustainable production of animal protein.

Despite the size of its product portfolio, some products are heavyweights in terms of total revenue and they are particularly dominant in parasiticides and dermatology medications in cats and dogs. Their best selling products, Simparica/Simparica Trio and Apoquel, contribute 13% and 10% of their revenue. If we add Cytopoint, Revolution/revolution, Plus/stronghold and their Ceftiofur product line, it comes down to a total revenue of 37%. These numbers are based on ZTS’s 2023 annual report.

Catalysts

So, what are the potential catalysts for ZTS to keep on growing? Let’s begin with the overall growth prospects of the animal health sector.

Research shows that the global animal health market will grow at a CAGR of 9% until 2030. The US market will grow at a CAGR of 8% annually.

Animal health market prospects (grandviewresearch.com)

This study provides several explanations to justify this possible growth.

- Rising pet ownership, especially COVID-19 has led to an increase in pet adoption, so more animal healthcare is needed.

- Increase of animal health expense.

- Rising prevalence of animal diseases.

- Pet humanization: Nowadays, pets are seen as family members and people are often willing to keep their pets in good condition. Even with a 20% decrease in total budget, households won’t spend less when it comes to their pets.

- Growing population worldwide: This will increase the demand for food, for example, meat, milk and eggs. This should lead to a growing “production animal” segment.

In addition to this, the animal health market is still fragmented and market share is held by a lot of different companies. Despite the fact that ZTS is already one of the larger businesses, there is still a lot to win. ZTS can certainly be called a winner in the long-term, as it continues to show higher growth compared to the market average.

ZTS market outperformance (investor overview 2023)

As shown in the picture below, ZTS has a strong presence in its key markets and if the company keeps innovating, there are a lot of options to further expand their business. ZTS sees itself as the R&D leader in its sector and has sufficient financial strength to innovate and to maintain its leading position.

ZTS market leadership (investor overview 2023)

Librela

One of the fast-growing products of ZTS is called Librela. This product is used on a monthly basis to control pain caused by osteoarthritis in dogs. Osteoarthritis is a common condition and the prevalence in North America is reported at 20% of all dogs over 1 year of age based on data collected from 200 veterinarians. At the moment, Librela is the most sold product in Europe when it comes to osteoarthritis pain and in October 2023, the product was officially launched in the US. My brother-in-law is a vet and he is seeing great results after using Librela. Although many consider it an expensive medicine, people are often willing to do anything for the well-being of their animal. Librela’s margins are also higher than the company’s average and could have a nice leverage on profitability when successfully rolled out. The success of this product should emerge in FY 2024.

Financials

So, how is the company performing over the last 10 years? Looking at revenue, the company has managed to grow it from $4.7 to $8.5 billion which implies a 10Y CAGR of 5.9%. From a net income point of view, things are looking much better with a CAGR of 14.8%. Over the years, ZTS has managed to increase its gross- and profit margin significantly in the long term and therefore outperform their peers.

ZTS profitability (Seeking Alpha)

Things are getting even better if we look at EPS and FCF per share which grew at a 10Y CAGR of 15.9% and 15.3% respectively. Based on these numbers, we can confirm that ZTS is a great compounder. What is good to mention is that the FCF per share is not growing that rapid from a 5Y time frame, but this is mainly due to significantly higher CapEx.

EPS and FCF per share development (YCharts)

Let’s look at some return ratios as well. ZTS is well able to use the money of its owners to generate bottom-line profit.

ZTS return ratios (YCharts)

Balance sheet

The balance sheet looks solid, and with a net debt-to-EBITDA of 1.3 it looks like the company is well able to handle its debt.

ZTS debt development (YCharts)

It is clear that the debt has increased over time, but not in a way to start worrying. There are also no significant short-term debt maturities that could not be met.

Outstanding debt securities (ZTS 2022 annual report)

With an interest coverage ratio of 12.8 ZTS has currently no problems with paying their interest.

The company also enjoys a credit rating of BBB from S&P and a Baa1 rating from Moody’s, which means they have a reasonable capacity to meet their financial obligations.

Dividend

The company is committed to grow their dividend at or faster than their adjusted net income. In this article, the dividend metrics will be reviewed via the dividend grades from the Seeking Alpha website.

Dividend grades (Seeking Alpha)

Yield and growth

ZTS’s TTM dividend yield is 0.79% and the FWD dividend yield is currently 0.88% and isn’t that impressive. Although from a 5Y perspective, it is at a relatively high level.

Dividend yield development (Seeking Alpha)

When we talk about dividend growth, it is a completely different story. The company scores an A+, with a 10Y CAGR of 19.2% and an even more impressive 5Y CAGR of 23.5%.

ZTS dividend growth (Seeking Alpha)

Personally, I like to use the Chowder Rule as a quick screener to evaluate dividend yield and growth. In this case, the dividend yield is less than 3%, which means that the 5 year CAGR plus the dividend yield must be greater than 15%. If we do the math, ZTS’s Chowder score is 24.3 because of its high dividend growth. However, I think the 23.5% isn’t sustainable and their future growth will be more in line with their latest dividend hike of 15%. In that case, the score would still be high enough to meet the Chowder criteria. Personally, I wouldn’t be surprised if ZTS can continue to increase its dividend by double digits beyond 2030.

Safety and consistency

The dividend is nicely covered with a payout ratio of 29.5%; however, the payout ratio is also getting higher over time.

dividend safety (YCharts)

What is standing out is that the cash payout ratio is currently 42.69%. This metric strengthens the case that they can’t keep up the dividend growth pace from the last 5 years.

Since 2013, they are increasing their dividend, so they have a dividend growth streak of 11 years. Given ZTS’s favorable long-term growth prospects, market position and dividend growth policy, I expect the company to eventually join the list of dividend aristocrats.

Latest quarterly results

ZTS’s share price dropped about 4% when they released earnings. What is good to see is that they keep outperforming the industry with 8% operational revenue growth.

Q4 2023 vs Q4 2022 results (ZTS Q4 2023 presentation)

The companion animal segment is still their greatest growth driver and their livestock segment has started growing again.

Looking at the revenue by product, it is clear that the more important products in their portfolio experiencing rapid growth. Simparica Trio grew 22% in Q4 2023 compared to Q4 2022, mainly due to price increases. Despite inventory headwinds in the first quarter and aggressive promotions from competitors, they still managed to grow their operational revenue from Simparica Trio 9% in FY 2023.

On of the other highlights is the performance of Librela. The roll out in the US going better than expected and Librela has achieved an operational revenue growth of 93% in Q4 2023 compared to Q4 2022.

Product revenue numbers (ZTS Q4 2023 presentation)

What is also striking are the disappointing results in China (-28% operational revenue Q4 2023 vs Q4 2022). Despite China only accounting for 5% of total revenue, the weakness in the economy has a meaningful impact on the numbers.

2024 outlook

I think that the decline in the share price after earnings has to do with the outlook.

Outlook FY 2024 (ZTS Q4 2023 presentation)

In FY 2024 they expect an operational revenue growth of 7-9% and adjusted net income growth of 9%-11%, so they assume they will continue to outperform the market. The companion animal segment is still the key growth driver for the company and the growth of livestock is expected to be in line with its industry. As I said, the roll out of Librela in the US seems to be more successful than expected and this should also result in impressive growth numbers in FY 2024. When it comes to Simparica Trio and their dermatology portfolio, high single-digit growth is taken into account. Since the economic situation is China is still bad, the company still expects headwinds when it comes to growth in FY 2024.

All in all, we can conclude that ZTS is growing nicely and it is likely that they continue to do so in the future. But is it enough to justify its stock price?

Valuation

ZTS is a wonderful company to have in your portfolio for the long term. But even with high-quality companies, it is certainly possible to overpay.

ZTS has a “F” valuation grade on the Seeking Alpha website, which means it is richly valued. Also the PEG ratio of 3 is indicating that the stock is currently overvalued.

Valuation grades (Seeking Alpha)

To calculate the fair value of ZTS, discounted cash flow analysis has been used. I used a FCF of $1.621 billion. As most people know, FCF can vary a lot over time and it has also been significantly influenced in recent years by the increase in CapEx to support future growth. However, I do expect that the FCF per share will follow the trend of EPS growth in the long term.

FCF and CapEx (YCharts)

As I said earlier in the article, the 10Y FCF per share of the company has grew with a CAGR of 15.3%.

FCF per share development (Seeking Alpha)

For the analysis, I used a 5-year growth rate of 12%, and for the 5 years thereafter 10% because it’s harder to make accurate assumptions over longer periods of time.

ZTS is trading at a P/E GAAP of 38.90, which is below its own 5Y average of 42.04. Due to its market leading position, profitability metrics and future growth prospects, it can be justified that ZTS is traded at a premium valuation. However, I think that a P/E of 39 is just too much.

For the analysis, I used a terminal multiple of 30. I applied a discount rate of 10%, because I want this as a minimal annual return on investment.

If we do the math, it comes down to a fair value of $154.28 per share, which means shares of ZTS are currently overvalued.

Discounted cash flow analysis (google spreadsheets)

Conclusion

ZTS is definitely a stock to hold for the long-term and investing in this company is investing in quality. The global animal health market is still growing high-single digits and ZTS is clearly going to take advantage of it. The market is still fragmented, this gives ZTS the opportunity to grow further due to their ability to do high R&D expenditure.

For (young) dividend growth investors, there is also a lot to like. At the moment, the dividend yield is low, but if you are investing for decades to come, the yield can grow into something beautiful.

In fact, everything seems good about the company, except its valuation. Based on the various valuation metrics on the Seeking Alpha website and the results of the discounted cash flow analysis, ZTS appears to be overvalued. With the current share price of $197.29 I think it is not worth it to buy ZTS right now. I think the risk for investing at current prices is too high for the potential reward.

I therefore see the high valuation as one of the biggest investment risks. There is also a lot of competition within the animal health sector, which means ZTS could always lose market share to competitors. If this is about important products in their portfolio, such as Simparica Trio or one of their other top-5 selling products, the company can be seriously hit.

I encourage you to add ZTS to your watch-list, so if the share price falls and there are no major changes fundamentally, this can create great opportunities to build a position with dollar-cost averaging.

With all this in mind, I give ZTS a “HOLD” rating.

{kind=link}