Anatoli Igolkin/iStock via Getty Images

Synopsis

American Woodmark (NASDAQ:AMWD) is one of the largest cabinet manufacturers in the US. It sells products to the remodeling and new construction markets through home centers, builders, independent dealers, and distributors. AMWD’s historical financial results have shown strong revenue growth, while margins have recovered in 2023 after a drop in 2022. However, in its latest 3Q24 earnings results, revenue took a hit due to challenging macro-economic conditions. On the flip side, due to years of underbuilding, the median age of US homes is gradually increasing, therefore creating opportunities for remodeling in the long run. In my relative valuation, my target price indicates mid-single-digit upside potential. Combining this with the challenging macro-economic trends, I am recommending a hold rating for AMWD.

Historical Financial Analysis

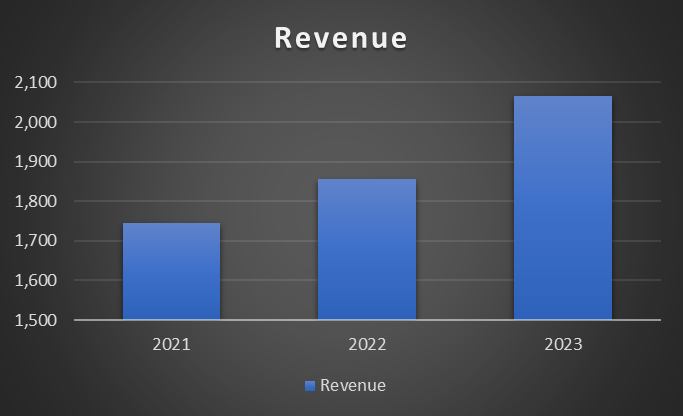

Over the last three years, AMWD’s revenue has been growing annually. In 2021, it reported total revenue of $1.74 billion. In 2022, revenue year-over-year growth was 6.5% due to strong growth in all three customer segments [Home Center, Builders, Independent Dealers and Distributors]. By 2023, it had grown to $2.06 billion, which represents a year-over-year growth of 11.3%. This growth was driven by strong growth in its builder and dealer distributor channels due to price increase.

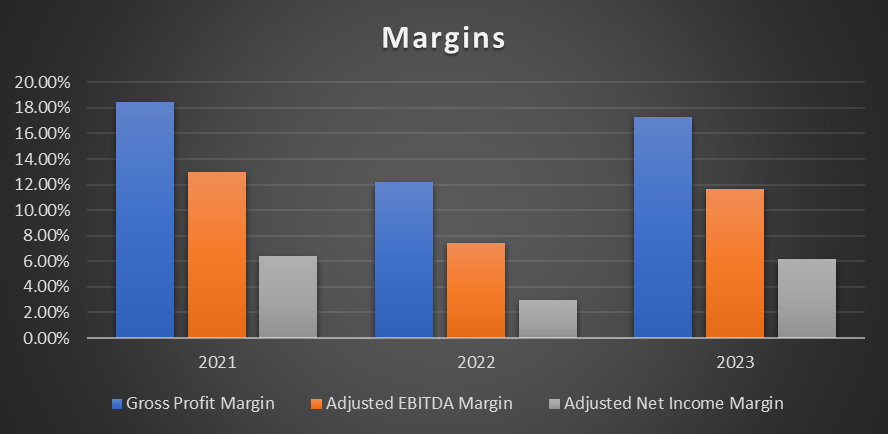

On profitability margins, there has been some volatility. In 2021, the gross profit margin was 18.47%, the adjusted EBITDA margin was 13%, and the adjusted net income margin was 6.39%. In 2022, all three margins took a hit. Gross profit margins fell to 12.2% due to higher inflation, which affected material, logistics, and wage costs. As a result, it impacted its adjusted EBITDA margin and adjusted net income margin, which decreased to 7.4% and 2.95%, respectively.

However, in 2023, all three margins recovered. Gross profit margin increased to 17.3%, driven by price increases and improvements to manufacturing efficiency. The improvement in gross profit margin positively impacted both its adjusted EBITDA margin and its adjusted net income margin. Adjusted EBITDA margin increased to 11.63%, while adjusted net income margin grew to 6.15%.

Author’s Chart Author’s Chart

3Q24 Earnings Analysis

For 3Q24, AMWD reported net sales of ~$422 million, which was down 12.2% year-over-year. The decrease was due to weakness in both its new construction and remodeling segments. New construction’s revenue fell 11% year-over-year, while remodeling decreased 13.1%. Overall, demand was weak due to lower in-store foot traffic and a shifting trend towards smaller projects.

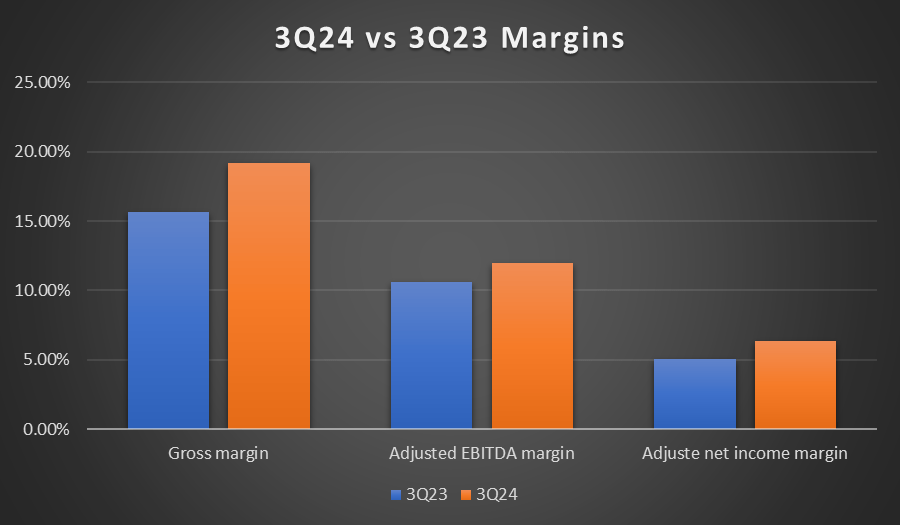

Moving down the P&L, the gross profit margin expanded from 15.7% to 19.2%. This gross margin expansion was driven by favorable product mix, pricing increase to offset inflationary impact, and supply chain stabilization. Its adjusted EBITDA margin expanded from the previous period’s 10.6% to 12.0%. Adjusted EPS [per diluted share] grew from $1.46 to $1.66. These adjusted margins improvements were driven by favorable product mix and increased operational efficiencies in its manufacturing facilities.

Author’s Chart

Unfavorable Macro-Economic Trend

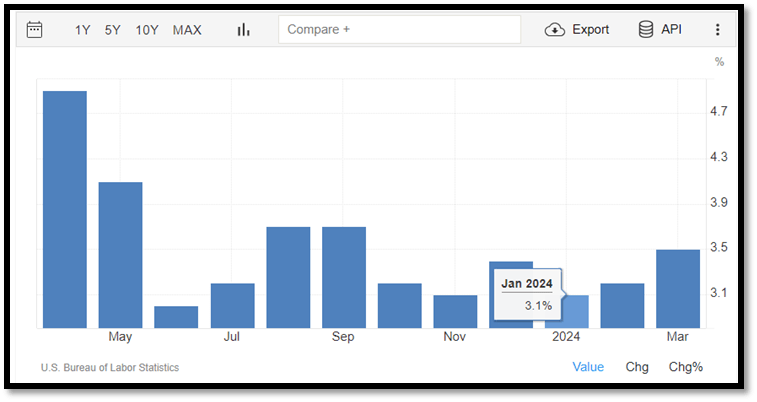

In 2024, AMWD was impacted by several challenging macro-economic trends. Firstly, the reported inflation for January 2024 was 3.1%. Although it was lower than the previous period’s 6.4%, the inflation rate is still above the Fed’s target rate of 2%. As of March 2024, inflation had increased to 3.5%, and these factors cast shadows on the timing of the Fed’s rate cuts. As inflation remains persistent, it has an impact on consumers’ discretionary spending, and this situation will have an impact on AMWD’s business.

Trading Economics

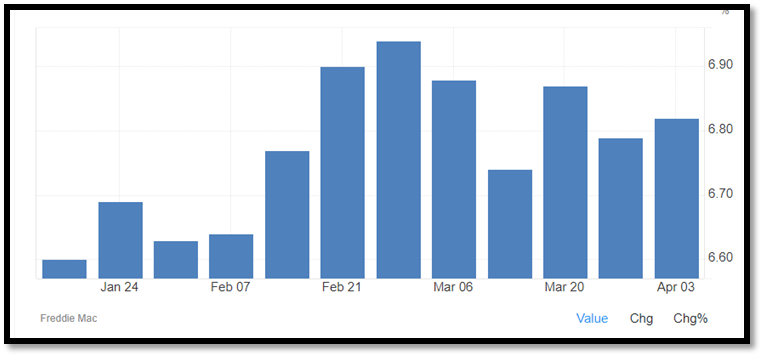

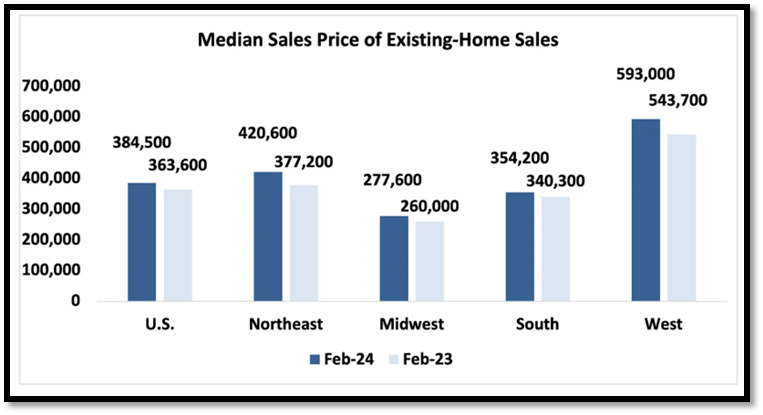

Apart from high inflation, the US 30-year mortgage rate has been steadily rising over the months since the start of 2024. On 31 January 2024, the rate was 6.63%, but by 03 April 2024, it had increased to 6.82%. Additionally, the median sales price of existing homes for February 2024 increased 5.7% year-over-year to $384,500. All these factors combine to contribute to the demand weakness AMWD faced in the first nine months of 2024. In 1Q24, net sales fell 8.2%, 2Q24 decreased even more at 15.6% while 3Q24 reported a decline of 12.2%. On a nine-month basis, net sales fell 12% year-over-year.

Trading Economics National Association of Realtors

Aging US Housing Age Creating Opportunities

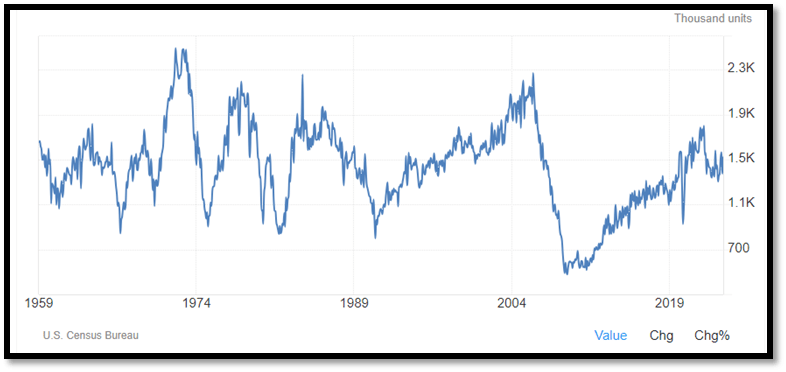

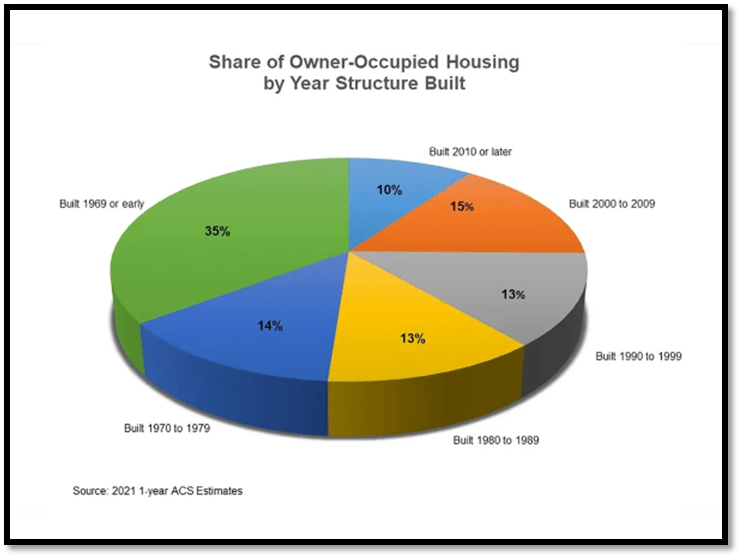

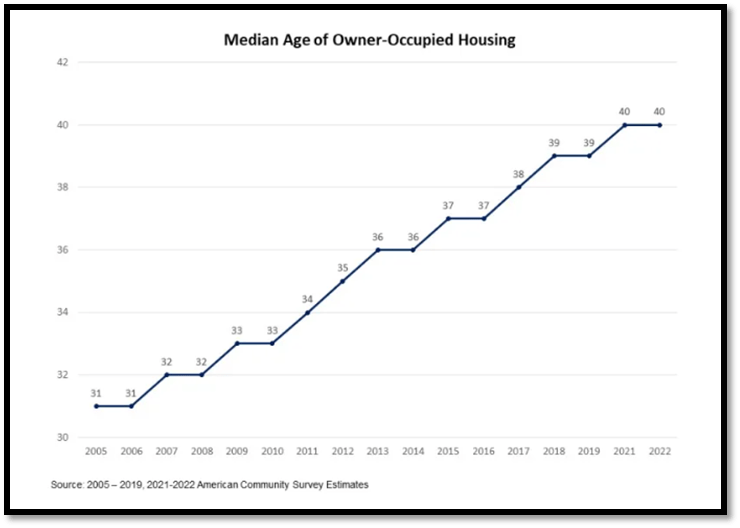

The first chart shows that the annual US housing starts have yet to recover to their historical levels since 2009, and it also highlights ~15 years of underbuilding. As a result, homes built in 2010 and later account for only 10% of total housing, while those built before 1969 account for 35%. Since 2005, the median age of US housing has been steadily increasing, reaching 40 years old in 2022.

As the median age of US houses increases, it also increases the need for maintenance and improvement. Therefore, this situation presents an opportunity for AMWD as it sells its products to the remodeling markets in the US. The increasing need for remodeling will lead to higher market demand, thus creating tailwind for AMWD and bolstering its long-term growth outlook.

Trading Economics National Association of Home Builders National Association of Home Builders

Relative Valuation

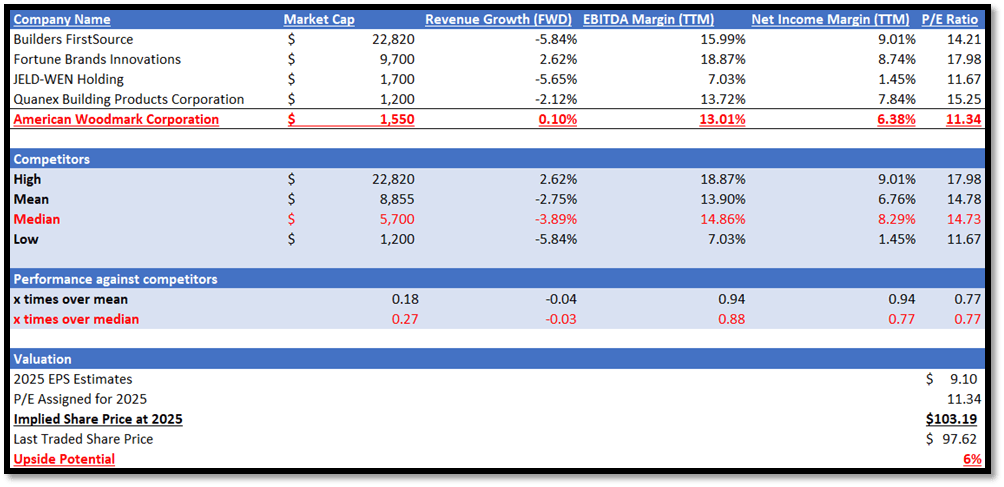

AMWD operates in the building products industry, and the competitors listed in my model also operate in the same industry. I will compare them in terms of forward growth outlook and profitability margins.

Firstly, in terms of forward growth outlook, AMWD performs better than its peers, as it has a forward revenue growth rate of 0.10% vs. peers’ median of -3.89%. Despite its outperformance, its forward revenue growth rate is modest due to the challenging macroeconomic trends that I have discussed above.

Moving onto profitability margins, AMWD underperformed its peers in both EBITDA margin TTM and net income margin TTM. AMWD’s EBITDA margin TTM was 13.01%, lower than peers’ median of 14.86%. In terms of net income margin TTM, AMWD reported 6.38%, while its peers’ median is higher at 8.29%.

Currently, AMWD’s forward P/E ratio of 11.34x is lower than peers’ median of 14.73x. Given its disappointing 3Q24 earnings results, headwinds from challenging macroeconomic trends, weak forward growth outlook, and underperforming profitability margins, I argue that it is fair that AMWD is trading at a lower P/E. In addition, AMWD’s current P/E ratio is trading around its 5-year average.

The market’s 2024 revenue estimate for AMWD is ~$1.84 billion, while the 2025 revenue estimate is ~$1.86 billion. 2024’s EPS estimates is ~$8.60, while 2025’s EPS is $9.10. Given the factors discussed together with management’s revenue guidance of low double-digit decline for 2024, these estimates are reasonable as they echo similar sentiments. By applying 11.34x to its 2025 EPS estimates, my 2025 target price is ~$103.19, which represents a modest mid-single-digit upside potential of 6%.

Author’s Valuation Model

Risk

The upside risk to my hold recommendation is related to the direction of inflation. If inflation were to start cooling, it would trigger a series of events. The Fed will begin to cut rates, which will have an impact on the mortgage rate. As a result, it might bolster demand for AMWD as discretionary spending increases. In addition, the aging US homes combined with lower inflation will also create a tailwind for more businesses.

Conclusion

Over the past three years, AMWD has demonstrated strong revenue growth. Even though margins fell in 2022, they recovered in 2023, almost on par with 2021’s level. However, in 3Q24, revenue fell double digits year-over-year, and it was attributed to challenging macro-economic trends such as high inflation. On a brighter note, 3Q24’s margins improved year-over-year, driven by favorable product mix and increased operational efficiencies. Since 2009, US housing starts have been below historical levels, leading to years of underbuilding. As a result, the median age of US homes has reached 40 years, which is creating opportunities for remodeling as these old houses may need more repairs and upgrades. Moving onto my relative valuation, my target price indicates mid-single-digit upside potential. Given the challenges AMWD faced in 2024, the risk and reward ratios are not attractive. Therefore, I am recommending a hold rating for AMWD.

{kind=link}