Guinness’ Will James reflects on the impact of volatility on the European equity market and why quality stocks ensure long-term resilience.

As geopolitical tensions have accelerated on both sides of the continent – largely since Russia invaded Ukraine in February 2022 – Europe has been under increasing pressure to invest in its own defence and national security.

In 2024, member states’ expenditure reached €343bn and was forecast to spend a further €381bn in 2025.

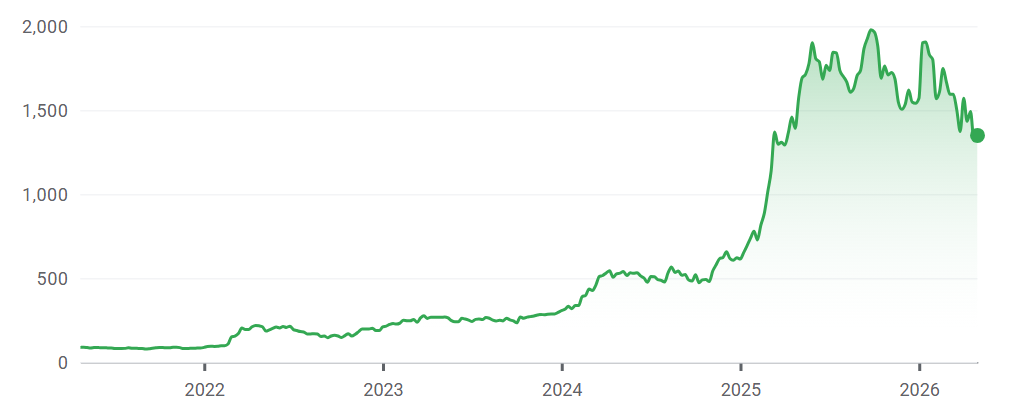

For many European fund managers, this flow of capital presented opportunity, with notable European defence stocks rocketing. For example, shares in Rheinmetall have surged since 2022.

Rheinmetall stock price performance since 2022

Source: Google Finance

However, not every European fund manager is looking to invest in the sector. Will James, manager of the Guinness European Equity Income fund, argued that defence stocks don’t meet his quality threshold.

“When looking for quality, we apply a 6% cost of capital screen across our universe and the minimum threshold for a company to be included is an 8% cashflow return on investment in each of the past eight years,” he said.

James said European defence businesses have not demonstrated an ability to generate high recurring returns on investment in a sustainable way.

“They are also beholden to things outside of their control,” he said. “One is government defence spending – that’s going up, fine – but the second factor is whether governments can spend the money as quickly as the market wants them to.”

Defence isn’t the only sector that doesn’t meet the fund’s cost of capital quality screen, as the portfolio also has no exposure to oil and gas, utilities, materials or telecom companies.

He said the Guinness strategy is instead focused on businesses that are less driven by macro narratives and can weather uncertainty.

Below, James sets out how the fund’s strict quality discipline has driven portfolio construction – including which stock calls have worked, and which have not.

What does the fund aim to do?

The fund looks to identify businesses that are in a strong position to generate organic cashflow, reinvest it in business growth and ultimately sustain and pay attractive dividends.

We are the most interested in the underlying quality of the business and the quality that supports the dividend flow, versus starting with a dividend and working backwards – so this fund doesn’t screen on yield.

We are focused and concentrated with 30 equal-weighted stocks, as we want a portfolio that reflects our highest-conviction ideas. The starting position for any holding in the portfolio is 3.3%. We will rebalance as things progress, but we don’t rebalance systematically.

What we don’t want is a portfolio that is determined by its top 10 holdings from a short‑term performance perspective. Instead, we want each exposure to play a role in delivering what we believe will be an attractive risk-adjusted total return over time.

The fund is never going to be the highest‑yielding fund out there. We look at it more through a total return prism than a yield‑at‑any‑price type approach.

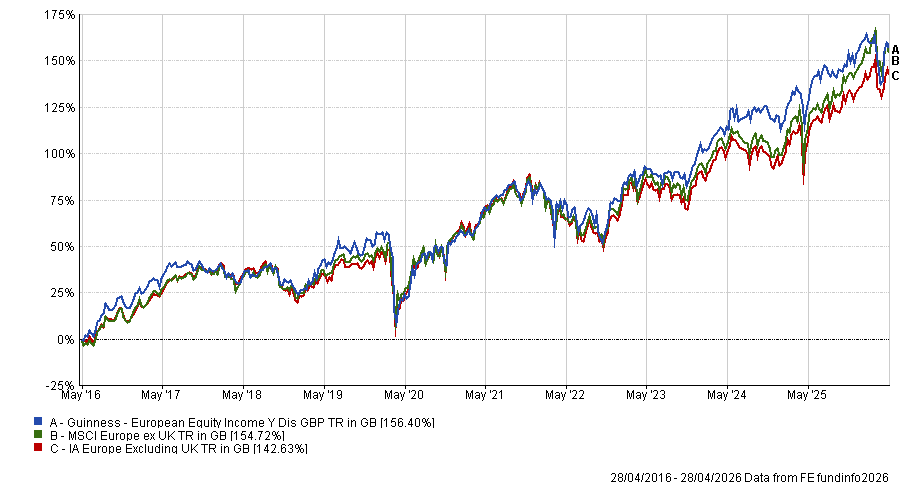

Performance of the fund vs sector and benchmark over 10yrs

Source: FE Analytics

With geopolitical uncertainty distorting markets, what are you seeing from a bottom-up perspective?

From a bottom‑up perspective, value, as defined by low price‑to‑book or high dividend yield, has done extremely well, and I understand why. But what’s more interesting now is that high‑quality, cash‑generative businesses are trading more cheaply than lower‑quality, asset‑backed businesses.

Last year, the market wanted EU domestic companies that were immune to dollar weakness and tariffs. This year it’s been similar – the market is backing last year’s winners because it doesn’t really know what else to do.

We think the opportunity now lies with businesses that are better diversified, because they are in a stronger position to weather uncertainty.

What are some of the best calls you have made in the past 12 to 18 months?

EssilorLuxottica was bought in early 2023 and we enjoyed strong performance, with shares up around 25% since purchase as the market started to price in the advent of Meta smart glass (Essilux provides the hardware).

However, by September 2025 we became concerned by the aggressive re-rating the shares had enjoyed, so we exited the position. Shares have fallen 30% since then.

BE Semiconductor was bought in April 2026 around the Liberation Day sell-off. It has contributed just under 2% to the total return of the strategy since purchase on evidence that end market demand for its leading-edge advanced packaging equipment is picking up markedly.

And some of your worst calls?

The danger as a quality investor is when a good quality company becomes less good quality – the market often recognises that before you do. A recent example has been Novo Nordisk.

We have owned Novo Nordisk since 2016 and consistently took profits over time. The mistake was not exiting in December 2024 or January 2025.

At the time, we debated selling Novo and didn’t. The valuation had halved, the dividend had doubled, but the quality still looked attractive.

When the company issued much more cautious guidance than expected earlier this year, the market reaction in February was more aggressive than anticipated.

Given the string of disappointments over the past 12 months, it was a detractor to performance to the tune of 1.5%.

That is one where we would say we got it wrong, and the position remains under review – but the positive side of our equal‑weighted approach is that exposures never become too large.

Looking ahead, how do you seeing geopolitical uncertainty shaping European equity markets over the course of 2026?

From a top‑down perspective, [US president] Donald Trump’s tariff announcement meant Europe had a tough year last year – but it also focused minds going into 2026.

Europe realised it couldn’t rely on the US for defence, couldn’t rely on Russia for cheap energy and couldn’t rely on China for growth. Europe has to focus inward.

The problem with the US-Israel conflict with Iran is that it has further highlighted the ongoing fragility of Europe.

The risk in the interim is a broader recession. One hopes Trump realises he doesn’t want a recession and pulls the levers accordingly.

Although we are bottom‑up investors and believe our underlying businesses are well placed to navigate headwinds, there is no escaping the fact that Trump has once again introduced uncertainty. What that ultimately means for global demand and consumer confidence remains unclear.

So I think there’s a structural positive case for Europe, counterbalanced by a cyclical question mark.

What do you do outside of fund management?

I enjoy making things. I spend a lot of time in the garden and, during Covid, I built a treehouse.