We Are

By John Baldi, Michael Clarfeld, CFA, & Peter Vanderlee, CFA

All Eyes on AI Leaves Much Overlooked

Market Overview

The first quarter provided a terrific start to the year for the S&P 500 Index (SP500, SPX) and the ClearBridge Dividend Strategy (MUTF:SOPAX). The S&P 500 rose 10.56% and the Strategy was up about 70% as much. This relative performance is consistent with our expectations. With our dividend focus and conservative approach, we tend to lag in momentum-led markets like the current one. Conversely, we tend to outperform in sharply declining markets. Recall 2022; the market sunk 18% while we were down less than half as much.

The market’s rise continues to be led by a small handful of mega cap technology names. Nvidia (NVDA) stands out; the chipmaker rose over 80% percent in the quarter and was responsible for nearly a quarter of the entire index’s increase. At almost 30% of the total index, information technology (IT) is now 2.25x the size of any other sector, near historical peaks, and that’s not counting Alphabet (GOOG), Amazon (AMZN) and Meta (META). Reclassify these three as IT companies, and the sector sums to almost 40% of the total market! At the individual stock level, the top five companies represent 25% of the overall market – the highest level in decades.

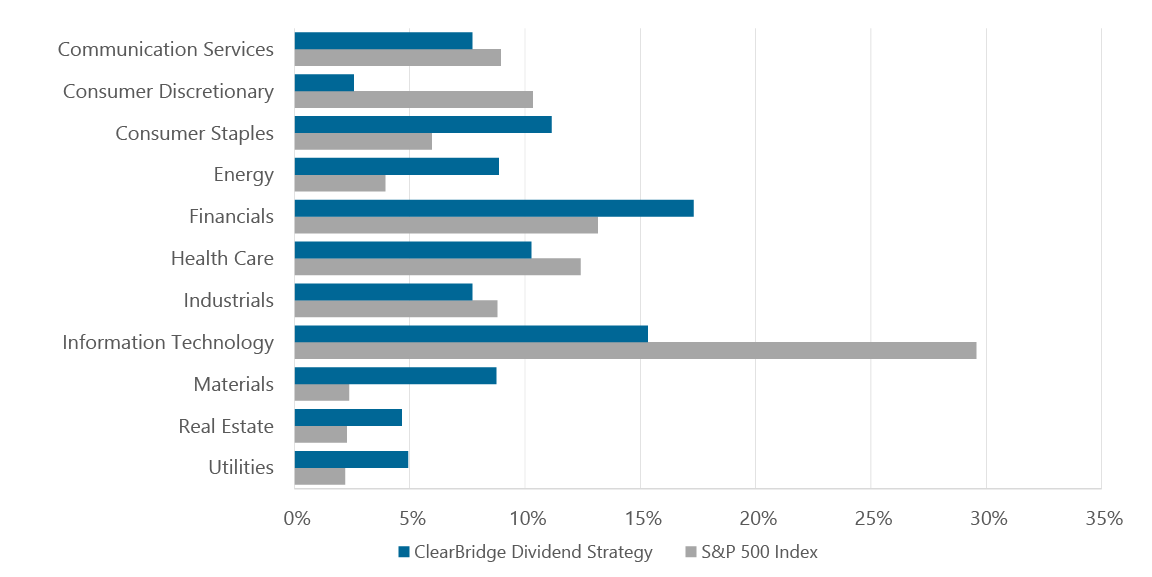

While the broad market has become increasingly concentrated in and correlated to these technology leaders, we remain steadfastly committed to broad exposure across sectors (Exhibit 1). Overemphasis on technology has created compelling opportunities for risk-adjusted returns in other sectors that have been ignored. Indeed, we were quite active in the period, as we found a handful of these out-of-favor corners of the market.

Exhibit 1: Differentiated Exposures in a Concentrated Market

As of March 31, 2024 (Source: ClearBridge Investments, FactSet.)

During the quarter we meaningfully increased our exposure to high-quality names in consumer staples, communications services and utilities. Our investments across these three distinct sectors share several key characteristics. These businesses are all typified by muted cyclicality, recurring revenues and a high degree of predictability. Our purchases were underwritten at undemanding valuations that embed a margin of safety and offer the potential for compelling long-term returns.

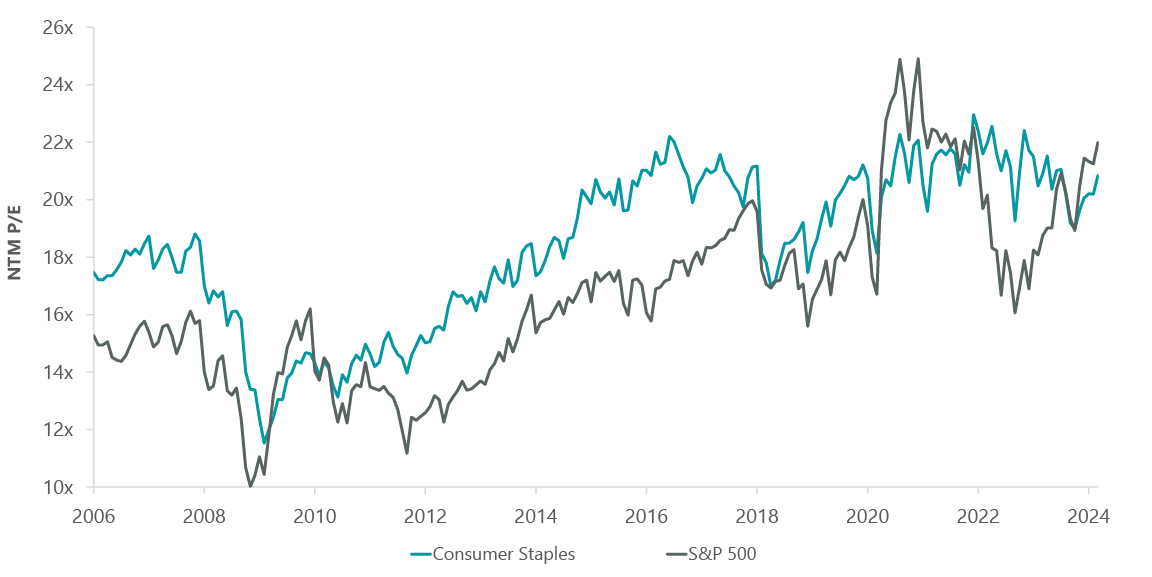

In consumer staples we added to our existing positions in Nestle (OTCPK:NSRGY), Coca-Cola (KO) and Diageo (DEO), and we initiated positions in over-the-counter health care staples companies Haleon (HLN) and Kenvue (KVUE). We purchased these staples at discounts to the broad market averages. High-quality consumer staples typically trade at a premium to the market given their stability, pricing power and attractive returns on investment (Exhibit 2). These securities offer attractive upfront yields and generate solid free cash flow, and we expect their relative valuations will ultimately return to trading at premiums to the market.

In communications services we added significantly to Comcast (CMCSA), T-Mobile (TMUS) and Walt Disney (DIS). Comcast and T-Mobile both benefit from recurring, predictable, subscription-based revenues and trade at low double-digit multiples of free cash flow. We added to Disney near the stock’s recent bottom, a level that embedded unrealistic pessimism. Disney’s low price imputed continued start-up losses in Disney+ in perpetuity, despite the company’s clear guidance that its direct-to-consumer business would reach profitability in the fourth quarter of fiscal 2024.

Exhibit 2: Staples Normally at a Premium to Market

As of March 31, 2024 (Source: ClearBridge Investments, FactSet)

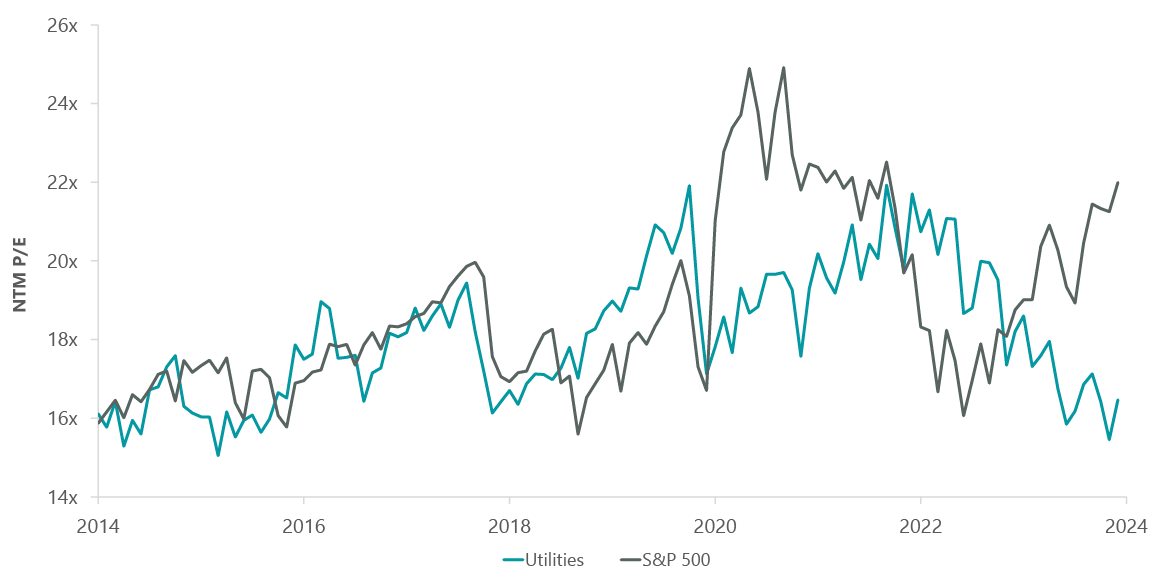

Continuing a trend begun last year, we increased our allocation to electric utilities with the addition of DTE Energy (DTE). Electric utilities offer attractive upfront yields, trade at their lowest relative valuations in a decade and – as consensus finally seems to have noticed – should enjoy stronger growth in the years ahead due to the energy transition and data centers’ phenomenal growth (Exhibit 3).

Exhibit 3: Utilities Near Lowest Relative Valuations in a Decade

As of March 31, 2024 (Source: ClearBridge Investments, FactSet.)

Of course, we are not only invested in more pedestrian sectors like consumer staples, telecommunications and utilities. We also have large positions in technology stalwarts Broadcom (AVGO), Microsoft (MSFT), Oracle (ORCL) and SAP (SAP) – all of which rose handsomely during the period. In the quarter we initiated a position in Meta after the company announced its inaugural dividend. Meta’s ecosystem of products is unparalleled, with daily active users equating to 40% of the global population. Meta is very profitable and maintains a robust balance sheet, even while investing heavily in growth. The initiation of a small but meaningful dividend, which we expect to compound steadily, is consistent with increasing capital discipline at Meta. Our active (as opposed to formulaic) approach to dividends enabled us to move quickly and buy the shares the day after Meta announced its dividend. Over the years, our nimble approach to dividend investing has frequently enabled us to profit from long-term investments in high-growth technology companies that many passive or formulaic dividend investors likely missed (e.g., American Tower, Mastercard, Meta, Visa).

Outlook

As we move into the second quarter, the market’s primary trends appear entrenched. Investor psychology remains dominated by FOMO in AI and consensus continues to believe the Fed will begin cutting rates shortly. Meanwhile, our approach remains deliberate, distinctive and consistent. We seek to enhance our diversification even as we embrace market trends like AI through measured investments in select names such as Broadcom and Microsoft. With respect to interest rates, we humbly acknowledge that our crystal ball is no better than anyone else’s. Not long ago the market was certain it would get two or three rate cuts in the back half of 2023 and early 2024; now it seems the first cut may not come until the back half of 2024. Rather than try to predict and time the Fed’s every move, we aim to construct a portfolio that will perform reasonably well under a broad range of interest rate scenarios.

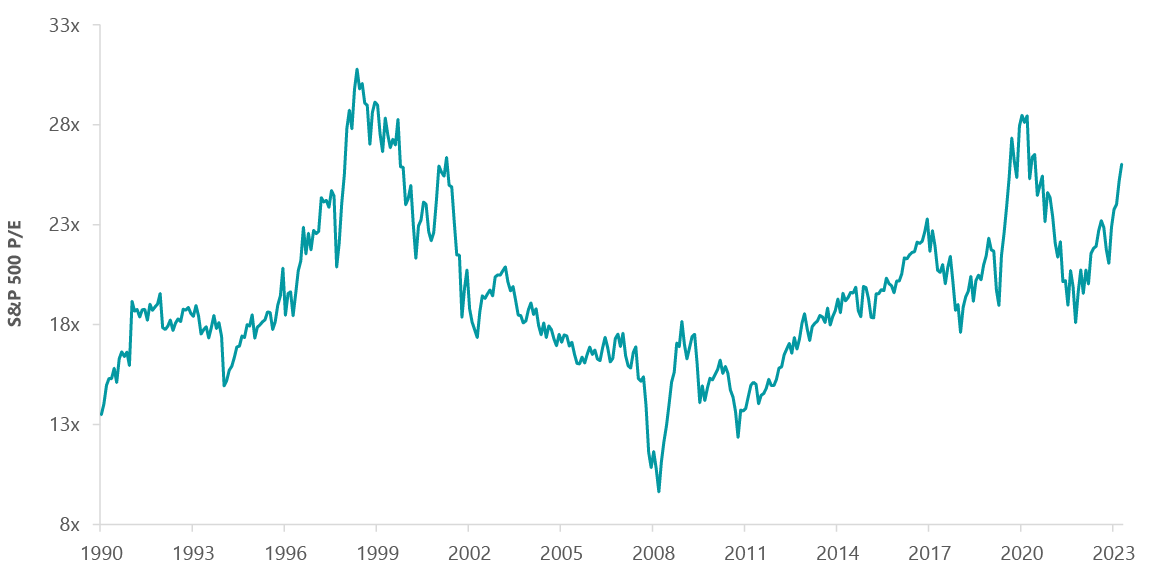

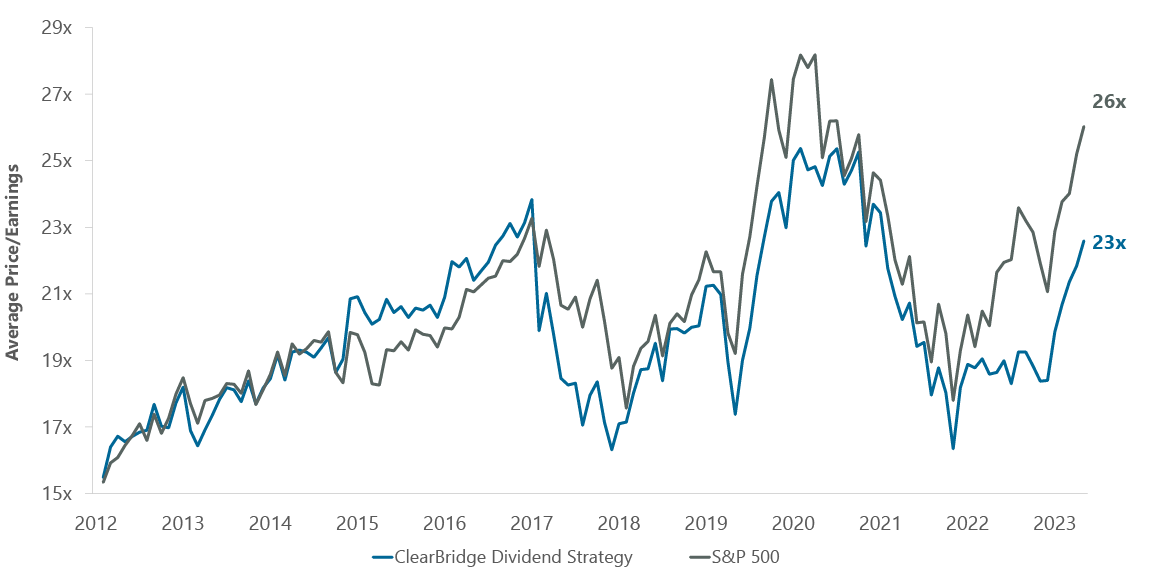

With market multiples approaching historic highs, it strikes us that many stocks likely require a cut in interest rates to sustain their levels (Exhibit 4).

Exhibit 4: Market Multiples Approaching Historic Highs

As of March 31, 2024 (Source: ClearBridge Investments, FactSet.)

Our portfolio, meanwhile, trades at much more modest valuations (Exhibit 5). This should serve us well regardless of the path of interest rates. With the market’s magnified focus on the hot new thing (AI, etc.), we are doubling down on the oldies but goodies: dividends, diversification and a disciplined approach to valuations.

Exhibit 5: ClearBridge Dividend Strategy Trading at Meaningful Discount

As of March 31, 2024 (Source: ClearBridge Investments, FactSet.)

Portfolio Highlights

The ClearBridge Dividend Strategy underperformed its S&P 500 Index benchmark during the first quarter. On an absolute basis, the Strategy saw positive contributions from nine of 11 sectors in which it was invested for the quarter. The financials and IT sectors were the main positive contributors, while the real estate and utilities sectors detracted.

On a relative basis, stock selection and sector allocation detracted. In particular, stock selection in the health care, communication services, IT, consumer staples and utilities sectors, an overweight to the real estate sector and an underweight to the IT sector weighed on relative results. Conversely, stock selection in the financials and consumer discretionary sectors and an underweight to the consumer discretionary sector proved beneficial.

On an individual stock basis, the main positive contributors were Apollo Global Management (APO), Microsoft (MSFT), JPMorgan Chase (JPM), Vulcan Materials (VMC) and Travelers (TRV). Positions in Apple (AAPL), Intel (INTC), American Tower (AMT), Nestle and UnitedHealth Group (UNH) were the main detractors from absolute returns in the quarter.

In addition to portfolio activity discussed above, we also initiated a new position in Air Products and Chemicals (APD) in the materials sector and exited Chesapeake Energy (CHK) in the energy sector, Pfizer (PFE) in the health care sector, Cisco Systems (CSCO) in the IT sector and Mastercard in the financials sector.

Michael Clarfeld, CFA, Managing Director, Portfolio Manager

Peter Vanderlee, CFA, Managing Director, Portfolio Manager

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

Performance source: Internal. Benchmark source: Standard & Poor’s.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

{kind=link}