Hiraman

By Jeffrey Bailin, CFA & Aram Green

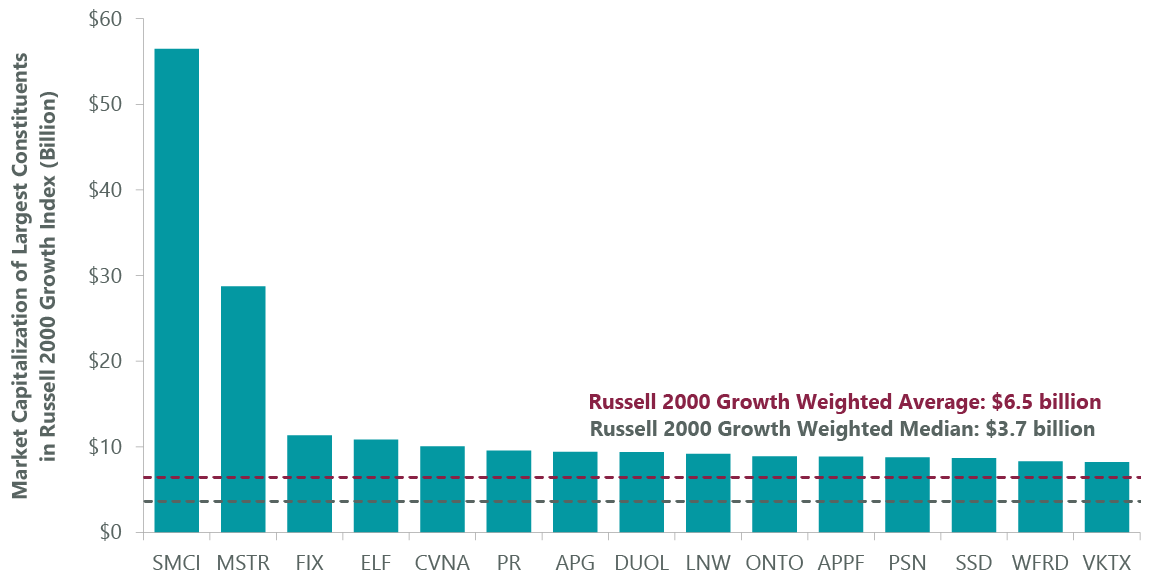

Benchmark Concentration Even More Severe in Small Growth

Market Overview

Entering 2024, we were hopeful that, after a year of extreme relative underperformance versus large cap peers, conditions were aligning for a broadening market more favorable for small cap stocks. Thus far, it has been more of the same, as large has outperformed small, paced by growth over value across market capitalizations. The benchmark Russell 2000 Growth Index returned 7.58% in the first quarter but the positive performance obscured a stark dichotomy within the small cap growth universe.

While large cap benchmarks get a lot of attention for a handful of mega cap stocks driving the lion’s share of performance, we would highlight even more extreme and unprecedented concentration in small cap benchmarks. Year to date, one stock, Super Micro Computer (SMCI) has driven 37% of the return of the benchmark, closely followed by MicroStrategy (MSTR), a unique stock that is largely considered a bitcoin proxy. Together, they accounted for over half of the benchmark’s first quarter return. This compares to Nvidia (NVDA), which accounted for 24% of the return of the S&P 500 Index (SP500). The 32 top-performing stocks in the Russell 2000 Growth Index accounted for 100% of its return, versus 81 names driving the S&P 500’s performance this quarter.

Currently, SMCI is the largest constituent by weight in our benchmark, and it peaked at over 4.5%, representing the largest individual security weight in a monthly dataset going back to 1985. That represented a weighting 83% higher than the second-largest weight (from 1999). Moreover, MicroStrategy at its peak this past quarter would have represented the fourth-largest security in the 38 years of the monthly dataset. We are hard-pressed to recall another instance where the largest constituent of our benchmark was also added to the S&P 500, as SMCI was this March. We would note that SMCI currently is a $61 billion market capitalization company and MicroStrategy boasts a market capitalization of $28 billion, both well above the $6.8 billion weighted average market cap of the Strategy.

Exhibit 1: Largest Components in Russell 2000 Growth Index

As of March 31, 2024 (Source: ClearBridge Investments, FactSet.)

Enthusiasm for AI and bitcoin have fueled this atypical concentration and performance distortion. Bitcoin rallied fast and furiously following the SEC’s approval of the first bitcoin ETF in early January, while the AI infrastructure build-out has had a narrow set of beneficiaries. Against this backdrop, the ClearBridge Small Cap Growth Strategy underperformed its benchmark. We are disappointed by this result, although 79% of the relative underperformance was due to not owning these two large benchmark holdings, which have fundamental and governance factors that have caused us, as long-term investors focused on quality sustainable growth stories, to avoid them. Finally, not owning biotech Viking Therapeutics (VKTX) for the entire period, another large benchmark weight, which appreciated significantly on GLP-1 potential and which we purchased in March, accounted for another 10% of the underperformance.

Portfolio Positioning

Encouragingly, we are seeing underlying improvements from companies we do own in the portfolio, with several being recent portfolio additions or subjects of repositioning work executed in 2023.

We would also highlight several longstanding portfolio holdings that saw meaningful returns in the first quarter, including Wingstop (WING), XPO (XPO) and Trex (TREX). These businesses are seeing results from idiosyncratic revenue and margin drivers, along with attractive returns on invested capital.

The first quarter represented another period of fruitful new idea generation with nine new investments. Consistent with historical practice, these initial investments represent modest position sizes that we intend to build over time.

- Viking Therapeutics is focused on metabolic and endocrine diseases. While still early stage, the company has had positive Phase 2 data on a GLP-1/GIP agonist injectable candidate potentially differentiated in mechanism with encouraging results relative to existing approved/pipeline candidates. The company is also pursuing an oral obesity GLP-1/GIP treatment and has a Phase 2 compound to treat nonalcoholic fatty liver disease, or NASH. Given the strong growth potential in the obesity market, multiple potential products and scarcity value in the small cap universe, we believe this is an attractive potential opportunity with sufficient capital to support near-term clinical development goals.

- CONMED (CNMD) is a medical device provider focusing on the orthopedic and general surgery categories. The business is balanced globally with over 80% of revenues coming from single-use products. CONMED has a handful of high-growth products, with competitive differentiation, early in their penetration.

- RadNet (RDNT) owns and operates outpatient freestanding diagnostic imaging centers. The market is seeing secular growth from a shift in the site of care from the more expensive inpatient setting to freestanding imaging centers like RadNet. With solid organic growth, coupled with an attractive de novo and acquisition opportunity, the company has a long runway to compound topline growth. RadNet has also invested heavily in newer AI applications that can provide an additional revenue stream, while also improving the early identification of cancers.

- Medpace (MEDP) provides outsourced clinical research drug development services to the pharmaceutical and biotechnology sectors. Medpace’s full-service focus on small-midsize biotech customers should allow it to post above-peer growth with strong profitability and cash flow generation.

- Insmed (INSM) is a biopharmaceutical company focused primarily on rare pulmonary diseases. The company has an approved and marketed product still growing in domestic and international markets, along with opportunities to expand its initial indication. Moreover, the company has several late-stage clinical candidates with blockbuster sales potential.

- Intapp (INTA), in the IT sector, is a vertical software provider with a leading position serving the professional and financial services industry. Its tailored offerings provide enterprise resource planning, customer relationship management and compliance solutions, tailored specifically for these verticals. We see significant runway to expand the modules sold to their existing clients, supporting robust growth and expanding margins.

- Duolingo (DUOL), in the consumer discretionary sector, is a category leader in online language learning. With a freemium digital education model offering 40+ languages, Duolingo’s application has exhibited rapid growth in users and conversion to paid subscribers. The company has opportunity to expand its English-learning focus as well as broaden into new categories like math and music. Duolingo offers a long history of product innovation, marketing efficiency and attractive profitability/unit economics.

- e.l.f. Beauty (ELF), in the consumer staples sector, is a mass cosmetics and skincare provider in the U.S., selling professional-quality makeup and skincare products at an attractive price point relative to legacy brands. With a significant online, direct-to-consumer presence and clean product ingredients, the company has been a strong market share gainer with multiple levers to sustain elevated growth.

We had one company acquired in the quarter: Masonite, a manufacturer of doors and accessories, announced its intent to be acquired by Owens Corning. We sold life science tools and services provider Olink (OLK) ahead of the closure of its acquisition by Thermo Fisher Scientific, originally announced in 2023. We also exited Omnicell (OMCL) and Integra LifeSciences (IART) in health care and Forward Air (FWRD) in industrials following persistent fundamental challenges.

Outlook

Through the first quarter, we have seen signs of optimism with continued spending on innovation, particularly in growth areas like AI and health care. M&A and capital markets activity are also attempting to expand from early green shoots. At a macro level, indicators offer crosscurrents with stickier elements of inflation and a still-hot labor environment balanced by more encouraging trends in other areas of the economy. Rate cuts from the Fed are expected this year with a possibility of policymakers navigating a soft landing. While acknowledging the increasing likelihood of such a scenario, we are mindful of government dysfunction, a looming contentious election cycle and geopolitical tensions, all of which could create volatility.

The ClearBridge Small Cap Growth Strategy remains committed to identifying idiosyncratic companies with growth opportunities and attractive returns irrespective of the macro backdrop. The guiding principles that have also informed our investment process and philosophy remain at the core of our process to exercise “judgment and patience” to ensure that we have 1) the right balance of opportunity and risk in the Strategy, and 2) appropriately capitalized investments with substantial intermediate to long-term growth opportunities.

Portfolio Highlights

The ClearBridge Small Cap Growth Strategy underperformed its benchmark in the first quarter. On an absolute basis, the Strategy posted gains across five of the nine sectors in which it was invested (out of 11 sectors total). The primary contributors to performance were in the industrials, consumer discretionary and consumer staples sectors while the main detractors included the communication services, financials and health care sectors.

Relative to the benchmark, overall stock selection detracted from performance but was partially offset by positive sector allocation effects. In particular, stock selection in the IT sector was the primary drag on results while selection in health care, communication services, financials and industrials also weighed on performance. On the positive side, stock selection in the consumer discretionary, consumer staples and energy sectors, an overweight to IT and a lack of exposure to utilities contributed to returns.

On an individual stock basis, the leading absolute contributors were positions in Wingstop, XPO, Trex, Casey’s General Stores (CASY) and Tennant (TNC). The primary detractors among names held in the portfolio were Iridium Communications (IRDM), Xometry (XMTR), Shoals Technologies (SHLS), Fox Factory (FOXF) and Integra LifeSciences. Not holding significant benchmark weights that saw rapid total returns in the quarter including Super Micro Computer, MicroStrategy and Viking Therapeutics were the most significant relative detractors.

In addition to the transactions mentioned above, we also added a new position in Arcadium Lithium (ALTM) (OTC:ARLTF) in the materials sector. We exited existing holding Livent in the materials sector.

Jeffrey Bailin, CFA, Director, Portfolio Manager

Aram Green, Managing Director, Portfolio Manager

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication.

Performance source: Internal. Benchmark source: Standard & Poor’s.

{kind=link}