Moving

Moving

money across borders should be as instant and frictionless as sending a text message. For businesses operating between established financial hubs like the UK or EU and rapidly growing emerging markets, the reality is much more complicated. Building the infrastructure

to connect these distinct ecosystems requires solving a complex puzzle of mismatched technology, differing regulatory speeds, and intricate payment networks.

To bridge these worlds, we have to look closely at the mechanics of modern cross-border systems and what it actually takes to stitch them together.

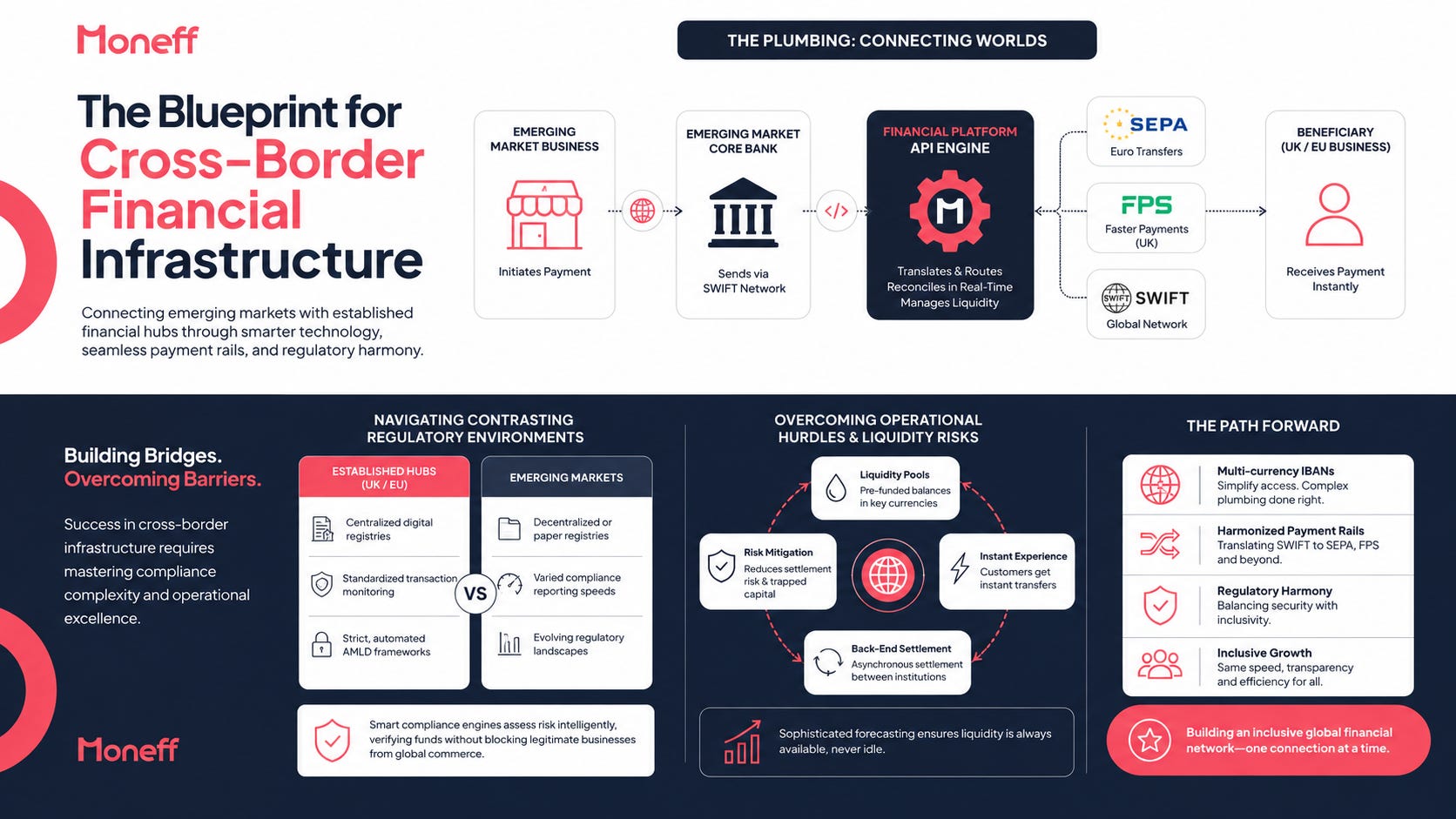

The plumbing

At the heart of international trade is the ability to hold, receive, and send multiple currencies without maintaining dozens of local bank accounts. This is where multi-currency IBANs become essential. A single IBAN capable of handling Euros, British Pounds,

and local emerging market currencies simplifies the user experience on the surface, but the underlying plumbing is highly intricate.

An emerging market core bank must communicate smoothly with our API engine, which then routes instructions out to networks like SEPA, SWIFT, or the UK’s Faster Payments Service.

When integrating with the European Union, the standard is the Single Euro Payments Area (SEPA). SEPA streamlines Euro transfers, making them cheap and fast. For the UK, the Faster Payments System (FPS) offers similar near-instant capabilities for Sterling.

The challenge arises when an emerging market bank, which often relies exclusively on the SWIFT network, tries to interact with these localized, high-speed rails.

SWIFT is reliable and globally recognized, but it can be slow and expensive due to its reliance on a chain of correspondent banks. Each bank in the chain takes a fee and adds processing time. To build a seamless bridge, financial platforms must act as translators.

We have to ingest a SWIFT message from an emerging market, convert the financial data into the specific formats required by SEPA or FPS, and clear the transaction without delay. This requires robust API engines that can reconcile transactions in real time,

ensuring that liquidity is available in the right currency at the exact moment it is needed.

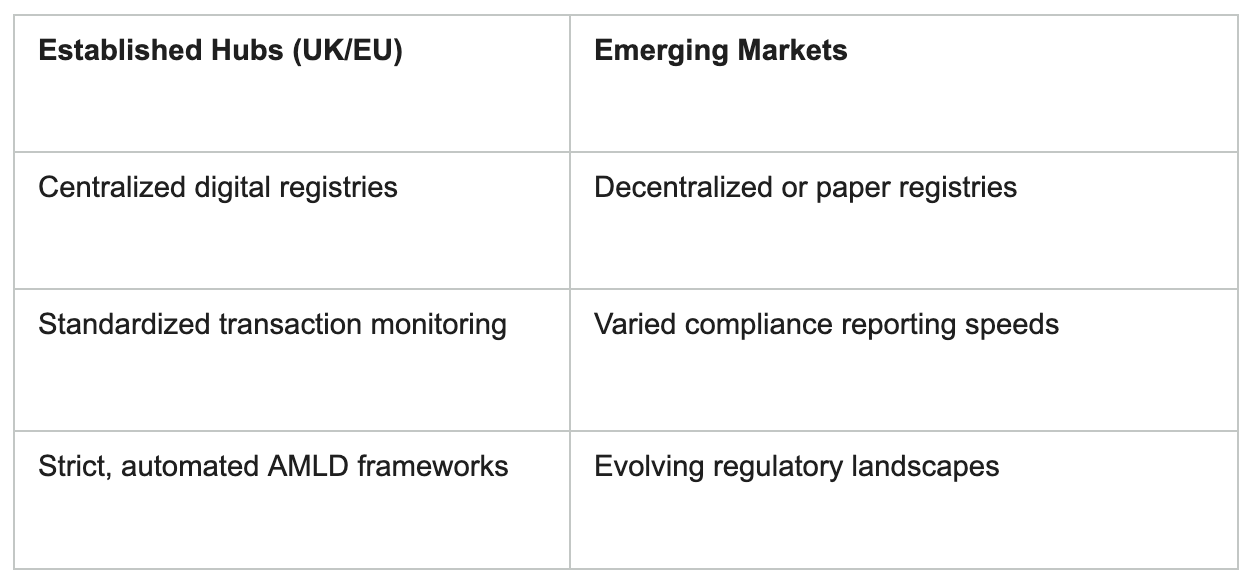

Navigating contrasting regulatory environments

Technical connectivity is only half the battle. The more formidable hurdle is navigating the regulatory friction between different jurisdictions.

The UK and the EU operate under highly sophisticated, deeply structured compliance frameworks. Rules like the EU’s Anti-Money Laundering Directives (AMLD) and strict Know Your Customer (KYC) requirements demand deep scrutiny of every transaction.

Emerging markets are also strongly committed to fighting financial crime, but their regulatory frameworks often develop at a different pace or rely on different documentation styles. For example, verifying the ultimate beneficial owner of a business in a

region without a centralized, digital corporate registry is a manual and time-consuming process.

Building a successful cross-border corridor means creating a compliance engine that satisfies both sides. It involves implementing transaction monitoring systems that can assess risk intelligently. Instead of applying a blunt, one-size-fits-all rule that

rejects unusual but legitimate transactions from developing regions, infrastructure providers must use contextual data to verify funds. This keeps the channels secure without shutting out valid businesses from global commerce.

Overcoming operational hurdles and liquidity risks

Operating across time zones and currency corridors introduces significant operational hurdles, particularly regarding liquidity management and settlement times.

When a business in an emerging market wants to pay a supplier in the EU, the exchange rate can fluctuate wildly in a matter of minutes. If the local banking day ends before the European markets open, capital can get trapped in transit. This creates settlement

risk.

To mitigate this, financial infrastructure providers must maintain strategic liquidity pools in key hubs. By holding balances of Euros, Pounds, and major emerging market currencies in reserve, we can pre-fund transactions. This allows the end customer to

experience an instant transfer, while the actual back-end settlement between institutions happens asynchronously. Managing these pools requires sophisticated forecasting models to ensure capital is never parked inefficiently, yet always available to grease

the wheels of trade.

The path forward

Connecting emerging markets with major financial hubs is not a matter of replacing existing systems, but of building smarter bridges between them. It requires a deep respect for local operational realities combined with a strict adherence to international

compliance standards.

By mastering the mechanics of multi-currency IBANs, harmonizing payment rails, and managing regulatory friction with smart technology, we can create a genuinely inclusive global financial network. The businesses driving growth in emerging economies deserve

the same speed, transparency, and efficiency that European enterprises take for granted. Building that blueprint is the defining task for the next generation of financial platforms.