Binance and several other crypto exchanges have begun offering stock trading services. This report examines what it means that exchanges are expanding into conventional finance.

-

The limits of the crypto trading fee model, the rise of perpetual futures DEXs led by Hyperliquid, and a more permissive regulatory environment following the Trump administration have together pushed major global crypto exchanges to reconsider their direction.

-

The path those exchanges are now pursuing points toward conventional financial products such as stocks and derivatives, and toward operating structures that resemble tradFi.

-

The complication is that centralized exchanges have been the primary liquidity providers sustaining the crypto ecosystem. If they step back from that role, the crypto market may not function the way it once did.

-

A period of self-reliance is beginning for crypto projects. Projects that can survive without exchange support and those that cannot are about to diverge.

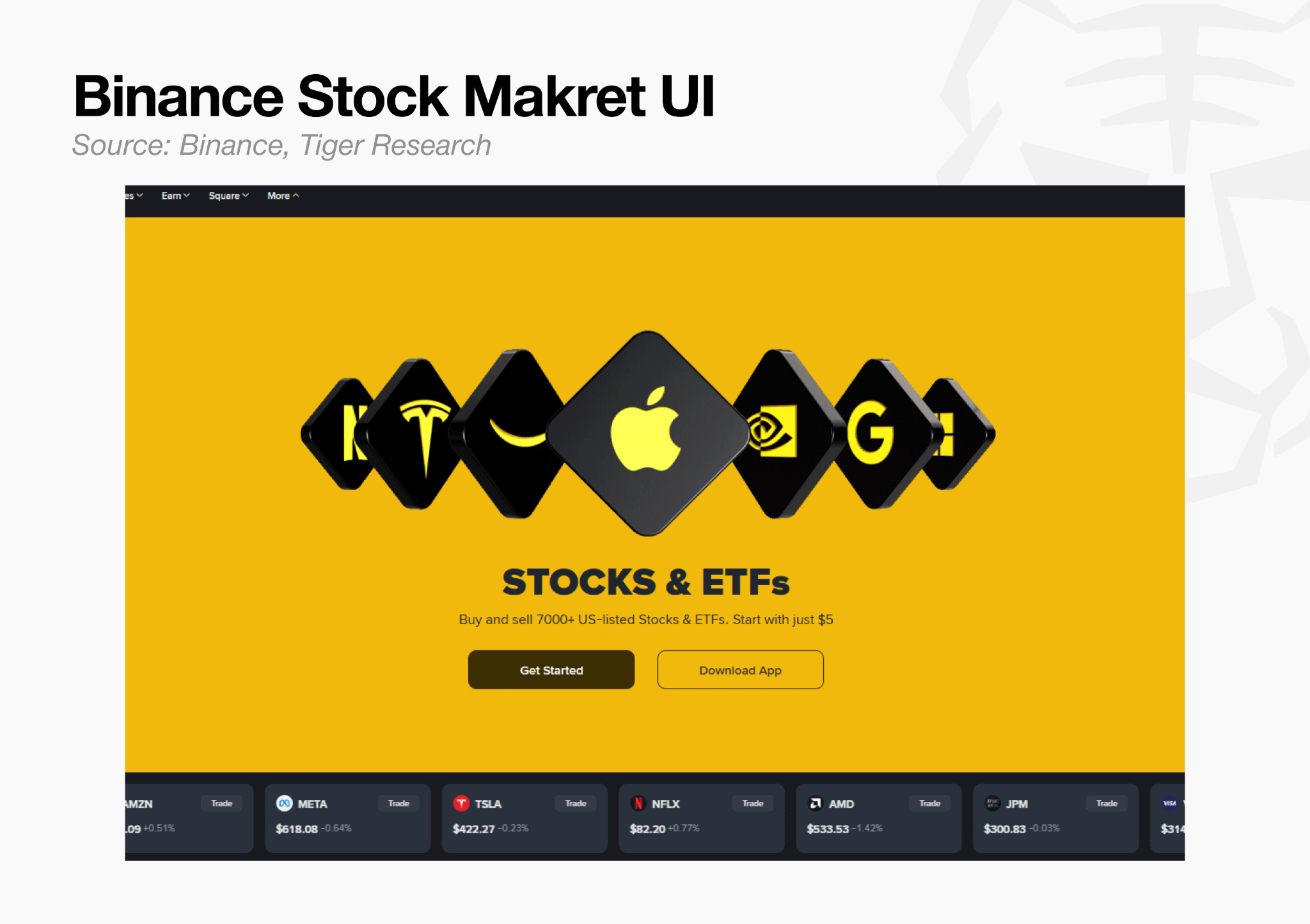

Since June 1, users have been able to buy stocks such as Apple (AAPL) and Alphabet (GOOGL) directly through the Binance app. The following day, Binance announced support for trading in SK Hynix, Samsung Electronics, and Hyundai Motor, three of the most actively traded stocks on the KOSPI.

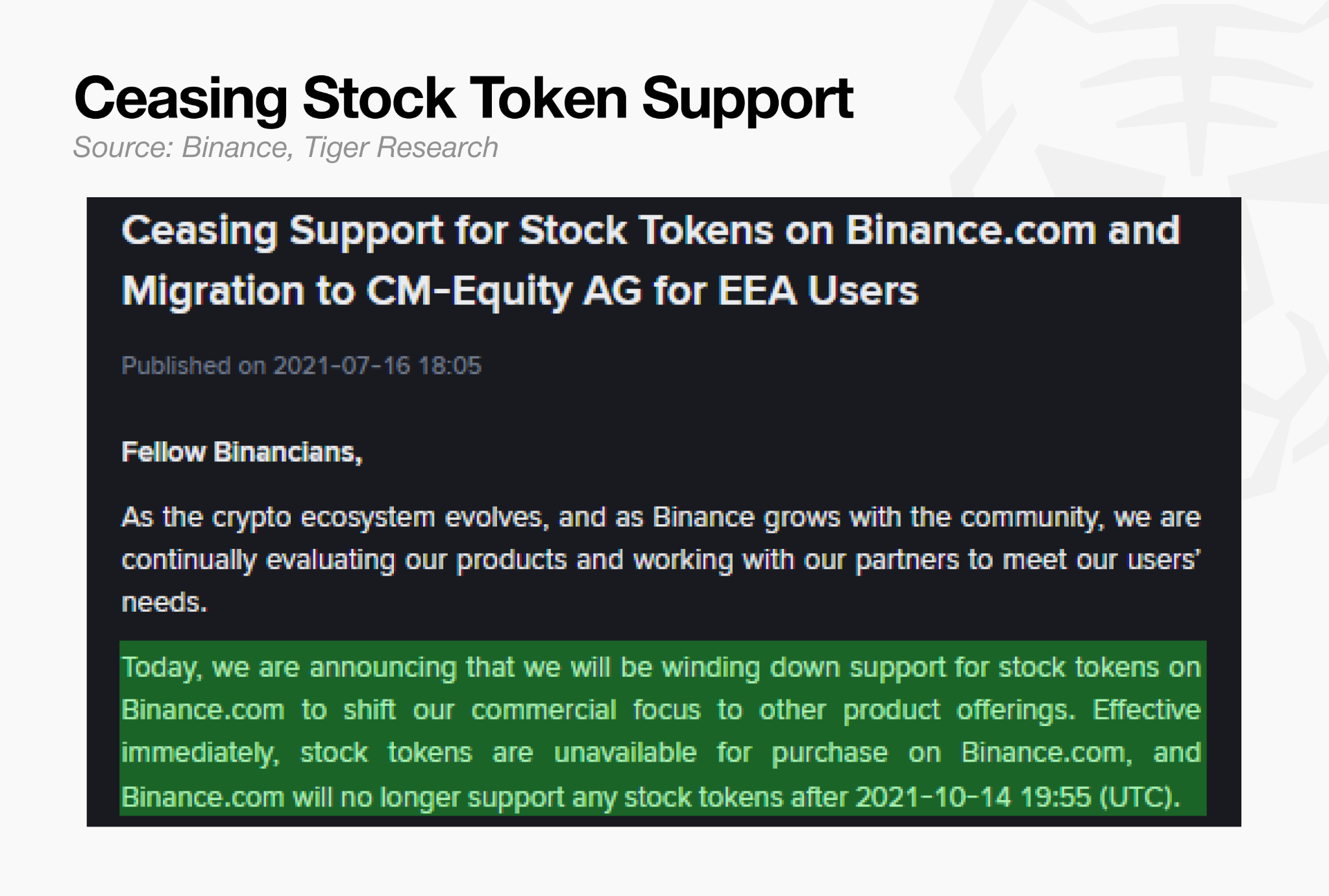

Binance’s interest in stock markets dates to 2021. That April, the exchange launched tokenized stock trading covering Tesla (TSLA), Apple (AAPL), and Microsoft (MSFT), only to shut the service down entirely by July of the same year under mounting regulatory pressure. Three structural problems had made the product untenable: the legal classification of stock tokens as securities versus derivatives was unresolved; the investor prospectuses required under EU regulations were absent; and Binance itself held no direct license to operate such a service. Germany’s BaFin, the UK’s FCA, and Hong Kong’s SFC all raised objections on those grounds.

The current launch is structured differently. Binance has routed order execution through a broker-dealer licensed by the Abu Dhabi Global Market (ADGM), giving the service a clear legal classification as brokerage. The ambiguity over who issues the underlying instrument, which was a central point of contention in 2021, is largely removed.

The timing is notable. Bybit launched a TradFi perpetual futures market around the same period, adding coverage of KOSPI names including SK Hynix and Samsung Electronics as well as perpetual futures on SpaceX (SPCX). Coinbase separately announced support for SPCX futures trading.

The question is why the major crypto exchanges have begun moving in the same direction at roughly the same time, away from a crypto-only model and toward something that more closely resembles a conventional financial services app.

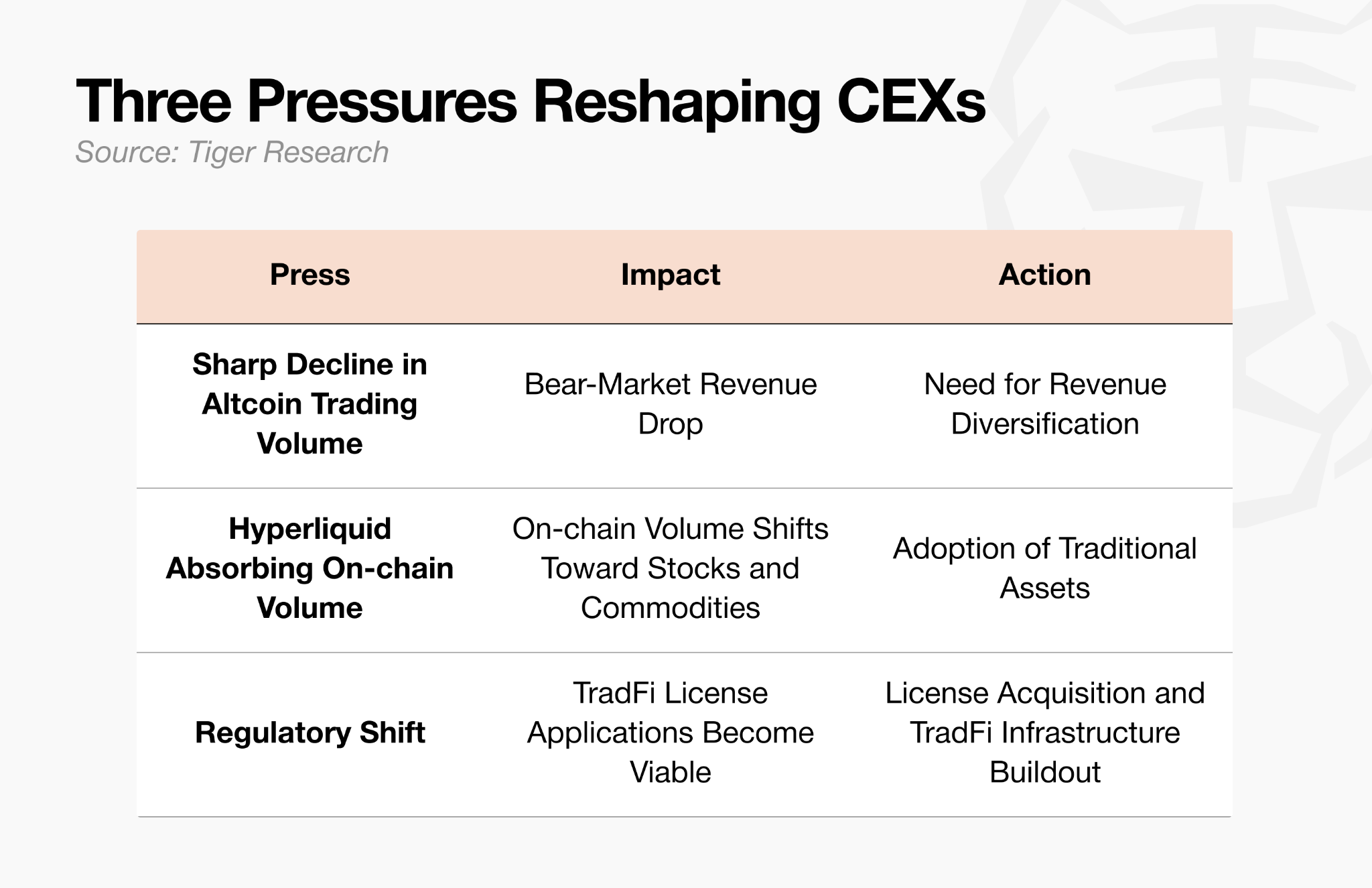

Three forces have pushed exchanges away from the crypto-only model.

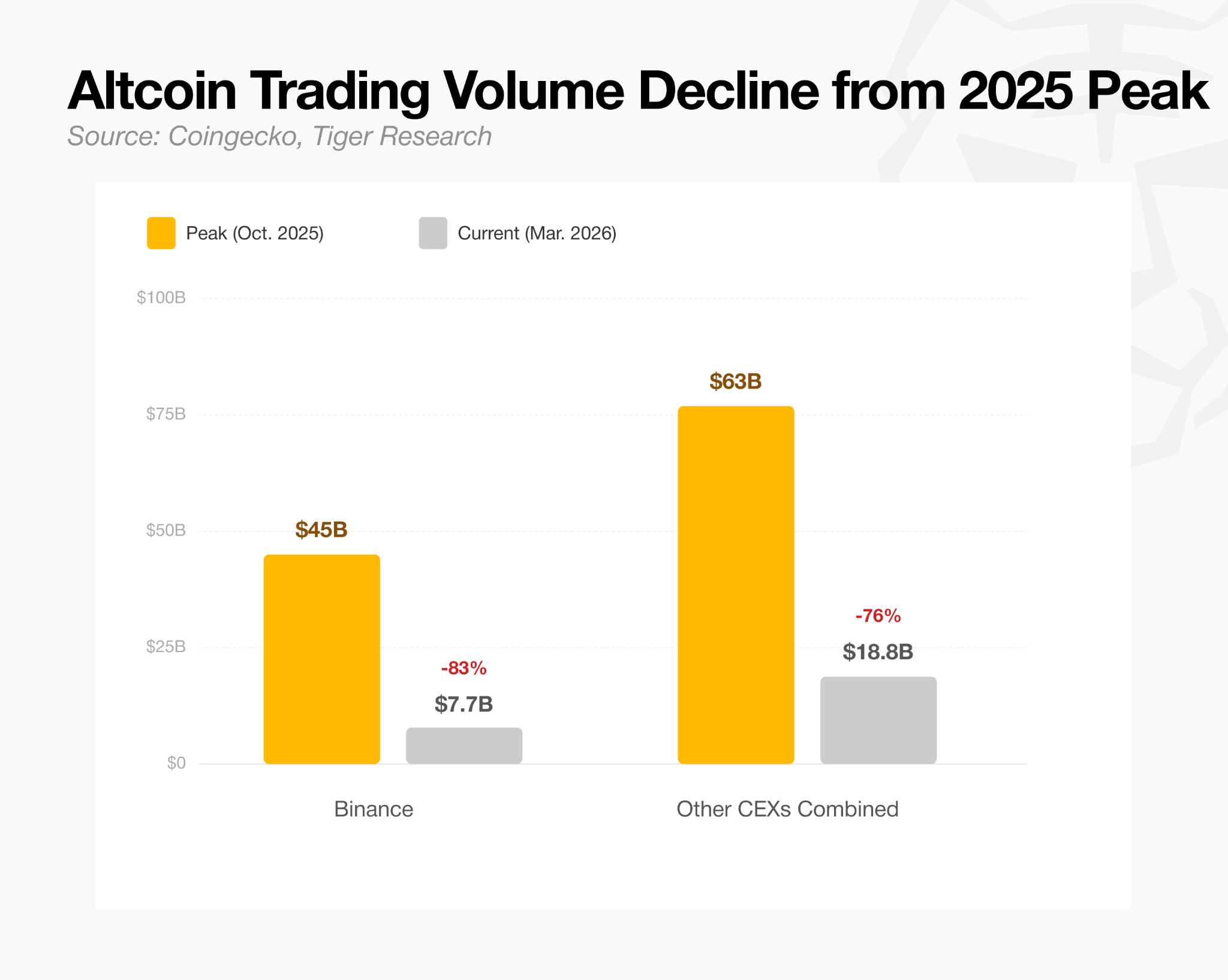

The first pressure is the decline in crypto trading volume. Exchange revenue is ultimately tied to altcoin trading volume, and that volume is determined by market sentiment.

On Binance, daily average spot trading volume fell roughly 80%, from a peak of approximately $45B in October 2025 to $7.7B today. Across other centralized exchanges combined, volume dropped around 70%, from a peak of roughly $63B to $18.8B. As trading volume declined, the fee-based revenue model began to break down. That a business model dependent on crypto trading fees cannot produce a sustainable revenue structure is something the exchanges themselves had long recognized.

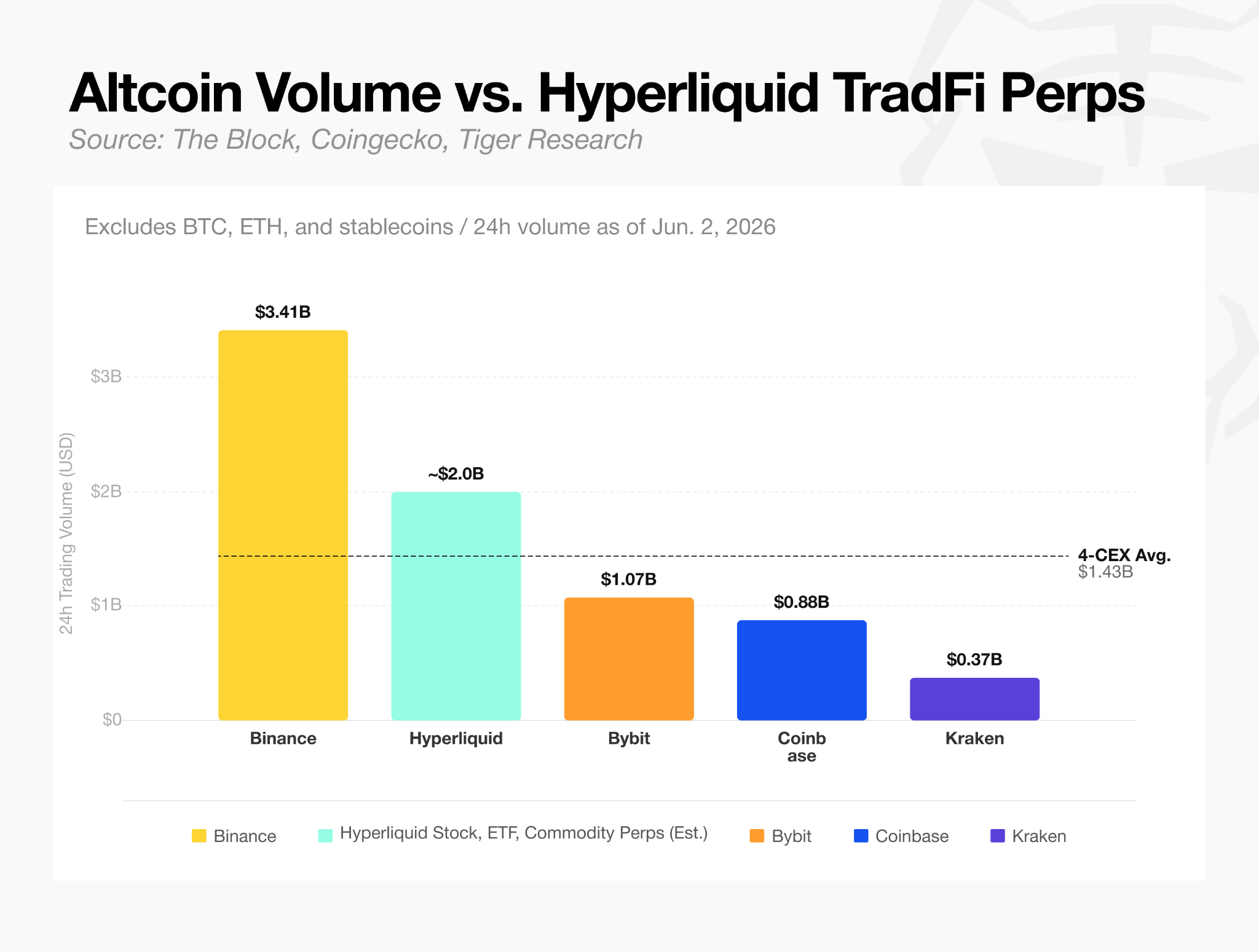

Comparing altcoin trading volume outside of Bitcoin and Ethereum against RWA asset volume including stocks and commodities on Hyperliquid makes the current situation clear.

Hyperliquid has begun drawing on-chain liquidity by supporting futures trading in stocks and commodities. As of mid-2026, 23 of the top 30 assets by perpetual futures volume on Hyperliquid were stocks and commodities, not crypto.

The premise that on-chain activity belongs exclusively to crypto no longer holds. The emergence of a decentralized exchange whose volume rivals that of centralized exchanges has put those exchanges on notice.

The third pressure came from the change in the regulatory landscape following the start of the Trump administration. The SEC dropped its lawsuits against Coinbase and Kraken. When regulators were adversarial, applying for conventional financial licenses carried real risk. Those licenses can now serve as a mark of credibility and a point of differentiation.

With clearer boundaries around what is and is not permissible, exchanges can build on their existing strengths and pursue a new direction. All three pressures converged at roughly the same time, as interest in stocks and other derivatives has also grown. Crypto exchanges now have little choice but to move quickly, along its own path, if they intend to survive.

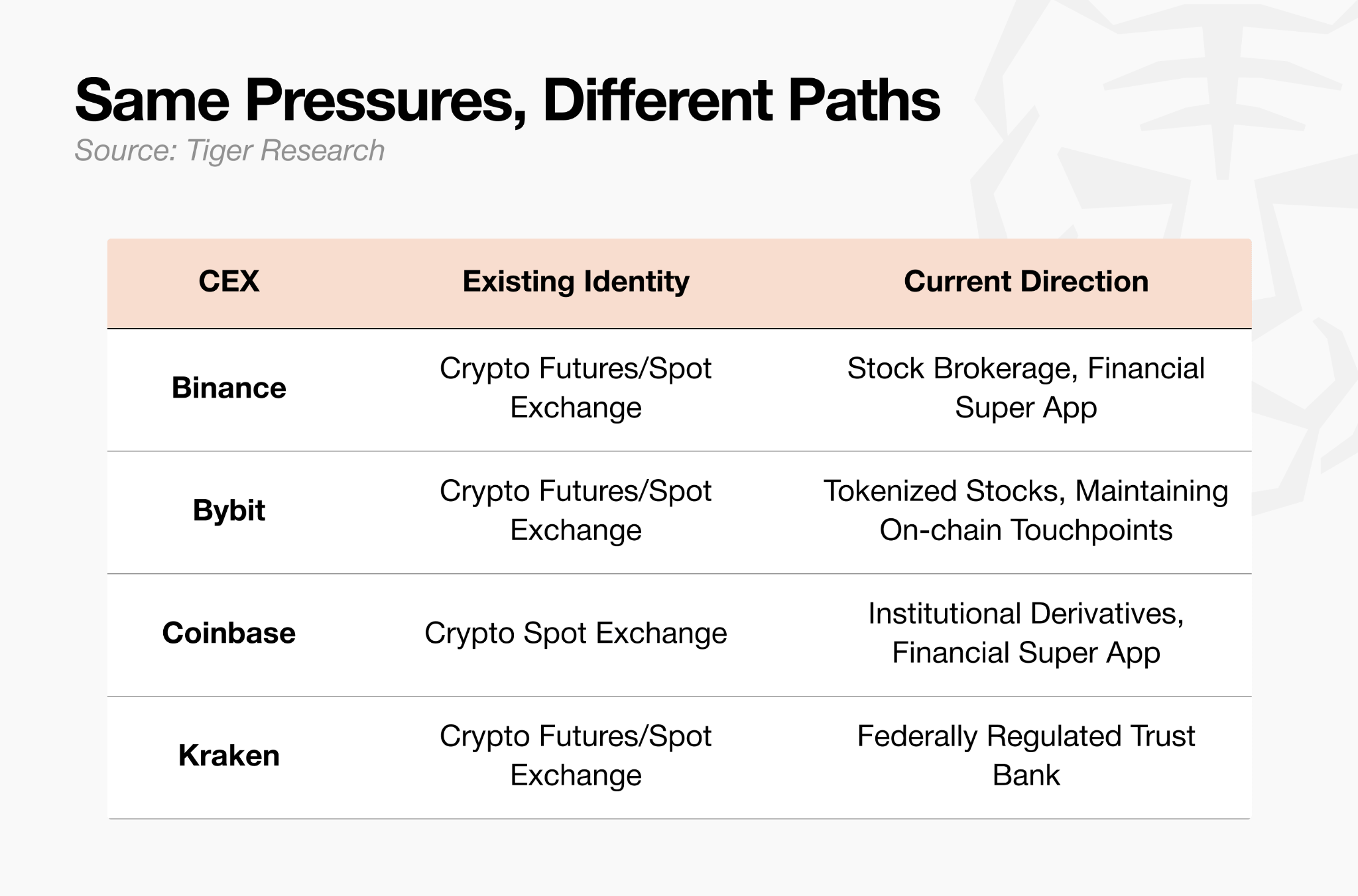

Centralized exchanges have faced the same set of pressures at the same time, but their responses have diverged.

Binance’s strategy is straightforward. The goal is to become an everything store, keeping all trading activity within its own platform and preventing users from leaving.

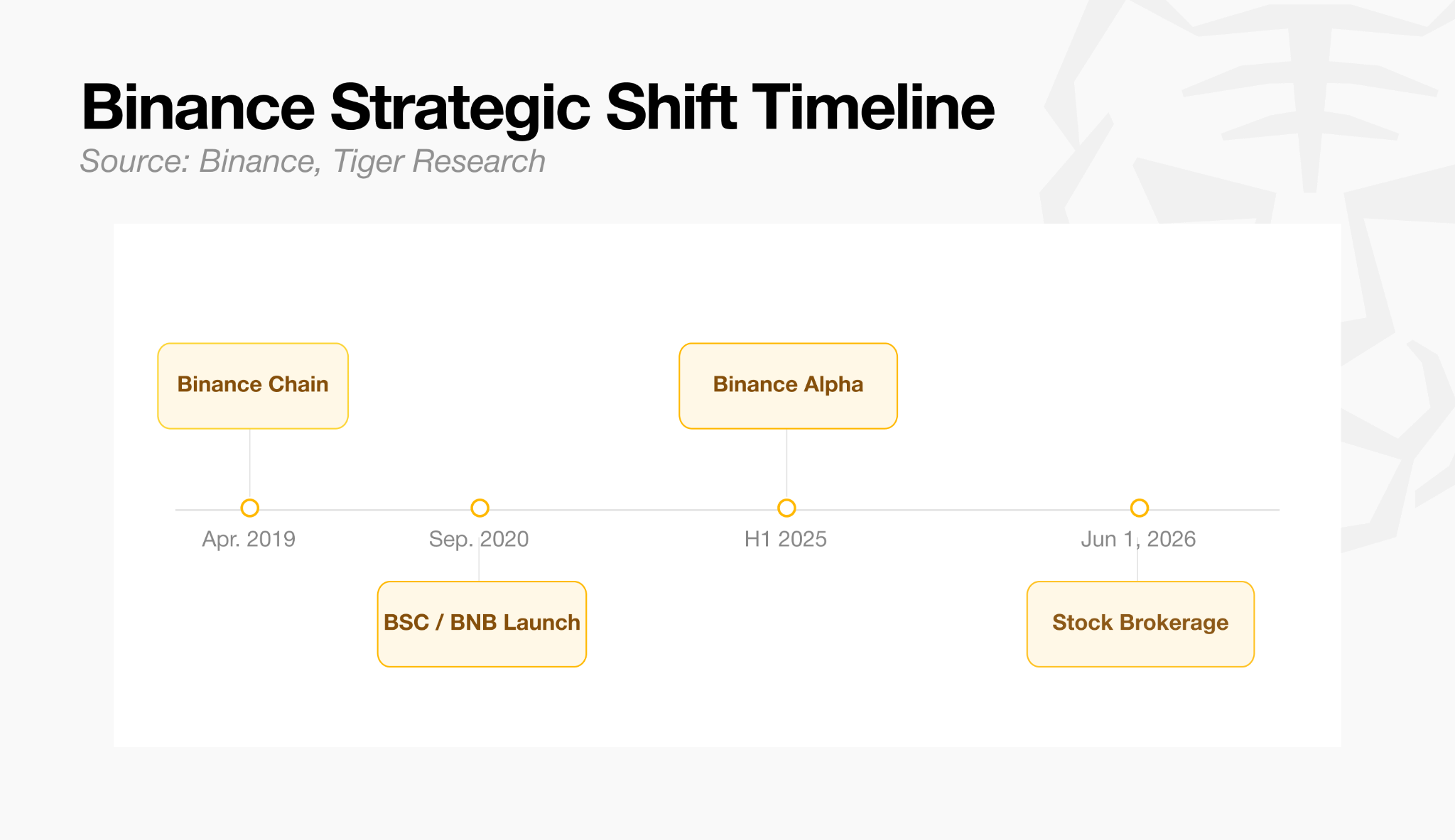

Binance had already moved on-chain and done so successfully. Having built its exchange business first, the company launched Binance Chain in April 2019 to capture the on-chain ecosystem, then followed with Binance Alpha in the first half of 2025, taking a meaningful share of on-chain activity.

By 2026, however, on-chain liquidity had begun shifting toward stock markets. When Hyperliquid moved quickly to absorb that liquidity through stocks and commodities, the on-chain user base Binance had cultivated came under pressure. Binance’s response was not to compete with Hyperliquid on-chain directly. Instead, it focused on launching a stock trading service aimed at its existing user base of over 200 million. Retaining users it already has is a more defensible position than fighting Hyperliquid on Hyperliquid’s own ground.

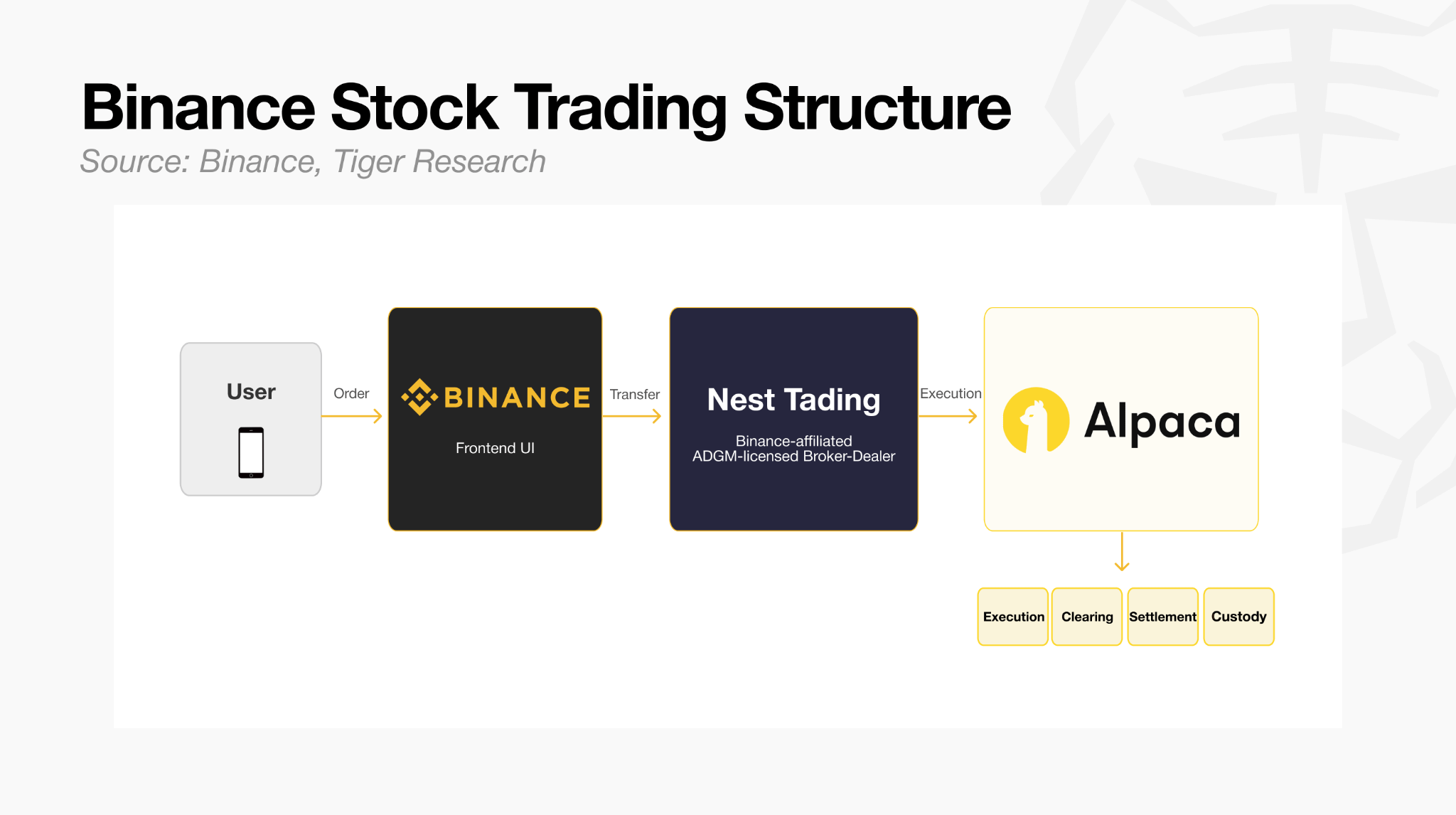

The structure works as follows. Orders placed through the Binance front end are received by Nest Trading, an ADGM-licensed broker-dealer, which then routes them to Alpaca Securities. Execution, clearing, settlement, and custody are all handled by Alpaca. Binance does not hold the securities directly, a structural choice that keeps it outside the scope of direct securities regulation.

Worth noting is that Nest Trading has been identified as a Binance affiliate. Binance also holds a minority stake in Alpaca, and the revenue-sharing arrangement gives Nest Trading 50% of order flow fees and 65% of stock lending income.

Binance is building the infrastructure itself, reorienting toward a financial super-app, and working to hold its existing users before altcoin volume migrates further toward Hyperliquid and stocks.

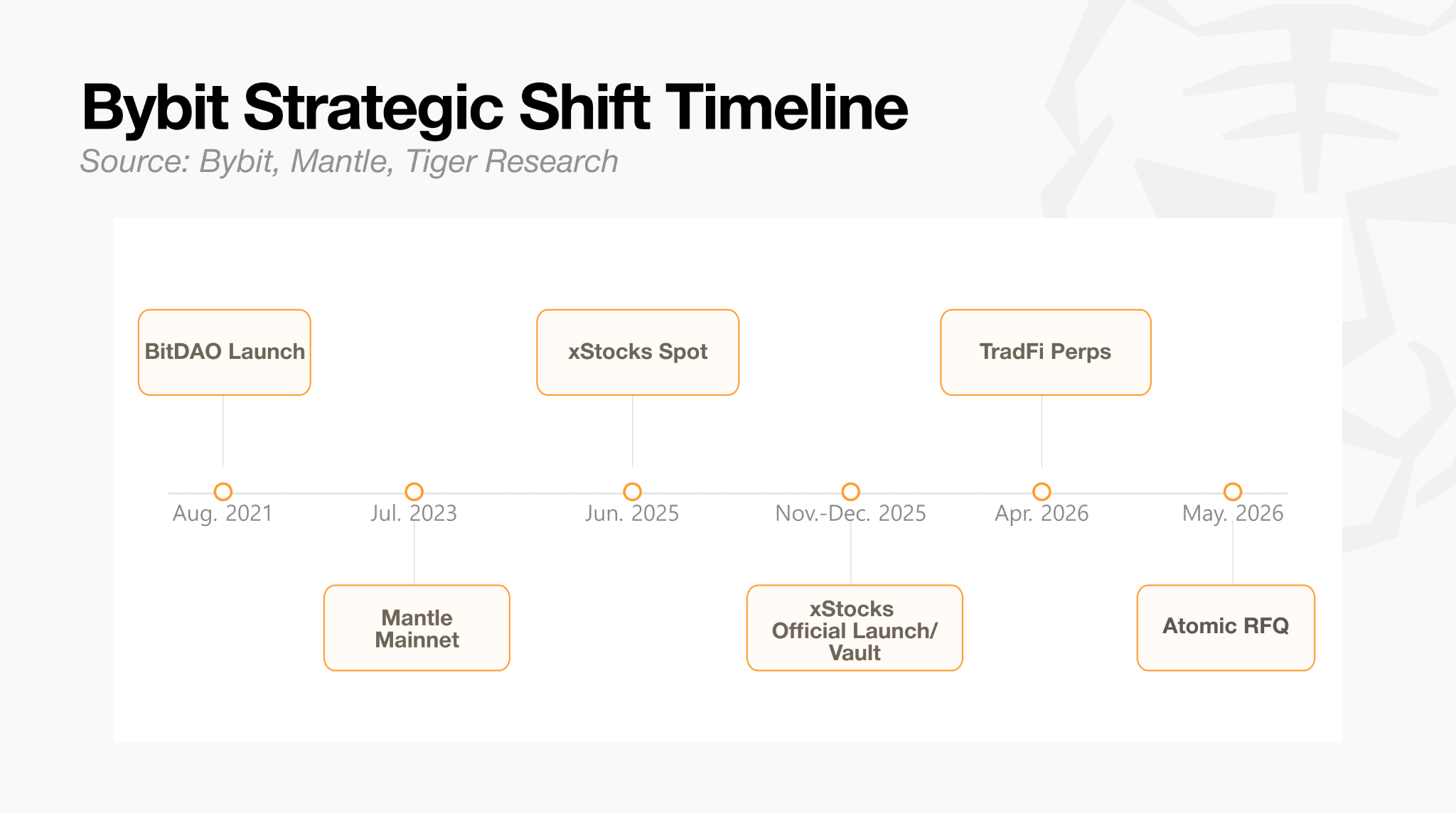

Bybit launched in 2018 as a derivatives exchange and grew rapidly on the back of up to 100x leverage and low fees. It is now running two tracks simultaneously: porting centralized exchange liquidity onto the blockchain, and listing conventional asset derivatives directly on the centralized exchange.

The on-chain track came first. In June 2025, Bybit listed Backed‘s xStocks on its spot market, marking its first step into tokenized stock partnerships. That November, a three-way collaboration with Mantle and Backed produced a formal launch of xStocks on the Mantle blockchain, covering major US stocks including Nvidia (NVDA) and Apple (AAPL).

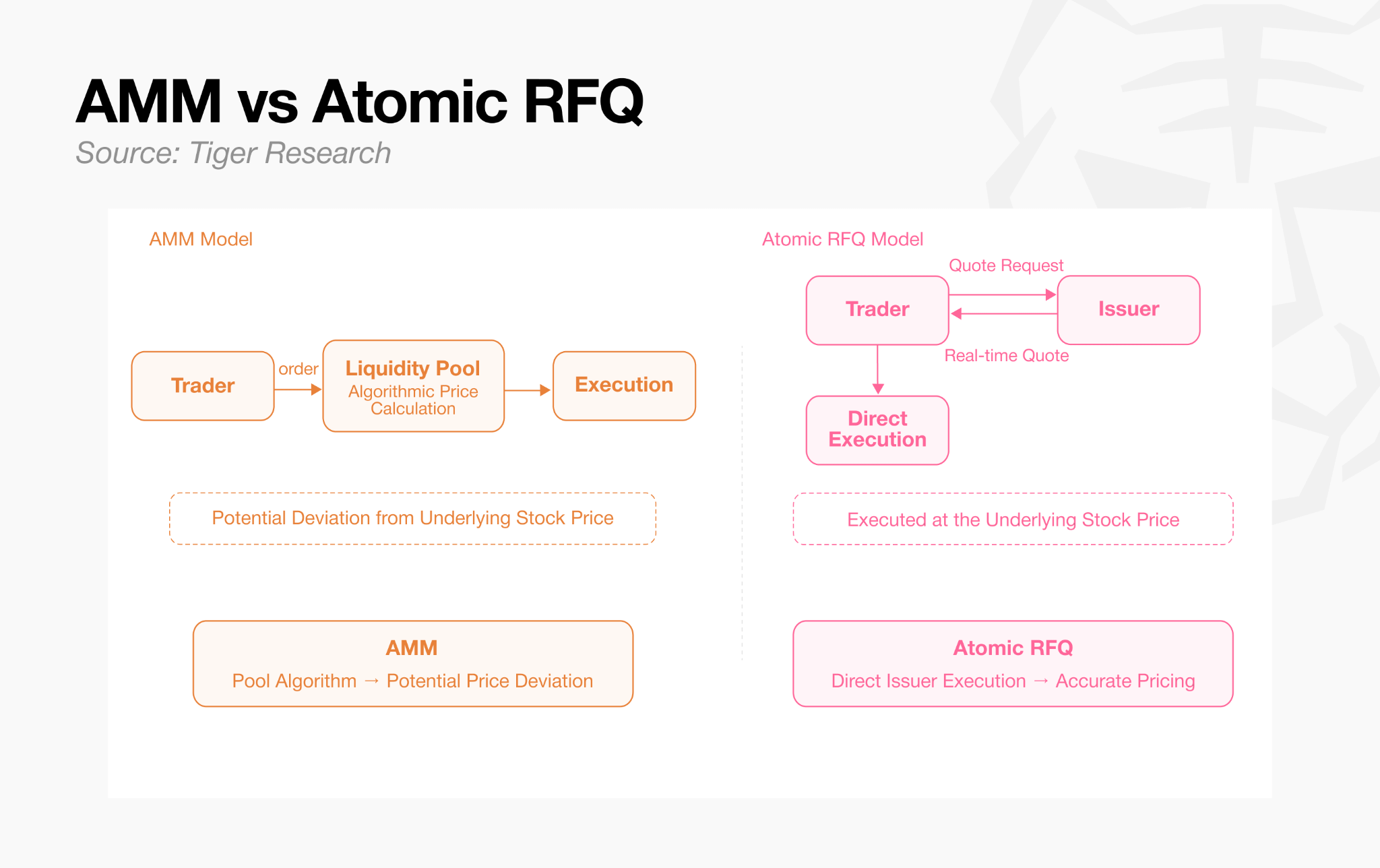

In May 2026, Bybit activated Atomic RFQ on Fluxion, a DEX within the Mantle ecosystem, upgrading the structure to direct issuer execution. Atomic RFQ works by requesting quotes directly from the issuer rather than routing through an AMM, achieving on-chain the execution quality that institutional participants expect in conventional finance.

Bybit has also moved on the centralized side. Facing pressures similar to those on Binance, it launched TradFi perpetual futures in April 2026 and has added new listings weekly. Major US stocks including Tesla (TSLA), Nvidia (NVDA), and Apple (AAPL), along with gold, silver, and crude oil, are now available for 24-hour trading settled in USDT. On June 4, Samsung Electronics, SK Hynix, and Hyundai Motor perpetual futures went live, and SpaceX pre-IPO trading is also supported.

Both tracks are ultimately aimed at building infrastructure for more precise trading of conventional assets across on-chain and off-chain venues. Where Bybit differs from Binance is in its effort to maintain an active on-chain presence through Fluxion and Mantle rather than concentrating entirely on the centralized platform.

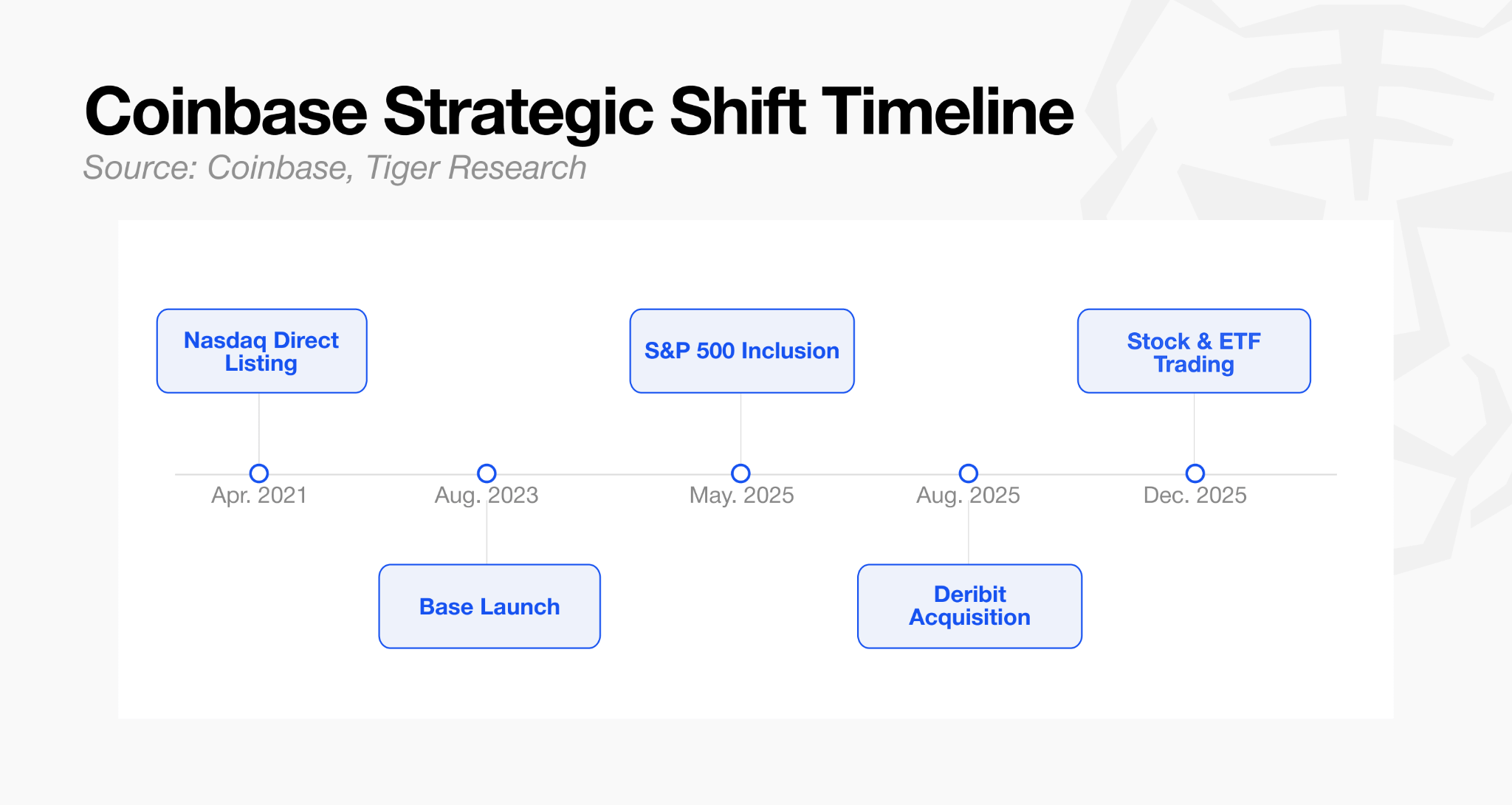

Coinbase listed on Nasdaq in 2021 and was added to the S&P 500 in May 2025. Backed by Wall Street, it is currently the centralized exchange that carries the most institutional credibility.

Coinbase has also maintained an on-chain presence. The Ethereum L2 Base, launched in 2023, climbed quickly to hold close to half of total L2 TVL by 2025. By 2026, however, growth had stalled and Base no longer appeared to be a core priority for the company.

Where Coinbase has committed most seriously is institutional clients. In August 2025, it completed the $2.9 billion acquisition of Deribit, capturing roughly 85% of the global crypto options market. It then launched a CFTC-licensed futures commission merchant (FCM) service and introduced cross-margin trading that consolidates spot, futures, and perpetual futures positions into a single collateral pool, broadening its institutional client base. Institutional lending balances from hedge funds and asset managers reached a quarterly record that year.

In December 2025, Coinbase opened commission-free stock and ETF trading within its existing app. Where Binance layered a separate brokerage infrastructure and took an indirect approach, Coinbase offers direct trading on the strength of its accumulated regulatory standing. On June 4, it announced support for SpaceX pre-IPO trading.

As Hyperliquid has built liquidity outside the regulatory perimeter by launching a broad range of products, Coinbase’s early entry into stock trading leaves it better placed to respond.

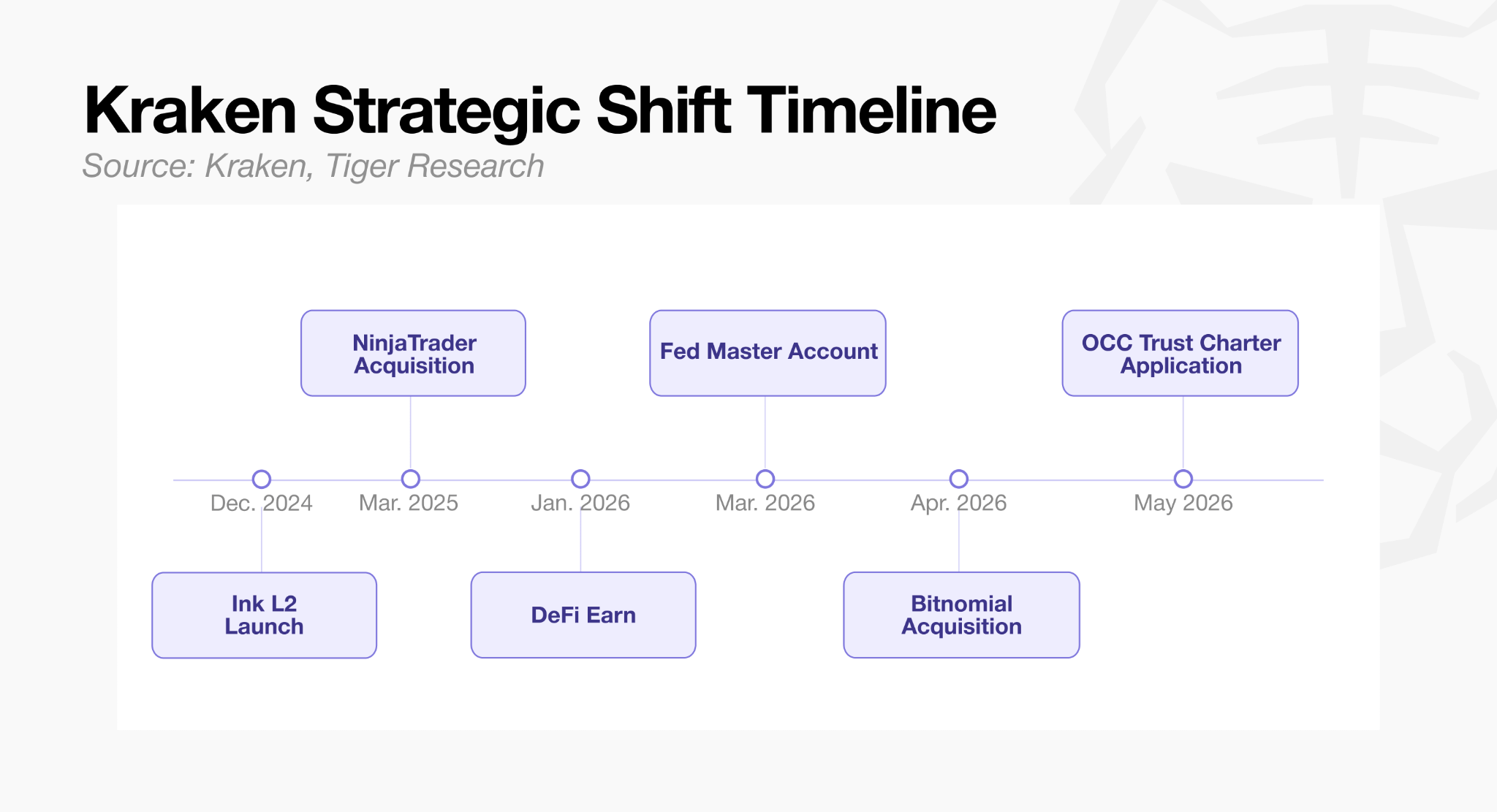

Founded in 2011, Kraken is one of the longest-standing exchanges in the crypto industry. Its strategy is to consolidate licenses, build infrastructure directly, and become a federally regulated institutional crypto custody bank.

Regulatory infrastructure has been the first priority. In March 2025, Kraken acquired NinjaTrader for $1.5 billion, gaining a CFTC FCM license and a retail trader base of two million users. In April 2026, it acquired Bitnomial for $550 million, the only crypto-native platform to have obtained all three CFTC licenses, DCM, DCO, and FCM, over a period of ten years. In March 2026, Kraken secured a Federal Reserve master account, and in May it filed an application with the OCC for a national trust company charter.

On-chain has not been neglected. Kraken launched its own L2, Ink, in December 2024, followed by lending protocol Tydro and perpetual DEX Nado on top of it. DeFi Earn launched in January 2026 and Bitcoin Vault in May. These products are built around assets that can be clearly explained to institutional clients. Altcoins have not been a priority in Kraken’s on-chain strategy either.

While other exchanges have moved into stock trading to retain users, Kraken has chosen a different path, aiming to become the only crypto-native bank that institutional clients can trust.

The strategies of the centralized exchanges covered here differ in their specifics. What they share is that altcoins do not feature prominently in any of their forward plans.

Centralized exchanges have been the liquidity backbone of the crypto ecosystem. They listed tokens and generated trading volume, and that support is what kept most crypto projects alive.

The underlying problem is that almost no crypto project has demonstrated real value through actual revenue. Token prices have been sustained not by protocol fundamentals but by exchange listings and early liquidity support mechanisms such as launchpools. For that structure to hold, exchanges and traders need to maintain sustained interest in crypto. Retail volume is shrinking, and without it, exchange listings and marketing support will follow. That structure cannot hold indefinitely.

The market itself has shifted toward tokens from projects that can demonstrate value through real product revenue, rather than depending on exchange support. Hyperliquid’s HYPE is the clearest illustration. It is one of the best-performing crypto assets at present, despite being the very actor that has drawn on-chain liquidity away from crypto and toward stock markets. This points to a weakening of the mutually beneficial relationship that previously existed between centralized exchanges and crypto projects.

The position of the exchanges reinforces this reading. Retail trading volume and user count are the foundations of any exchange business. Concentrating on crypto trading volume alone now risks eroding that foundation, because the market no longer finds newly listed crypto assets as compelling as it once did. Exchanges have little choice but to protect the infrastructure and user base they have built while finding other revenue sources to pursue.

That is what has driven the pivot toward stock derivatives, yield products, and custody. In redirecting their efforts, the exchanges have effectively left altcoins to fend for themselves.

In previous downturns, centralized exchanges weathered the bear market alongside crypto. Now they are looking for ways to grow without it. That is why this downturn is likely to be harder for crypto than previous ones.

Read more reports related to this research.This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.