TradingKey – SpaceX ( SPCX) options officially debuted for trading this Tuesday (June 17). Approximately 1.8 million contracts traded on the first day, with about $2.8 billion in premium changing hands, breaking the first-day volume record for single-stock options. Notably, market sentiment was clearly characterized by chasing the rally, with call option volume outstripping put option volume. The overall call/put ratio was approximately 1.3:1, indicating that capital is still betting on a continued rise in SpaceX’s stock price.

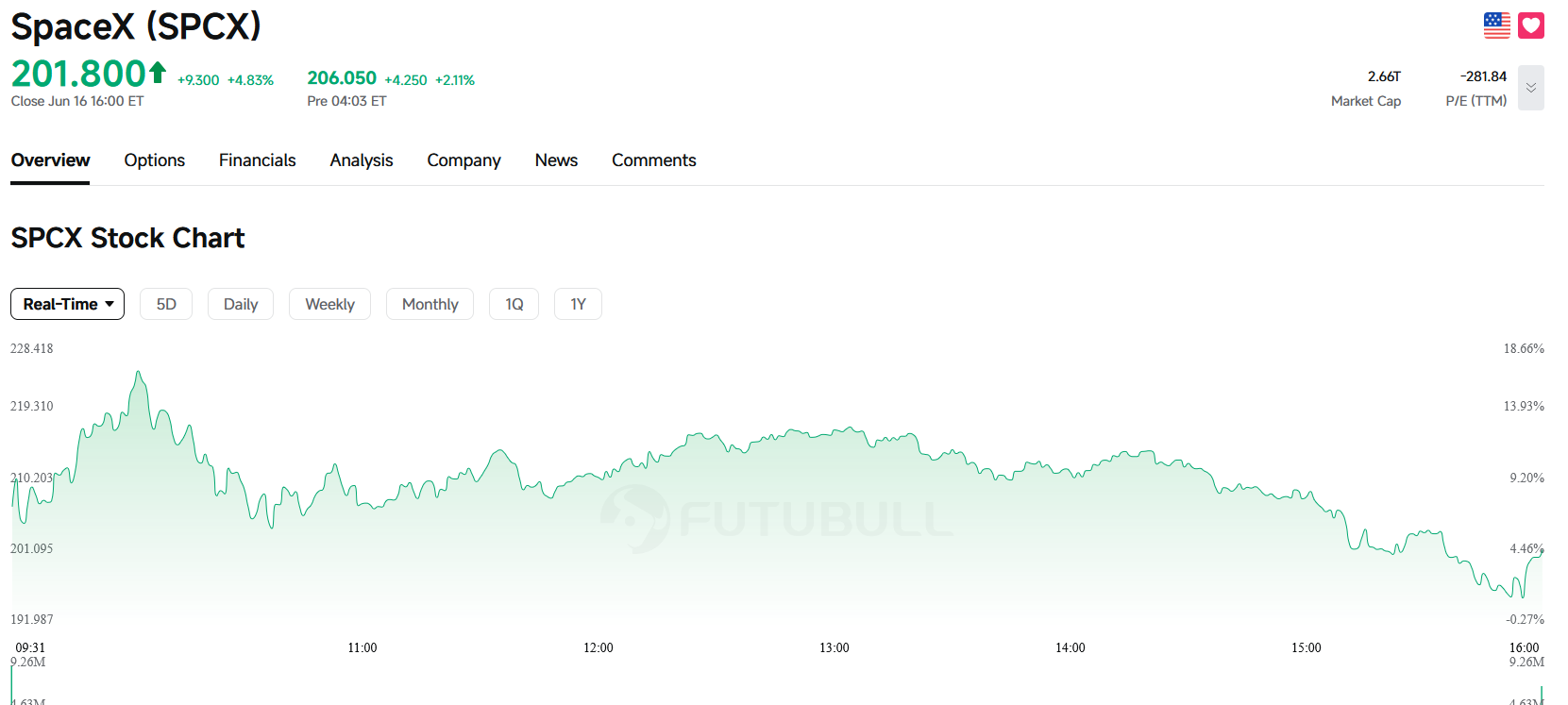

In terms of the underlying stock’s performance, SPCX’s first-day option trading and stock price volatility reinforced each other. The stock surged to near $225 intraday before pulling back to close at $201.80, though it still posted a significant gain from the previous session. For a highly watched star asset that has just gone public with a limited float, a surge in option market volume naturally amplifies underlying stock volatility. When a massive number of investors buy call options, market makers may need to buy the underlying stock to hedge their risk, triggering a short-term “Gamma squeeze.” However, once the stock price pulls back from its highs, option values can quickly evaporate, meaning the risk of buying out-of-the-money (OTM) calls at peak prices is also substantial.

SpaceX Stock Price Trend, Source: FUTUBULL

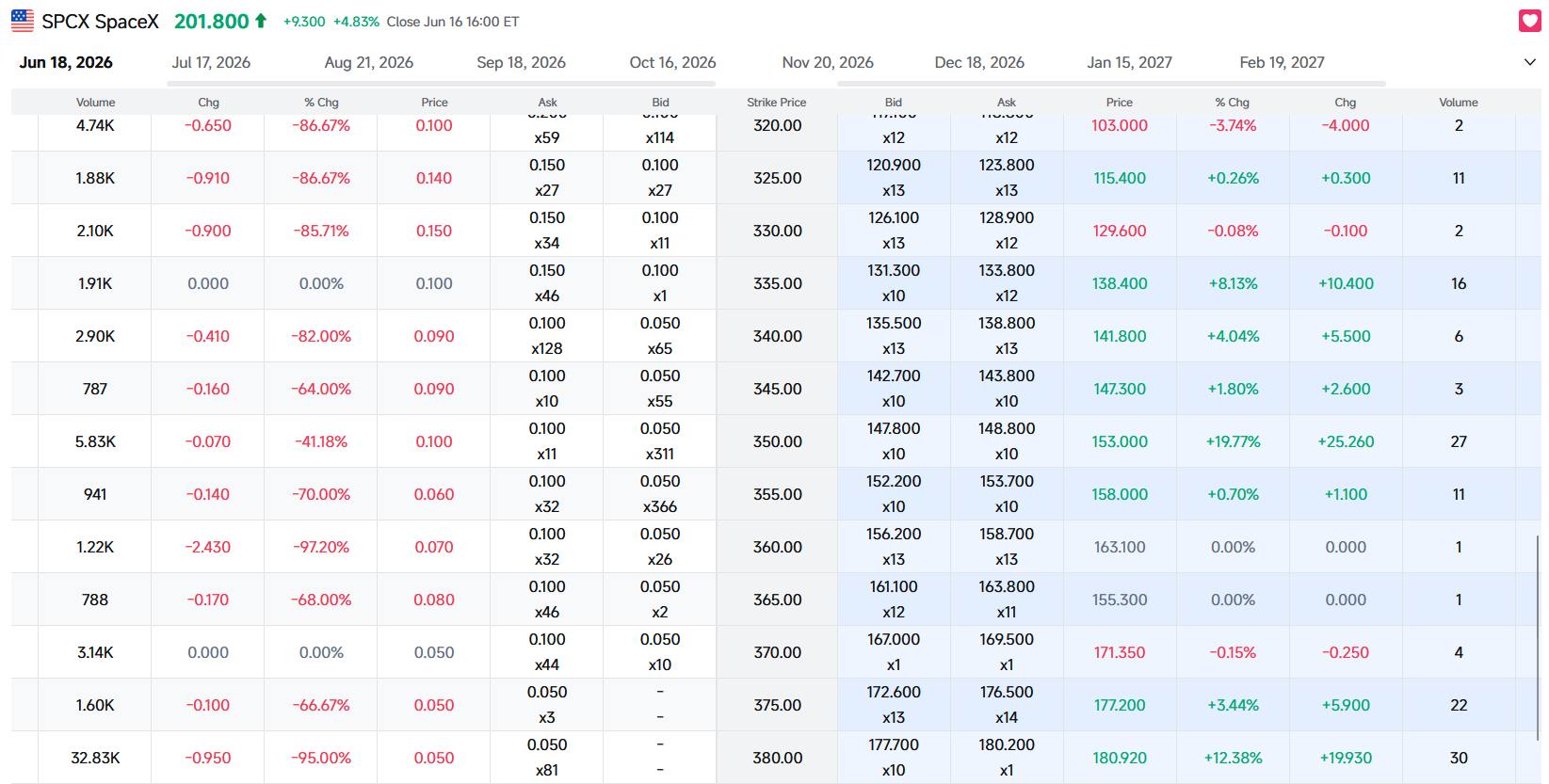

Looking at the volume structure of the option chain, near-term contracts best reflect the direction of short-term capital positioning. Among the near-term options expiring on June 18, trading was highly active near the at-the-money (ATM) range, including the $200, $205, $210, and $220 strikes, indicating that the market is re-pricing SpaceX’s short-term anchor around $200. Taking the $200 strike as an example, heavy volume was recorded on both the put and call sides, indicating this is both a defensive support line for bulls and a core level for short-term directional bets and risk hedging. Call contracts in the $205-$220 range were also prominent, suggesting the market remains willing to pay a high premium for continued short-term upside.

SpaceX Option Data, Source: FUTUBULL

However, the true gauge of speculative fervor lies in the long-dated out-of-the-money (OTM) calls. Contracts around the $300, $375, and $380 strikes also saw noticeable volume, indicating that some capital is deploying small premiums to bet on extreme upside scenarios. The appeal of these trades lies in their capped downside and massive potential leverage. The catch, however, is that implied volatility is often driven to extreme levels by sentiment during the initial listing phase. Buying deep OTM calls is not simply buying a “cheap lottery ticket,” but rather paying an expensive premium for extreme volatility. If the underlying stock fails to continue its sharp rally in the short term, time decay will erode the option’s value very rapidly.

For aggressive investors who are bullish on SpaceX’s continued upside, rather than buying high-priced OTM calls outright, a bull call spread may be more suitable. This involves buying a near-the-money call while simultaneously selling a call with a higher strike price, sacrificing some upside potential to reduce the entry cost. This approach allows participation in the rally while preventing single-leg call options from suffering a severe valuation crush when high volatility subsides.

For investors who already hold SPCX shares, the primary value of options is not to chase the rally, but to manage risk. With the potential pressure of a lock-up expiration in August, downside protection trades targeting September contracts have already emerged in the market. Shareholders could consider protective puts or covered calls (selling a corresponding number of call options while holding the underlying stock) to lower their holding costs. However, covered calls come with a trade-off: if market sentiment drives the stock price up again, investors may forfeit their upside gains prematurely.

For neutral traders, it is currently more advisable to wait for volatility to cool down rather than blindly selling volatility at the peak of sentiment on day one. Pricing has not yet stabilized in the early stages of listing, and bid-ask spreads, implied volatility, and market-maker hedging can all cause abnormal swings. A more robust approach is to monitor several key areas: first, whether the $200 level can hold as effective support; second, whether the previous high of $220—$225 can be broken again; and third, whether deep OTM call volume remains concentrated above $300. If speculative interest spreads but the stock price fails to advance in tandem, it indicates that speculative capital may be entering a waning phase.