We built our 2026 outlook around three themes: (1) Based on accommodative capital markets conditions, we expected private market transaction volumes to extend the recovery that set in in 2025; (2) We emphasized that bank lending appetite is a key driver of fund finance origination volume and that balance sheet trends and capital regulation developments would likely support fund lending growth; and (3) We flagged a concern that higher interest rates could become a limiting factor to the fundraising recovery.

We review these themes in light of broader market volatility due to the Iran conflict, questions on future capital flows from Middle East investors, elevated redemptions from semi-liquid private credit vehicles, and uncertainty around credit fund asset values. Despite these developments, we find that transaction volume has continued to gain momentum and the bank lending capacity outlook has further strengthened.

Transaction Volume Continues to Improve

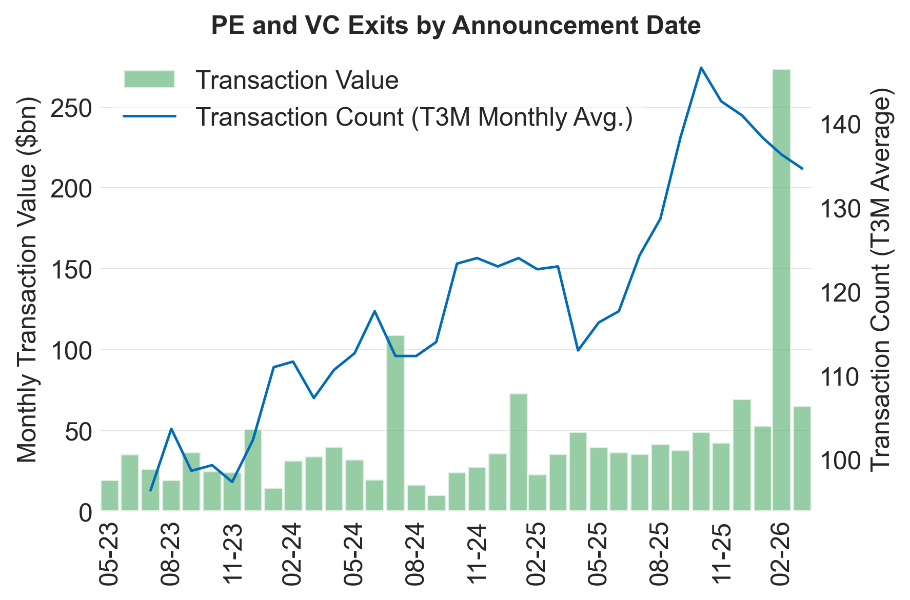

While PE and VC exits slowed in March, the longer-term trend remains positive. Breakout transaction volume for the month suggests that, while exits were constrained, funds went to work on deployment.

Source: S&P Capital IQ and Cadwalader, Wickersham & Taft LLP.

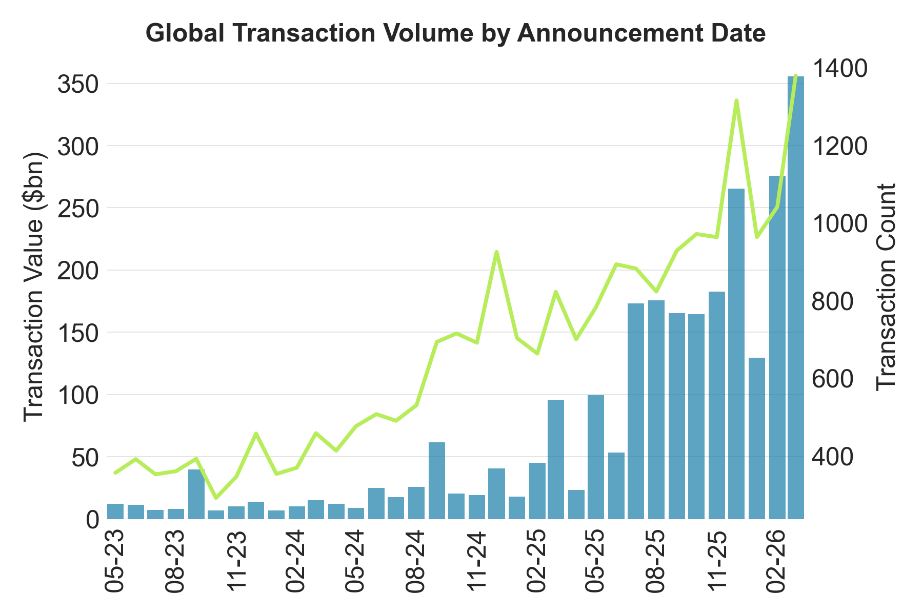

Source: S&P Capital IQ and Cadwalader, Wickersham & Taft LLP.

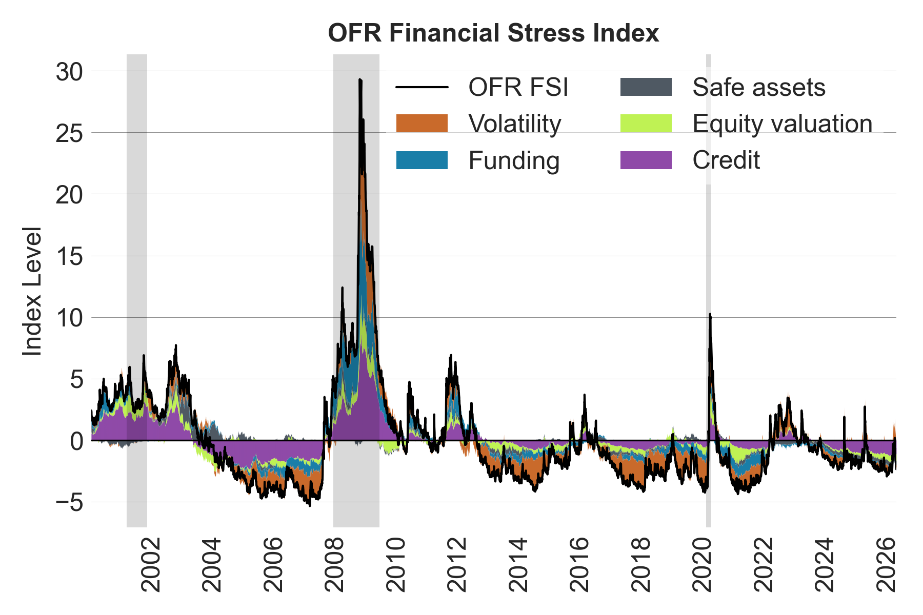

Broader market conditions support further gains. The Office of Financial Research Financial Stress Index, which measures 33 market variables, including yield spreads, valuation measures, and interest rates shows that Iran conflict stress has thus far proved short-lived with the index returning to January–February levels. The index signals accommodative conditions that should support further deal activity gains.

Source: U.S. Department of the Treasury Office of Financial Research and Cadwalader, Wickersham & Taft LLP.

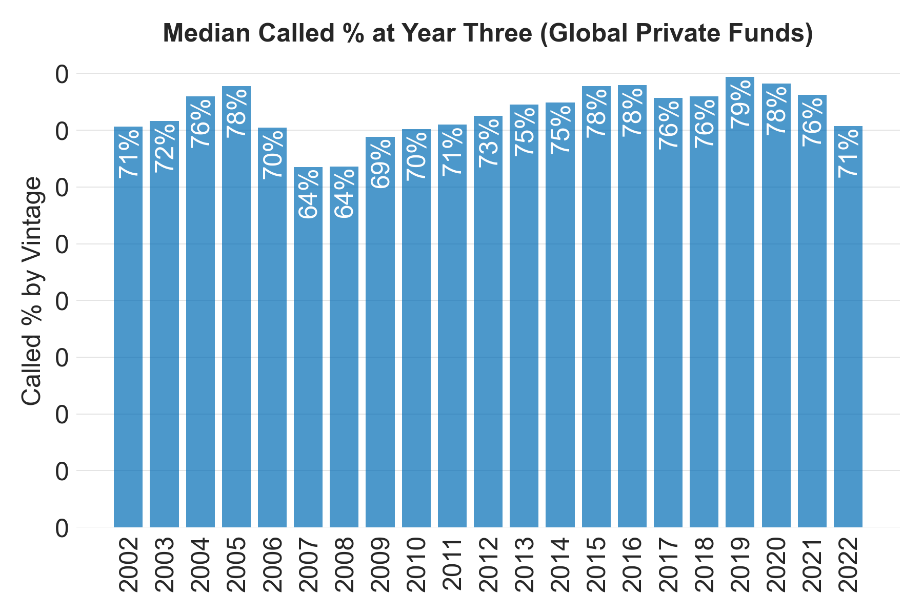

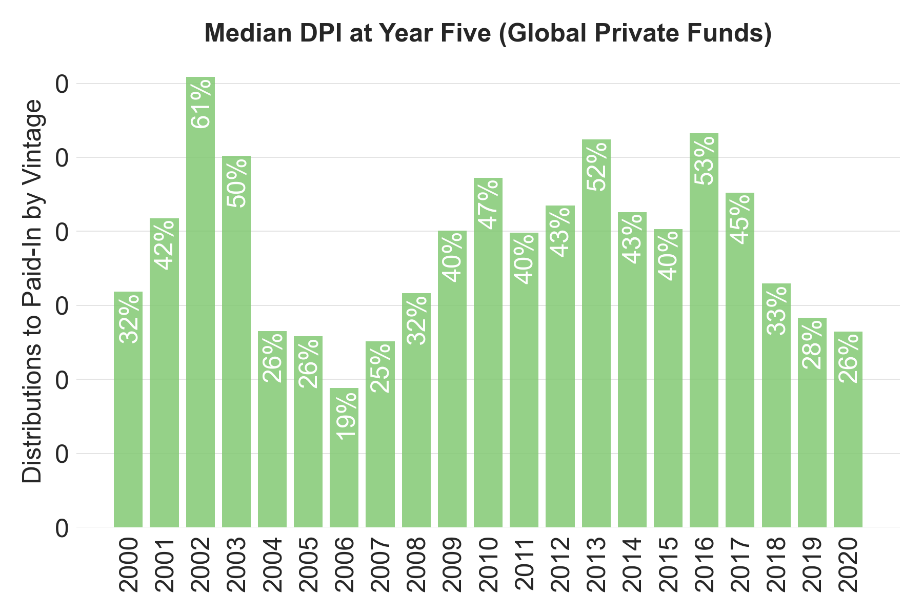

Accelerating deal activity has to be viewed in the context of the nearly $13 trillion in accumulated private fund AUM. Because of the size of the market, two things can be true at the same time: Deal activity may be accelerating while distributions remain under pressure.

Source: Preqin, S&P Capital IQ, and Cadwalader, Wickersham & Taft LLP.

Source: Preqin, S&P Capital IQ, and Cadwalader, Wickersham & Taft LLP.

Bank Lending Capacity—More Runway

Bank capacity (willingness and ability to extend credit) is an often-overlooked driver of fund finance origination volume. The industry banks only a fraction of the $1.3 trillion in funds raised per year. Within the subset of and bankable institutional LP pool funds, the swing factor is bank capacity.

Bank capacity is positioned to support origination growth in 2026. Aggregate indicators across balance-sheet constraints, funding costs, credit stance, and loss dynamics are all positioned to support growth for banks with $100 billion or more in total assets (although subscription facility economics have tightened).

The recent Basel III re-proposals add long-term support to an origination growth thesis through the 65% risk weight available to unlisted corporate exposures (currently 100% if not publicly traded). Specifically, Category I and II banking organizations will have broader access to a 65% risk weight for non-subordinated corporate exposures based on a determination that the exposure is to an investment-grade counterparty using an internal credit risk rating system that is used in actual business and risk-management decisions and is subject to validation requirements. The lower risk weight category is currently only available to publicly traded entities.

Interest Rates Inform Fundraising

Over the past five years, we’ve often related capital velocity in private markets directly to fundraising, with the thesis that improvement in the return of capital to investors would drive fundraising. At this juncture, we see higher interest rates loosening the connection between the two. As depressed distributions defer fund cash flow and duration extends into a higher rate environment, improved capital circulation in private markets may become less directly linked to fundraising.

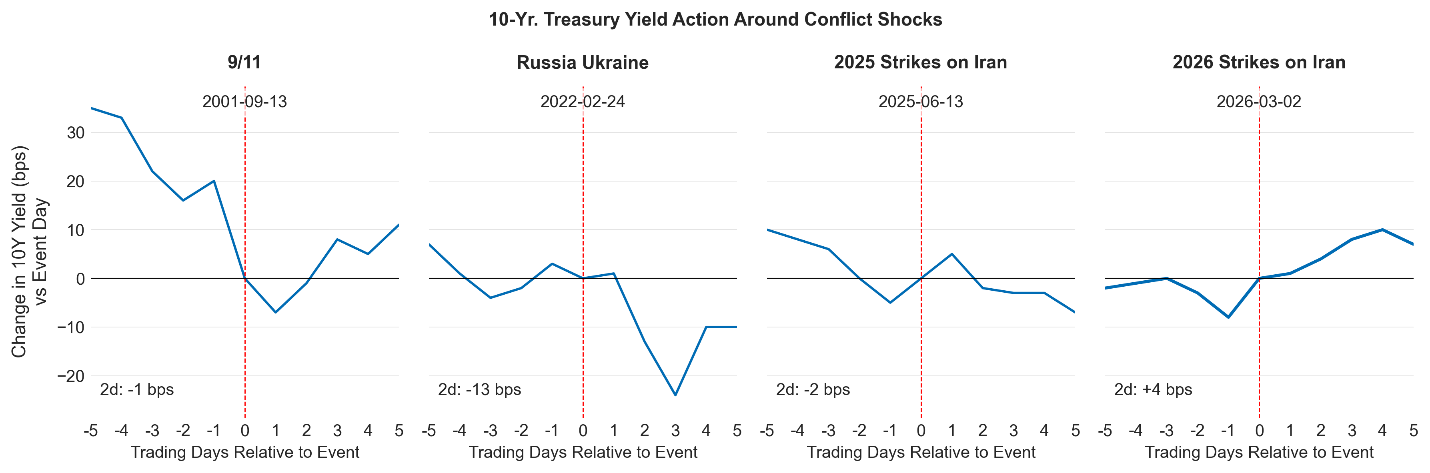

In 2026, Treasury buyers have been quick to look past conflict-driven dislocation to instead anticipate rising inflation, fiscal impulse, and rising Treasury supply. These dynamics were visible in March when Treasury auction internals weakened and long-end yields failed to mount a flight-to-quality rally amid geopolitical conflict. Instead, long-end rates are higher today than at the beginning of the Iran conflict.

Sustained higher long-end rates signal (1) that investors may be reluctant to take on duration amid inflation uncertainty and the high Federal deficit, and (2) that liquid fixed income products will be relatively more competitive to the static 8% preferred return embedded in closed-end funds. Over time, lengthened durations for private fund investments may influence allocation decisions.

For fund finance lenders this dynamic may continue to translate to stretched facility closing timelines, long fund intervals, and ultimately interest rates imposing a soft ceiling on the rebound in fundraising. In this context, GPs and LPs are likely to continue to engineer liquidity through financing structures and in the secondaries market.

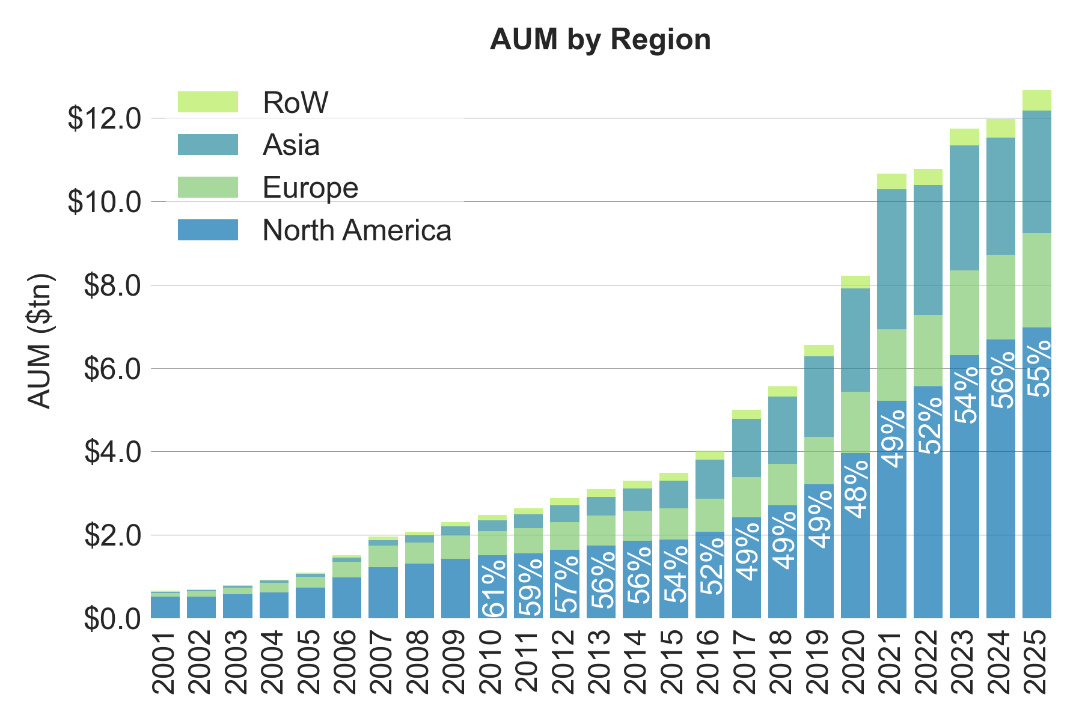

A Global Perspective

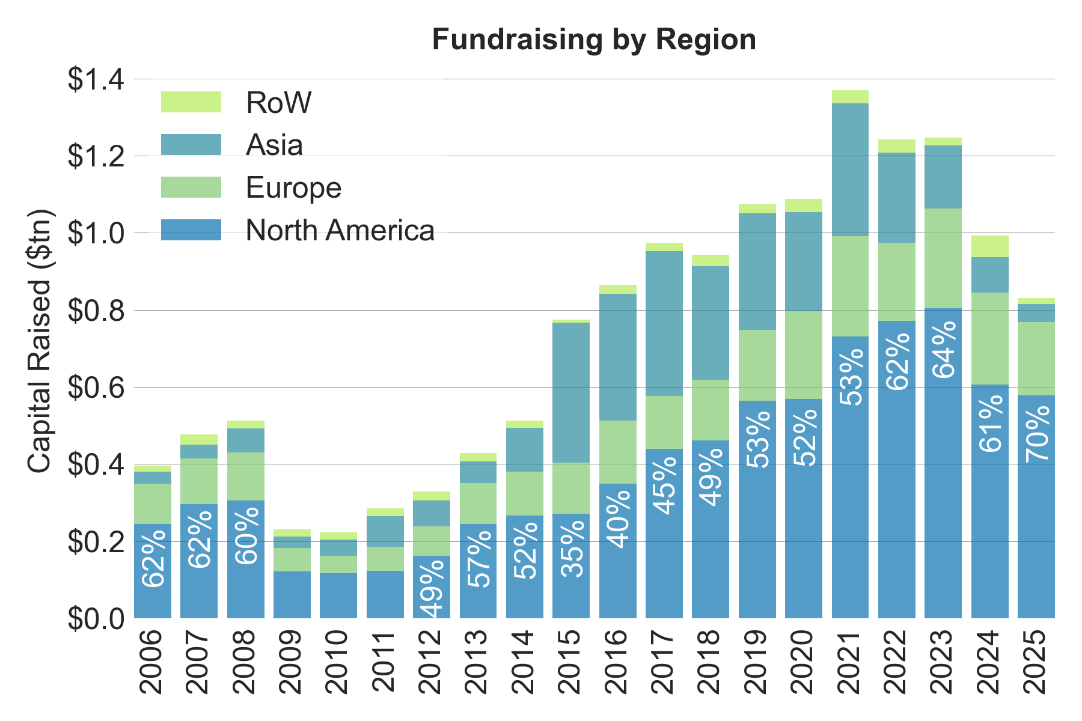

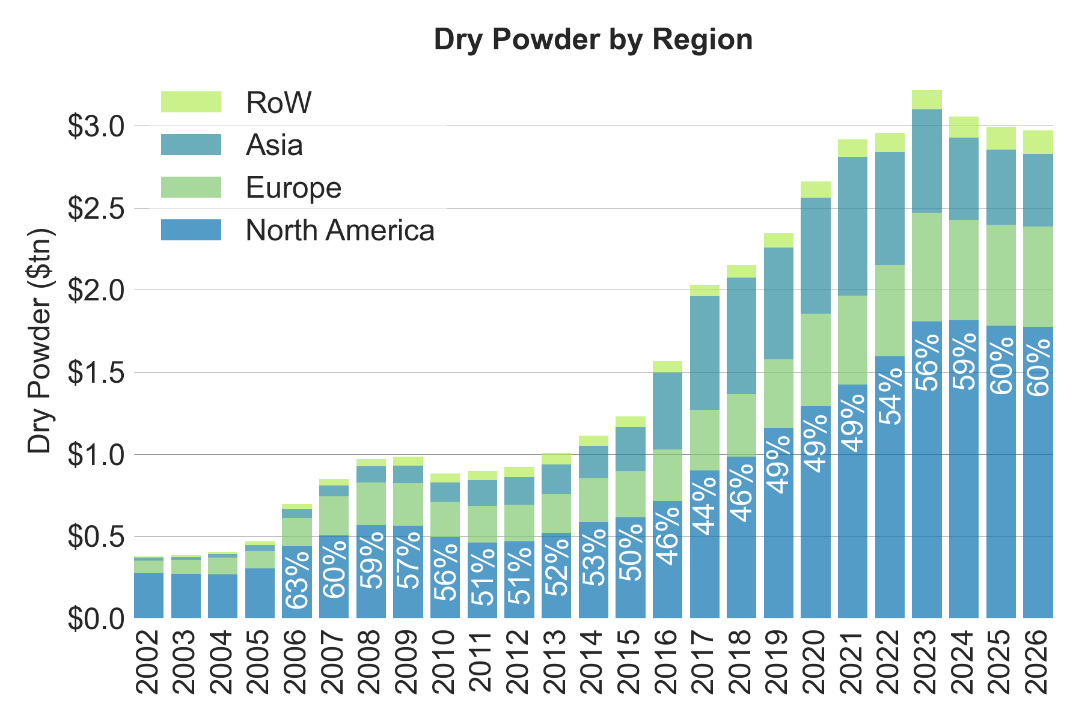

On an international basis, the addressable fund finance market varies by product segment. In recent years, fundraising has skewed toward North America, implying that new money subscription lines are more likely to be sourced from this region. (In process Asia-focused fund closings will influence the mix this year.) Dry powder, by contrast, is more broadly distributed by region.

Compared to the subscription oriented measures (fundraising and dry powder), the more NAV oriented AUM is less concentrated in North America, adding context to the view that NAV uptake is higher outside this region.

Conclusion

To complete the picture on private markets and the outlook for fund finance, it’s helpful to review the drivers that have supported fund finance origination growth over the years:

- Because fund finance does not primarily rely on a capital markets funding mechanisms, episodic credit market volatility has a far less disruptive impact on the market.

- Unlike the almost all other secured credit products, subscription collateral values are not tied directly to interest rates. Corporate loans that rely on interest coverage ratios, consumer loans tied to borrower debt servicing capacity, or discounted cash flow assets experience an loan interest income benefit from higher rates, but with some offsetting impact on collateral values.

- Finally, fund finance services a large global sponsor base with many dimensions of diversification across region, strategy, investment asset class, investor base, and vintage.

As in the past, these differentiating factors will continue to provide a supporting foundation in 2026.